What are Fraudulent Transfers? What is Civil Conspiracy? What is the Uniform Fraudulent Act state regarding LLC and creditor claims? Discuss the Single Member LLC within the context of owning public shares in a stock and its role in asset protection.

Under the Uniform Transfer Act you would be committing a crime, see Section 19.40.041

“…(a) a transfer made or obligation incurred by a debtor is fraudulent as to a creditor whether the creditor’s claim arose before or after the transfer was made or the obligation was incurred, if the debtor made the transfer or incurred the obligation: (1) with actual intent to hinder, delay, or defraud any creditor of the debtor…”

Watch the video on 'Fraudulent Transfers, Civil Conspiracy, Uniform Fraudulent Transfer Act'

Like this video? Subscribe to our channel.

Fraudulent conveyance has to do with transferring assets at less than the “fair cash value” thereby defrauding a potential creditor or the intentional divesting of assets which become unavailable for satisfaction of the creditor’s claims. Fair cash value means cash or near cash value at the time of transfer, not the price you paid for the asset.

For example, you transfer your portion of your equity in your home to your wife for $200.00 and the fair cash value of your portion of the equity was $250,000 (total value of the home was $500,000) or you transfer title to your Mercedes to your brother for $100.00. Additionally the IRS would claim that such a transfer is a gift subject to a gift tax return and assess a penalty for the non-filing of Form 709 (PDF) United States Gift (and Generation-Skipping Transfer) Tax Return.

What is Civil Conspiracy?

The “civil conspiracy theory” has been defined by the courts as (1) an agreement (2) by two or more persons (3) to perform overt act(s) (4) in furtherance of the agreement or conspiracy (5) to accomplish an unlawful purpose or a lawful purpose by unlawful means (6) causing injury to another.

To be convincing, the creditor must allege not only the conspirators committed the act but also the act was tortious in nature. The conspiracy alone is not enough to trigger a claim for civil conspiracy without the underlying tort. Lately, however, advisors have been dragged into the creditor claims as co-conspirators for suggesting and implementing everyday common asset protection strategies. This has made me more cautious, making sure that I don’t get dragged in to my own legal nightmare.

Example of Single Member LLC Membership Units and Shares in a Public Stock

SINGLE MEMBER LLCs should be avoided. The example I can use is this: If you own 1,000 shares of General Motors it’s considered a personal asset subject to a creditor claim. If the claim is perfected by litigation in favor of the creditor the owner of the 1,000 shares of General Motors will have to transfer those shares to the creditor in satisfaction of his claim. Owning single member units of an LLC is not any different. The Owner of the LLC membership units is equivalent to owning the 1,000 shares of General Motors and therefore subject to a perfected creditor claim.

Asset Protection: Placing Title of Assets in Another Legal Entity

THE CONCEPT OF ASSET PROTECTION includes the possibility of placing title in certain assets in the name of a less vulnerable spouse or other family members, or a legal entity. One should be very attentive in transferring title without an open invitation to a “incorrect transfer” claim against the asset transferred or the possibility of death by the spouse or family member, or possible dissolution of the marriage, or a court judgment.

The most common methods of holding assets by INDIVIDUALS:

Joint Tenancy

Joint Tenancy with right of survivorship

Tenants in Common

Tenancy by the Entirety

Community Property

LEGAL ENTITIES (Artificial person created by application of law):

General Partnership

Limited Partnership

Limited Liability Company

Corporation under Chapter “C”

Corporation under Sub Chapter “S”

Revocable Trust (There are many Revocable Trust variations, since a Trust is nothing more than a Contract)

Irrevocable Trust (There are many Irrevocable Trust variations, since a Trust is nothing more than a Contract)

To learn more about avoiding conveyance rules and how to avoid civil conspiracy theories when repositioning assets and implementation of precise asset protection systems speak with an experienced and knowledgeable financial planner and advisor in these matters such as Estate Street Partners offering free initial consultations.

I always caution against simply speaking with only an attorney and only an accountant in complex financial planning with regards to single member LLC scenarios, partnerships in Limited Liability Company formations, regulations surrounding conveyance and civil conspiracy and asset protection. It’s best to develop or consult with a group or team consisting of an attorney, accountant and financial planner or advisor to offer you the best, well-rounded protection. You will gain a more thorough understanding of the nature of asset protection from LLC formations to avoid incorrect conveyance and civil conspiracy judgments.

Watch the video on 'What is Asset Protection'

Like this video? Subscribe to our channel.

“LATE-R” is already too “LATE.”

“If you’ve taken NO steps to protect yourself, your wealth, and your family from thieves, con artists, ruthless greedy lawyers, overzealous bureaucrats; you have underestimated the abilities of these shrewd, ruthless, invasive, money-hungry, predators.” – Rocco Beatrice, CPA, MST, MBA

Definition:

It’s the concept of protecting and preserving one’s assets from frivolous, illogical, ill motivated, more often than not, devastating catastrophic claims against your wealth, designed to destroy your current and future lifestyle. In short, they want what you’ve got and they want to inflict maximum pain.

Asset protection has two goals:

To make the enforcement of judgments against your protected assets virtually impossible, and

To allow the “owner” of protected assets to retain engineered “control” over his assets

How Good Asset Protection can Protect Your Privacy:

“Identity Theft” is the fastest growing financial crime in America – source: the U.S. Secret Service

There are literally hundreds of ways to protect your assets. Some are just common sense. Don’t flash your money around; don’t talk too much at parties, etc. By implementing a properly crafted asset protection plan, your creditor will have to jump through several hoops, before he even finds your money. A contingent fee predator lawyer will want an easier target.

There are approximately 950,000 lawyers. Just go through your own yellow pages. Most of them live on what they can “squeeze out of you.” Don’t become a statistic. Learn from other people’s mistakes. Learn how to become every contingency-fee lawyer’s nightmare.

The Internet is spyware on steroids and can be used as invisible wealth snatchers. Information collection about you, your associates, your family, your finances, has been compromised by the enhancement of data gathering technology through the internet. “Even if you’ve got nothing to hide” your very basic privacy can be had for a few bucks by thieves, con artists, ruthless greedy lawyers, and overzealous bureaucrats.

How “paranoid” are you? How “paranoid” should you be? the problem is not the zillion merchants collecting data about your spending habits. The problem is who’s collecting the data without your knowledge. And, for what purpose?

A Good Plan will:

Protect your current and future lifestyle

Discourage litigation and promote settlements, in your favor

Keep the ownership of your assets confidential and hard to find

Eliminate the need of prenuptial agreements

Internationalize your investments as a hedge against the unexpected surprise

Spread out your control over your most valuable assets

Help you in getting a fresh start, if you ever became insolvent in any of your other assets

Hedge against potential political, economic, and personal instability

Chartered Blueprint of Wealth Preservation and Steps to Protecting Assets:

What are your financial goals?

Think about each of your personal/business assets that you need or wish to protect

Will there be domestic and/or international platform(s)?

*Customized Hybrids, i.e. LLC, Family LLC, Limited Partnership, Family Limited Partnership or General Partnership is owned by an UltraTrust®

* = My preferred structures

Foreign Platform(s)1 (please read note – 1)

Foreign Bank Account

International Business Company

Foreign A/P Trust

Foreign Security Trust

Foreign Limited Liability Company (FAPT)

Offshore Uni Trusts

Offshore Mutual Fund

International Trading Company

Multi-Currency Bank Deposits

Swiss Annuities

Foreign Credit Card

Foreign Stock Trading Account

Registered Foreign Office

Registered Foreign Sales Facilities

Note – Use “Good” planning NOT “Secrecy.” Rely on “Law” NOT “Secrecy.”

1**Watch out for Foreign and Offshore Scams & Practitioners**

There’s a thriving industry of “offshore practitioners” advising IRS definition of “U.S. Person” to set-up offshore bank accounts and other financial structures thinking that they have “just become NON-U.S. Taxable.” They persuade the U.S. Persons to trust the “Iron Clad” secrecy laws of the jurisdiction and not to report ownership of their funds or structures to the Internal Revenue Service and other agencies. This is pure and simple tax fraud and gets many U.S. Persons in trouble.

WARNING: Complexity(ies) of U.S. laws requires many tax reporting and other various reporting requirements. Protect yourself, make absolutely sure that you seek competent professional expert legal, accounting, and tax advice before you consider implementing your foreign A/P plan. Contact Estate Street Partners and get the facts for proper U.S. reporting procedures.

Authorities are looking for NON-COMPLIANCE, not for those who report and comply. We believe in full disclosure. If there’s no reporting form, we make-up our own and file.

To my knowledge, there are no laws prohibiting you from protecting your hard-earned money with offshore international structures, as long as you file all proper documentation with proper reporting agencies. When protecting your assets / wealth preservation plan is professionally and carefully implemented by competent professionals, the foreign side of life becomes significantly enhanced. Most international jurisdictions do not recognize U.S. based creditor judgments.

For example: a proper utilization of a foreign bank account should be part of protecting your assets / wealth preservation plan, it’s the less complex and the most useful part of protecting your assets / wealth preservation strategy. Your cash will become an “A/P fortress,” just make sure that you check the box on your Form 1040 schedule B, and file TD F 90-22.1. NO BIG DEAL. There is absolutely no downside to proper reporting on the existence of a foreign bank account.

No Financial plan is ever 100% bullet proof: Know These Facts about a good plan

You can’t lose your assets without first being sued and them winning the lawsuit. Winning and getting the money are two separate issues.

Implement your A/P strategy when times are good. It’s too late when the crap starts flying. You will have to deal with several “fraudulent conveyance” laws – that is, if you had some warning, or you merely became aware (real or potential), or you should have been aware that someone was going to potentially sue you. By implementing any A/P plan, you made your assets unavailable to satisfy creditor claims. Therefore, you may be found guilty of a “fraudulent conveyance.” The judge may set aside your attempt to hide your assets and hand it over to your creditors. In addition, the judge may decide to throw the book at you with other financial and possibly other consequences. PLAN EARLY, when the sea is calm. Don’t become a statistic.

Your creditors can’t take what you don’t have. Don’t put everything in your name. Don’t be so obvious.

What your creditor’s don’t know becomes your asset. Don’t volunteer information, don’t flaunt your wealth, don’t talk too much at parties, don’t tell them your business, don’t tell them how smart you are.

No country in the world will automatically honor a judgment against you. Outside the United States there are no contingency lawyers. Your creditor must re-litigate his case in the foreign country. Your creditor must put up a bond. Your creditor must pre-pay attorney fees. If your creditor loses his case he must pay your attorney fees. Finally, your creditor must prove that the laws of their country are invalid, the judge is a bum, and that the whole country should disappear into the sea.

There’s a greater chance that you will be sued more times than you will have a hospital stay.

Your Individual Retirement Account (IRA) is not protected by ERISA. Your Individual Retirement Account is usually the second asset to be attacked, behind your cash and investment account. Your IRA is an easy target because (1) It’s always in the United States and (2) Your IRA is usually in cash or near cash.

The United States is the only country that permits contingent fee litigation.

There are approximately 950,000 lawyers. Just go through your own yellow pages. Most of them live on what they can squeeze out of you. Don’t become a statistic.

For many self-made, hard working citizens, the “American Dream” can become the “American Nightmare.” Exorbitant taxes, lawsuit-friendly courtrooms, persistent predator plaintiffs, and contingent-fee clever lawyers are a constant threat to everything you’ve worked so hard to accomplish. It could all evaporate before your very eyes.

Take personal responsibility. If you’ve taken no steps to protect yourself, your wealth, and your family from thieves, con artists, ruthless greedy lawyers, overzealous bureaucrats…you have underestimated the abilities of these shrewd, ruthless, invasive, money-hungry predators.

Hundreds of books, thousands of articles, every third (3rd) lawyer claims to be a knowledgeable, experienced, asset protection expert.

In my 45 years’ experience, the nuts and bolts of asset protection strategies are about giving your creditor two (2) options:

Option #1. YOU dictate the terms of settlement to your creditor,

or

Option #2. YOU threaten to file for bankruptcy, and your creditor gets NOTHING.

Which is better: diarrhea or throwing-up?

We have been helping clients with court tested, expert level estate planning for more than 30 years. We avoid canned approaches by evaluating and personalizing your plan to your specific family dynamics, protection of your wealth from unwanted creditors, elimination of probate, elimination of estate taxes, tax optimization, and tax-efficient transactions to preserve and grow your wealth. Let us go into more detail.

It happened!

And now, someone may be planning / plotting / threatening / bullying to sue you. “For everything you’ve got.”

A lawsuit is on the horizon and you are looking for an attorney. You knew!! that you should have done something before a “lawsuit” was more than just an “idle warning”…You gave it some serious thought, and even spoke to an attorney a while back. You intended to do it, later…but,…

“Later” became a week, then a year, and now it has been at least three years. And, it just never got done.

Sound familiar?

THAT DYSFUNCTIONAL LEGAL SYSTEM. Contingent fee lawyers make a living off what they can extract from their targets, and there’s 100K more graduating from law school every year. It’s nothing new to you. You heard someone-else’s horror stories, divorce stories, victim stories. You just did not expect it – to become your story.

The internet is full of information. With every lawyer claiming they have the best solution. Who can you trust?

My 45 years of personal experience dealing with lawyers and lawsuits in business, right down to the “nuts and bolts” of wealth protection strategies for business owners.

REMOVE THE INCENTIVE TO SUE YOU

It’s all about giving your creditor two (2) options:

option #1. You dictate the terms of settlement to your creditor.

OR

option #2. You threaten to file for bankruptcy, and your creditor gets NOTHING.

Everything must stop, all creditor demands must stop, once you file for bankruptcy.

Which is better, diarrhea or throwing-up?

The nuts and bolts

REMOVE THE INCENTIVE TO SUE YOU

the nuts and bolts:

Our Ultra Trust® locked to a Derivative Financial Instrument™

INFORMATION BROKERS CAN’T FIND YOU. INTERNET SEARCHES, ARE USELESS.

Our System

For the most part, professional internet information brokers use your social security number. A properly implemented plan, will not use your social security number, rendering internet information broker asset searches, useless.

————————–

You see the writing on the wall.

You’re not certain if this litigation is going to begin in a month, six months, or year; but you definitely feel the stress related to it. The thought is consuming and dominating your daily life. If you have never gone through this nightmare, I can tell you: … IT’S EXHAUSTING.

Our system is financially engineered to be the best methods to protect against unscrupulous lawyers, internet prying eyes about you, your family, your finances, scam artists, identity thieves, and other con-artists, and “I’m from the Government and I’m here to help you” because it addresses all potential problems that can cause a structure to be to be unwound.

90% of the time, the biggest problem is with fraudulent transfers. “Fraudulently transferring” property is merely giving a gift to the trust or any 3rd party. Every state requires 4 years to pass before they consider a gift to be “completed.” That’s called the “statute of limitations.”

This ominous fact is because regardless of what structure that you use, whether it be a limited partnership (LP), a family limited partnership (FLP), a domestic Limited Liability Company (LLC), a domestic corporation, a domestic Sub S corporation, or even an offshore trust, if the judge sees that your transfers were without fair market consideration (i.e. you never got paid a fair price for them when you gave them away), they can be clawed back by the court.

Something this stressful, like a threat of a lawsuit, gets some people so overwhelmed with fear and anxiety that it causes them an inability to take action. They think that if they keep pushing it aside, and bury their head in the sand, that the problem is somehow going to go away on its own.

We receive calls when its too late to help someone at least a dozen times every year. Mike originally reached out to us at a time that there was a high risk of a court battle coming, but nothing was set in stone yet. Because he hadn’t actually been served papers indicating that he’s been sued, he thought there might be a chance that there may never be a lawsuit, so he decided to hold off taking action to avoid the cost.

A few months later, he found out through a series of bounced checks that his bank accounts were frozen. The creditor got a preliminary judgment and brought it to his bank, freezing the accounts without his knowledge.

At that point, not only was there nothing that anyone could do, but he couldn’t even access funds to retain a defense attorney, because all of his money was frozen.

The most powerful weapon in the hands of the Creditor plaintiff:

The Pre-Judgement Attachment

This remedy is used to freeze all property (cash, near cash, broker accounts, real estate, etc.) of the Defendant to prevent the transfer, spend-down, or liquidation. The Plaintiff merely has to demonstrate the likelihood that he will win at trial.

You cannot deposit rents or income, pay your bills, run your business or withdraw your money. Your residence, rental property, or business can also be attached, and your property cannot be sold or refinanced. Judges are shockingly flexible and very democratic against defendants with things to share … … …the politically correct way to say this is the redistribution of (your) wealth. At that point, you have No leverage, No room to negotiate, nothing to talk about or discuss … They’ve Got You. You’re screwed to the wall.

The truth of the matter is that the stacked legal system is full of political appointees that may not be aware of every related legal precedence; they could be acting solely in their emotional judgement. The way they see it, is that you will get a chance at trial to prove your case so there is very little risk to them in issuing that Pre-Judgement Attachment.

You don’t have to go through what Mike went through. You don’t have to become a vulnerable victim subject to your plaintiff’s “back-up the truck and take what you want” mentality.

DOES YOUR CREDITOR/PLAINTIFF HAVE A CASE?

There are many kinds of creditors with really only 2 different objectives: Your creditor/PLAINTIFF is either in the business of:

1. Extracting of your money, because he sees an opportunity

2. Creating the maximum grief, regardless of cost, because he sees an injustice.

Your creditor’s first response is googling “contingent fee lawyers.” These are local entrepreneurs with a law degree and a state license. They realized that they could get many more clients if they did not charge a fee up front, but rather collect only when they provide results. “No recovery = No fee.”

They will not take a case unless there’s a short-term recovery.

Personally, I was a contingent fee entrepreneur in the real estate tax abatement business for decades. I knew exactly my costs based on my experience (knowledge) of hundreds of cases. And, I knew exactly my expected outcome.

The experienced contingent fee lawyer, knows exactly because:

“No recovery = No fee.”

Your Creditor/Plaintiff has the advantage within the politically correct legal system. Assuming that you can’t find a contingent fee lawyer, and because the creditor / plaintiff wants to inflict pain or seek justice, or other destructive motivations, they can hire a fee-for-service lawyer.

The fee-for-service lawyer has a different model and a different objective:

Run the clock.

When he interviews you, the plaintiff, for the “free initial consultation” he offers you NO advice unless you sign a contract and pay a retainer. His objective is his new Mercedes, next vacation, or his kid’s college education.

Easily, your legal expenses can amount to $50- $100,000.

Your creditor/plaintiff’s objective is to: delay, delay, delay. File motions, new motions, discovery, interrogatories, depositions, subpoenas, face to face interrogation, examination before trial, expert witnesses, continue your case, delay, delay, delay, any potential trial date, or settlement.

The legal system aids, encourages, and facilitates your fee-for-service lawyer.

If you are on the receiving end: it’s a living, extremely-long, exhausting, nightmare.

BUT… I’m sure you’re thinking, “well, by using an offshore trust, the judge doesn’t have any jurisdiction, so a ‘judgment’ is not executable and “it’ll be fine” and you’d be partially right… except for one small detail:

1. Offshore trusts typically cost $5-10,000 a year to maintain

2. If you have committed a fraudulent transfer, most judges now put you in jail until you comply with a court order to bring the money back into the United States.

Offshore trusts for real estate work even less well:

Real estate that is physically located in a state that the court does have jurisdiction (even if the property is owned by an offshore trust), can be unwound if it is found that you gave up the property without getting anything for it.

And while setting up a structure and transferring property into it well before a problem arises is the best advice, the issue of “fraudulent transfer” still will come up because there is a 4-year statute of limitations for any transfer if you do not get paid for it.

This means that, even if you take action before a lawsuit happens, but less than four years from the transfer of the property, you could still be at risk of a fraudulent conveyance claim. So, if you take the wrong advice from an attorney, you could lose more than “just money,” you could be held civilly and criminally liable taking advice from every 3rd lawyer who claims to be “the Expert.” Most lawyers use the “gifting method” to transfer money or property. “GIFTING” is a Fraudulent Conveyance.

Under the Uniform Fraudulent Transfer Act you would be committing a crime, see Section 19.40.041

…. (a) a transfer made or obligation incurred by a debtor is fraudulent as to a creditor whether the creditor’s claim arose before or after the transfer was made or the obligation was incurred, if the debtor made the transfer or incurred the obligation: (1) with actual intent to hinder, delay, or defraud any creditor of the debtor.”…

Your lawyer could also be held liable, and possibly lose his license under the theory for civil conspiracy:

————————–

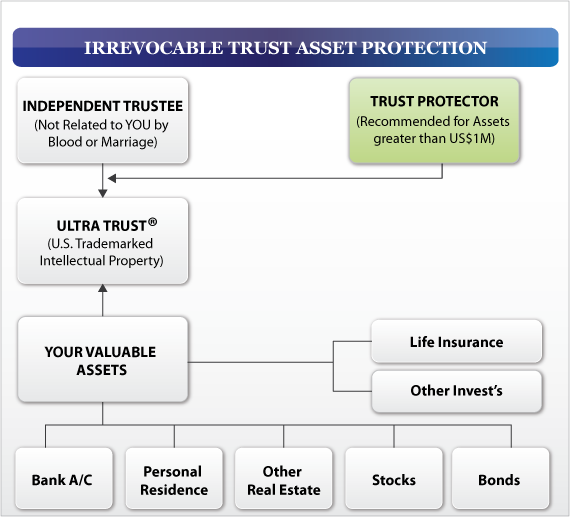

Ultra Trust®

Irrevocable Trust

Our Ultra Trust® is an intellectual property right registered with the U. S. Patent Office and one of the best methods available. Financially engineered to remove yourself from the probability of becoming the next creditor victim. This whole website www.ultratrust.com is devoted to the best ways for business owners to safeguard their wealth and the Ultra Trust® Irrevocable Trust has been developed by our expert attorney’s with 30+ years of experience and hundreds of court challenges.

NOTE: Properly implemented, your Social Security Number is not used. The IRS legal entity is separate from its owners. Comprehensive fee for service information / property search brokers will NOT be able to Earn a Fee.

“No find. … No Lawsuit. …No fee.”

Information is “Power.” Knowledge and Skill is “Significantly MORE Powerful.” (Rocco Beatrice, Sr.)

The Vanderbilts, Rockfellers, Carnegies, and other aristocratic or super-wealthy, have successfully shielded themselves from public prying eyes, identity thieves, scam artists, and other con-artists for generations.

Don’t underestimate your risk. Remove yourself from the probability of becoming the next creditor victim.

If a contingent fee (savvy business entrepreneur) lawyer determines that there are insufficient funds to pay a judgment, in all likelihood, the lawsuit will NOT be commenced.

What’s a Trust?

Any attorney will tell you that a “TRUST” is nothing more than a “CONTRACT” between the person who wants to protect wealth (the Settlor), the person who will manage the assets (the Trustee), for the benefit of all Beneficiaries – whomever you choose.

The Trust Agreement requires the transfer of property to be protected from the original owner (Settlor) to a legal entity for the purpose for which the Trust Agreement was created.

Think of it as a

shoe box

. (the [T]rust)

All your stuff in your shoe box, is protected: your house, your bank accounts, broker accounts, CDs, your Business(es), autos, life insurance policy, and other valuables … including your sub S shares, and your LLC membership units.

Your [I]ndependent [T]rustee (not related to you by blood or marriage) is the care-taker of your shoe box. His job is to act as your [F]iduciary, to protect your shoe box, at any cost. Read more about fiduciary: https://en.wikipedia.org/wiki/Fiduciary

The [B]eneficiaries are the people that can use the stuff in the box: you, your spouse, your children, … anyone you wish. Like renting a car, you use it, you bring it back. You do NOT OWN the stuff in the box (you don’t own the car, you are merely renting the car).

Implemented correctly: you cannot be compelled to act, because you have no ownership and no control.

Protecting your STUFF can only be done with an Irrevocable Trust, with an Independent Trustee.

IRREVOCABLE TRUST

What type of trust, Grantor, or Non Grantor? What’s the distinction? A ‘Grantor’ Trust acquires a special regulation/loophole consequence within the IRS tax code.Our Ultra Trust® is an “Irrevocable Grantor Trust” for tax purposes is treated as a ‘disregarded’ legal entity. The IRS disregarded entity is “Income Tax Neutral” meaning that the original Grantor retained strings attached, so that for purposes of the IRS income tax reporting, the original owner (grantor(s) retains the property in his complete control, thus our Ultra Trust® is a “pass-through” to your form 1040 i.e. real estate tax deduction and mortgage interest deduction on his personal income tax return, INCOME TAX NEUTRAL.

Revocable, Irrevocable trust, what’s that mean? Revocable is when the original person with the property transfers (repositions) the money to a trust with strings attached. The Grantor, the Trustee, and the Beneficiary are the same person. Effectively you have done nothing, because it’s between you and you for the benefit of you.

A revocable trust does absolutely nothing to protect property because you can be forced to revoke it by a creditor or court. Many lawyers recommend revocable trusts for avoiding probate, recognizing that the trust is not worth the paper it’s written on for protecting property against frivolous lawsuits and the avoidance of estate taxes or the five-year Medicaid spend-down provisions.

IRREVOCABLE TRUSTS ADVANTAGES

A properly written, executed, and funded irrevocable grantor trust, such as the Ultra Trust®, is an extremely powerful shield. The opposite of revocable is “irrevocable.” No strings are attached by the Grantor. An “Irrevocable” trust advantages includes the fact that nobody can force you to revoke it, and thus if written, executed, and funded correctly, provides one of the best methods available.

Once funds are transferred from the Grantor(s) to the Irrevocable Grantor Trust, the Grantor has no control, other than possibly some very limited powers. It’s this clear-cut lack of control and ownership that makes this trust a very powerful methodology – yet another one of the irrevocable trust advantages. You can’t be sued for things you no longer own or directly control. The fiduciary duty of an independent trustee of an irrevocable grantor trust is critical and viewed by the courts as golden (read more https://en.wikipedia.org/wiki/Fiduciary). The Trustee must preserve the assets entrusted to him at any cost. Courts take a very unpleasant view on a Trustee who has abused his fiduciary duty. Breach of fiduciary duties by a Trustee could be considered and intentional tort subject to punitive damages.

OUR irrevocable Ultra Trust® when combined with a Limited Liability Company (LLC) or Family Limited Partnership (FLP) is a fortress, short of a foreign trust. A foreign irrevocable trust combined with the derivative financial instrument is the Rolls Royce – expensive to set up and maintain every year, but when properly executed, the creditor must restart a lawsuit in the new jurisdiction. The domestic irrevocable trust with an LLC and the derivative financial instrument to avoid a fraudulent transfers is the Tesla of asset protection – not inexpensive to set up, but minimal maintenance costs and if written, executed, funded correctly, 99.9% as strong.

NOTE: Our Ultra Trust® is the only entity that can hold sub S stock and LLC membership units. IRS has onerous rules.

WHAT’S A TRUST PROTECTOR? You won’t get this from your lawyer

Because you are concerned about the power and discretion granted to the Trustee, we add the Trust Protector to create the checks and balances you need to feel comfortable, while reinforcing the bullet-proofing of our Ultra Trust®.

The power of the Trust Protector is derived from the Irrevocable Grantor Trust Contract. The Agreement sets forth the dual function of the Trustee and the Trust Protector to give you a backup plan if the Trustee is not cooperative. While the Trustee can be a bank, CPA, trust company, or other financial institution, the Trust Protector is usually a person close to the family, a CPA, accountant, or lawyer who is already the family consiglieri.

The Trust Protector’s powers can take any form, limited only by the wishes of the Grantor(s) and their imagination. Generally, the powers granted the Trust Protector are:

1. Ability to remove or replace the Trustee without any explanation “You’re Fired.” Often this is the only power granted to the Trust Protector. In cases where the Trustee is a corporate body (bank, trust company, insurance company, or professional trustee) if the Trustee is unresponsive or not performing to the Trust Agreement for the benefit of all Beneficiaries, or changes in management, or investment choices, the Trust Protector can fire and replace the Trustee, at will, without explanation to the current Trustee.

2. Ability to change the Trust’s situs to take advantage of law changes or necessary steps to act in the best interest of beneficiaries if they move from low tax states to high tax states, i.e. from CA or NY (high tax states) to NH, TX, or NV (low tax states) or changes in laws occurring long after the initial implementation of the Trust Agreement.

3. Ability to resolve deadlocks between co-trustees or in squabbling between the Trustee and/or Beneficiaries.

4. Ability to veto spending over a certain amount. This level of control is significant if disbursements of the Trust are in excess of a pre-arranged amount requiring two signatures, the Trustee and the Trust Protector i.e. in excess of $20,000.

5. Ability to veto distributions to Beneficiaries. Before distributions are to occur the Trust Protector may want to investigate the financial stability of the Beneficiaries. For example, if the beneficiary is being sued, The Trust Protector may withhold distributions, or the Beneficiary is undergoing divorce proceedings, or the Beneficiary may be too young, is under duress, mentally incompetent, unable to manage, or otherwise unavailable. The Trust Protector can override/veto the Trustee and withhold distributions temporarily or permanently make other arrangements such as buy the property necessary for the benefit of the beneficiary (buy a house, a car, sign a rental agreement, but have the Trust own the properties, make loans, or make other provisions.

6. Ability to veto investment decisions. This checking and balancing of investment decisions are based on the Trust Protector’s experience, prudence, and the Trust Agreement guidelines in protecting the wealth for the Beneficiaries.

7. Ability to sue and defend lawsuits against the Irrevocable Trust. The fiduciary duty of the Trustee and The Trust Protector has to save the property of the Trust, at any cost, for the benefit of all classes of Beneficiaries.

8. Ability to terminate the Irrevocable Grantor Trust is another of the Irrevocable Trust advantages. If in the opinion of the Trust Protector there are insufficient funds or the cost of administration is greater than available cost/benefit, the Trust Protector may terminate the Trust.

The Trust Protector’s role is created by the Trust Agreement to add an additional layer of protection and is usually a person most familiar with the Grantor’s long term financial and personal goals. A Trust Protector usually is the balance of power between the Trust Agreement, the Trustee, The Grantor, and the Beneficiaries. Neither the Trustee or the Trust Protector should be anyone related to the family by blood or marriage. Both positions should be independent of each other acting in the long-term interest of the beneficiaries.

Derivative Financial Instrument™

What is it? It’s a linked financial investment, estate planning services. The formation, development, and implementation of a ‘personalized’ investment of funds strategy(ies) for individuals, linked to a private investment contract that derives its value from the performance of an underlying class of assets, i.e. cash or near cash, a futures contract, an option, collateralized debt obligation, insurance contract, a credit default swap, a stock, a time deposit, a general debt obligation, bonds, mortgages, or any underlying property used as the medium of exchange between third parties to a financial instrument.

The Derivative Financial Instrument is the most critical part of planning that every attorney overlooks, but it is crucial to the success of any asset protection strategy for business owners.

The Derivative Financial Instrument™ is a financial intermediation of a contractual method of [E]xchange in money or money’s worth, designed and implemented, to avoid fraudulent conveyance claims by a [P]ast; [P]resent; and a [F]uture (not yet born) creditor.

The Derivative Financial Instrument™ is the most critical decisive component to our Ultra Trust®

The Derivative Financial Instrument™ is engineered for estate planning to avoid the [T]trigger for: – IRS income taxes, gift taxes, estate taxes, and probate.

When timely and properly implemented, the Derivative Financial Instrument™ will set the legal defense for potential civil conspiracy issues that may be advanced by the [P]ast; [P]resent; and [F]uture (not yet born) creditor.

The Derivative Financial Instrument™ is a restricted long-term personalized estate planning investment of funds strategy for individuals using a cash – asset class derivative contract executed at “fair market value,” non-marketable, non-amendable, non-assignable, non-transferable, non-anticipated, non-encumberable, whose market value is derived from the underlying property, indexed to an IRS supported interest rate, terminating at death.

Our Ultra Trust® is an Irrevocable Grantor Trust under Internal Revenue Code (IRC) 671-679 and IRS Regulation 7701-7 provides one of the absolute best wealth protection approaches. When implemented with an Independent Trustee, and an Independent Trust Protector, secured to a Derivative Financial Instrument™, ourUltra Trust® is financially engineered to avoid Fraudulent Conveyance claims, defend a claim of Civil Conspiracy, eliminate the Probate process, eliminate Estate Taxes, mitigate and eliminate the Medicaid and/or Medicaid state recovery under the Federal Medicaid Act 42 USC 1396 et. Seq., providing you with a secured unchallengeable estate plan that results in one of the strongest wealth protection approaches available.

Unchallengeable Estate Plan: The Ultra Trust® combined with the Derivative Financial Instrumentis One of the Strongest Methods for Business Owners

DESCRIPTIONS

Derivative:

In finance, a “derivative” is a contract that derives its value from the performance of an underlying entity. The underlying entity can be a class of assets, i.e. cash or near cash, a futures contract, an option, collateralized debt obligation, insurance contract, a credit default swap, a stock, a time deposit, a general debt obligation, bonds, mortgages, or any underlying property used as “the medium of [E]xchange.”

Intermediation:

Intermediation is the process of matching positives with negatives to develop a desired outcome in a new contractual obligation method of [E]xchange between third parties.

The underlying entity(ies) considered in the Derivative Financial Instrument™:

Estate Planning

Gift Taxes

Intentionally Defective Grantor Trust (IDGT)

Grantor Retained Annuity Trust (GRAT)

Grantor Retained Unitrust (GRUT)

Commercial Annuity

Private Annuity

Installment Sale

Self-Canceling Installment Note (SCIN)

Treasury General Counsel’s Memorandum (GCM) 3953, May 7, 1986

Estate of Moss v. Commissioner, T.C. 1239 (1980) acq. in result, 1981-2 C.B.1

Estate of Costanza v. Commissioner, T.C. Memo 2001-128; reversed and remanded

6th Circuit, No. 01-2207, February 18, 2003

Estate of Frane v. Commissioner, 998 F. 2nd (8th Circuit 1993)

Lazarus v. Commissioner, 58 TC 854, August 17. 1972

Estate of Musgrove, 33 Fed Cl. 657 (1995)

Estate of Kite, T.C. Memo. 2013-43

Estate of William M. Davidson, U.S. Tax Court Docket No. 013748-13

United States v. Davis, 370 U.S. 65 (1962)

International Freighting Corp. v. Commissioner, 135 F.2d310 (2nd Cir. 1943),

United States v. General Shoe Corp., 282 F.2d 9 (6th Cir. 1960);

Wood v. Commissioner, 39 T.C. 1 (1962)

CCA 201330033; Treas. Reg. § 25.2512-8

Revenue Ruling 80-80, 1980 1 C.B. 194

Revenue Ruling 55-119, 1955 – 1 C. B. 352

Revenue Ruling 86-72, 1 C.B. 253

Revenue Ruling 68-392, 1968 -2 C. B. 284; and 69-74, 1969-1 C. B. 43

Treasury Regulation 1.1275 4(c); (j); and § 25.7520-3

Treasury Regulations § 1.72-6(e); and 1.1001-1(j), October 2006

Life expectancy (determined under Reg. 1.72-9, Table V)

Federal Medicaid Act 42 USC 1396 et. Seq.

Internal Revenue Code (IRC) 72; and (IRC) 7520

Fair Market Value:

Fair market value is defined as “the price at which the property would change hands (the [E]xchange) between a willing buyer and a willing seller, neither being under any compulsion to buy or sell and both having reasonable knowledge of relevant facts to the transaction.” The fair market value of the Derivative Financial Instrument™ is generally determined under the annuity tables prescribed by the IRS. See 26 U.S.C. 7520(a); Treas. Reg. 20.7520-1. These tables provide a factor composed of an interest rate component and a mortality component that is used to determine the present value of an annuity. Treas. Reg. 20.7520-1.

Fraudulent Conveyance:

A fraudulent conveyance, or fraudulent transfer, is an attempt to avoid debt by transferring money to another person or company. In civil litigation the creditor attempts to void the transfer and make the property available to him in satisfaction of his claim.

A transfer will be fraudulent if made with actual intent to hinder, delay or defraud any creditor. Thus, if a transfer is made with the specific intent to avoid satisfying a specific liability, then actual intent is present. However, when a debtor prefers to pay one creditor instead of another that is not a fraudulent transfer.

Under the Uniform Fraudulent Transfer Act, you would be committing a crime, see Section 19.40.041

…. (a) a transfer made or obligation incurred by a debtor is fraudulent as to a creditor whether the creditor’s claim arose before or after the transfer was made or the obligation was incurred, if the debtor made the transfer or incurred the obligation: (1) with actual intent to hinder, delay, or defraud any creditor of the debtor.”…

Fraudulent conveyance has to do with transferring property at “less than the fair cash value” thereby defrauding a potential creditor or the “intentional divesting of money/wealth” which would have been available for satisfaction of his creditor claim. This intentional disregard can become a sticky-wicky for a judge who does not like to be undermined in “his” court-room.

Civil Conspiracy:

The “civil conspiracy theory” has been defined by the courts as: (1) an agreement (2) by two or more persons (3) to perform overt act(s) (4) in furtherance of the agreement or conspiracy (5) to accomplish an unlawful purpose /or/ a lawful purpose by unlawful means (6) causing injury to another.

To be convincing, the creditor must allege not only the conspirators committed the act but also the act was tortious in nature. The conspiracy alone is not enough to trigger a claim for civil conspiracy without the underlying tort.

Avoiding the “Trigger:”

Gifting, by definition, is a Fraudulent Conveyance or Fraudulent Transfer because there is NO Exchange at the fair market value. The Derivative Financial Instrument™ solves this problem because the [E]xchange is at the fair market value.

REMARKABLE: The Derivative Financial Instrument™ is a contract for which, NOT EVEN BANKRUPTCY COURT CAN UNWIND because it’s at Fair Cash Value and not to the detriment of the Creditor. The Derivative Financial Instrument™ protects the funds/wealth even after the owner loses a lawsuit. This is because the courts cannot set aside the purchase . . . it’s not voidable by a creditor as a fraudulent transfer, nor by a bankruptcy court as an “executory contract.” The result is one of the best ways for small business owners to guard their wealth.

The “Trigger” for Estate Taxes is the value of ALL assets owned by the individual at the DATE OF DEATH, “the Gross Estate.” Our Ultra Trust® ELIMINATES the “Trigger” because on the Date of Death, ALL assets are owned by your Ultra Trust® Irrevocable Grantor Trust with an independent Trustee, and Independent Trust Protector. You cannot file an estate tax return. You cannot Trigger the estate tax return, you own nothing on the date of your death. Your Gross Estate is below the taxable threshold. It is the ultimate in wealth protection approaches that is not offered by your attorney.

We look forward to our visit with you and your professional representatives to assist you with the advancement of your estate planning.

Cordially,

Rocco Beatrice, CPA (Certified Public Accountant), MST (Master of Science in Taxation), MBA (Master of Business Administration), CWPP (Certified Wealth Protection Planner), CAPP (Certified A/P Planner), CMP (Certified Medicaid Planner), MMB (Master Mortgage Broker)

Managing Director, Estate Street Partners, LLC

Riverside Center Building II, Suite 400, Newton, MA 02466

“Helping our clients resolve their problems quickly, effectively, and decisively.”

The Ultra Trust® “Precise Wealth Repositioning System”

This statement is required by IRS regulations (31 CFR Part 10, 10.35): Circular 230 disclaimer: To ensure compliance with requirements imposed by the IRS, we inform you that any U.S. federal tax advice contained in this communication (including any attachments) is not intended or written to be used, and cannot be used, for the purpose of (i) avoiding penalties under the Internal Revenue Code or (ii) promoting, marketing or recommending to another party any transaction or matter addressed herein.