Asset protection comparison & definitions of General Partnership, Limited Partnership, Corporation Chapter “C”, Corporation Chapter “S”, Limited Liability Companies & Revocable Trusts and Irrevocable Trusts.

PART 2: ASSET PROTECTION: GENERAL/LIMITED PARTNERSHIP, CORP CHAPTER “C”/CHAPTER “S”, LLC, TRUSTS

Read PART 1: ASSET PROTECTION: JOINT TENANCY, TENANCY IN COMMON, TENANCY IN ENTIRETY & COMMUNITY PROPERTY

Watch the video on Like this video? Subscribe to our channel.

THE CONCEPT OF ASSET PROTECTION includes the possibility of placing title in certain assets in the name of a less vulnerable spouse or other family members, or a legal entity. One should be very attentive in transferring title without an open invitation to a “fraudulent transfer” claim against the asset transferred due to the possibility of death, marriage dissolution, or a court judgment.

Fraudulent conveyance refers to transferring assets at less than the “fair cash value,” thereby defrauding a potential creditor or intentionally divesting assets, making them unavailable for a lawsuit. Fair cash value means cash or near-cash value at the time of transfer, not the original purchase price. For example, transferring home equity worth $250,000 to a spouse for $100 or transferring a car title to a brother for $10.

Common Methods of Holding Assets by Individuals

• Joint Tenancy

• Joint Tenancy with Right of Survivorship

• Tenants in Common

• Tenancy by the Entirety

• Community Property

(Read part 1 “Asset Protection with Joint Tenancy, Tenancy in Common, Tenancy in Entirety & Community Property”)

Legal Entities (Artificial Persons Created by Law)

• General Partnership

• Limited Partnership

• Limited Liability Company

• Corporation under Chapter “C”

• Corporation under Subchapter “S”

• Revocable Trust (A Trust is essentially a Contract)

• Irrevocable Trust (Irrevocable variations exist since a Trust is a Contract)

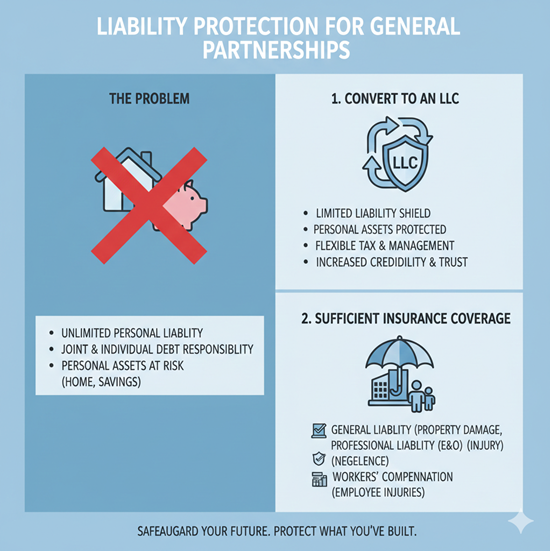

General Partnership

A General Partnership is an association of individuals owning property or a business together. However, it exposes all partners to liabilities, meaning any partner can be held 100% liable for another’s actions. It is one of the riskiest business structures.

Limited Partnership

A Limited Partnership consists of one or more General Partners who control the partnership and one or more Limited Partners who have no control. This setup can offer asset protection and tax advantages, particularly in a Family Limited Partnership where parents maintain control while gradually transferring ownership to their children tax-free.

On Family Limited Partnerships

The key benefits of a Family Limited Partnership:

• Asset protection: Creditors cannot step into the shoes of a partner. The only remedy is a “charging order.”

• Reduction of Federal Estate Taxes: Lifetime gifts under tax-exempt rules help transfer wealth while retaining control.

• Estate tax valuation reduction through discounting for lack of marketability and minority interest.

Limited Liability Company (LLC)

An LLC is a hybrid “pass-through” entity offering the tax benefits of a partnership while providing limited liability like a corporation.

Corporations (Standard Corporation under Chapter “C”)

A “C” Corporation is the most common business structure, offering limited liability for shareholders. However, shareholders face double taxation on corporate profits and dividends.

Corporation Under Subchapter “S”

An “S” Corporation provides pass-through taxation benefits, but it comes with many restrictions.

Revocable Trust or Revocable Living Trust

A Trust is a Contract between the Grantor (owner), the Trustee (who manages assets), and Beneficiaries. A “Revocable” Trust allows the Grantor to retain control, meaning:

Irrevocable Trusts

An Irrevocable Trust transfers full control of assets to a Trustee, offering strong asset protection and tax benefits.

Trustees have strict fiduciary duties, including:

• Keeping beneficiaries informed.

• Managing trust assets solely for beneficiaries.

• Preserving trust assets.

• Prudent investment diversification.

Fiduciary Duty and Legal Cases

Example of fiduciary breach: In the 2006 case *Fifth Third Bank v. Firstar Bank*, a trustee was sued for failing to diversify investments quickly enough, resulting in a $1M judgment.

For more information on asset protection and estate planning, visit www.ultraTrust.com.

Our strategy is to leverage knowledge and multi-dimensional approaches to protect assets from lawsuits, minimize taxes, eliminate probate, and ensure tax-efficient wealth transfers to future generations.

Helpful resources: Helpful next steps often include Asset Protection for Business Owners, LLC vs Trust for Asset Protection, and official SBA guidance when weighing practical next steps.