If you are like most of us, you want to invest over the long haul, buying the best mutual funds to invest in and not have to worry about it. Most people automatically make an assumption that growth stock mutual funds will provide the best returns over the long run. Often times this is a poor assumption, but in our research we found the best mutual funds to invest in were, in fact, growth stock mutual funds, but let us not forget, retirement investing is for your long term retirement goals, so you want to make the most of every dollar you put in there, so you can have enough money to retire… maybe even retire early.

Kiplinger puts out a great list of best performing mutual funds to invest in (10 years). They actually look at the best mutual funds to invest in during the last year, the last 5 years, 10 years and 20 years, but let us not digress. Their analysis is purely from a statistical perspective; e.g. which funds averaged the best returns. No doubt that it might be fun to take a look at the best mutual funds to invest in for the last year. Here one will often find growth stock mutual funds that had large investments in some of the highest-appreciating stocks and “got lucky.” The true testament comes for the funds that can endure and consistently outperform year in and year out through full business cycles. A full business cycle being about 5-7 years on average. (we will later explain how we define a full business cycle)

Best Growth Stock Mutual Funds to Invest In

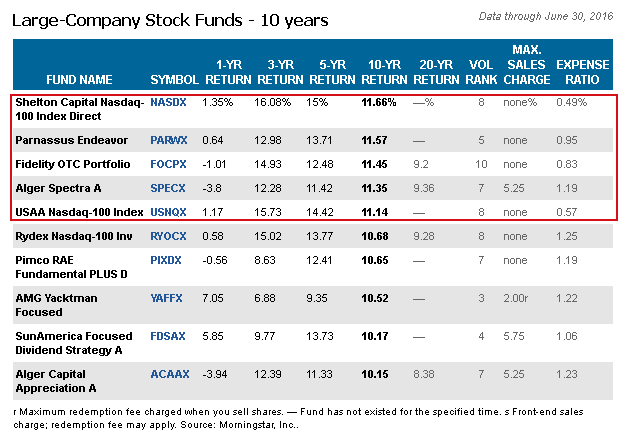

Large company stock funds over last 10 years. Data through June 30, 2016. Source: Morningstar, Inc.

Therefore, since our time horizon for this analysis is 10-15 years, we are most interested in the best performing mutual funds (10 years) over the long run. Those mutual funds to invest in which, don’t just get lucky one year, but have the skills to “get lucky” year in and year out selecting their stocks and getting out at the right time as well. Most growth funds often have a year of outperformance and maybe even 2 or 3 years. One would suggest that their outperformance really goes from “getting lucky” to actually having real talent with stock picking. However, the most skilled managers of growth stock mutual funds do it year in and year out in up markets and down markets.

By selecting the 10-year timeframe to focus our attention on, we’re looking for those best performing mutual funds to invest in that actually have gone through a major market down-turn like the one that occurred in 2008 when the S&P500 was down 37%. 2008 was one of the most painful periods for most people in their 401K. How did these funds perform during the most painful period in recent history? Did those growth stock mutual funds outperform the S&P500 during the tough years as well? Or were they susceptible to the same dips that the stock market tends to have at least once every business cycle?

Critical Big Picture Fact:

Since the year 1900 there have been 19 recessionary periods. That is one recessionary period every 6.1 years on average. The last one occurred in 2008/9.

Each one of these recessionary periods resulted in a 20%-80% loss in the S&P 500. Currently, we are 8 years from our last recessionary period.

The top 5 best performing mutual funds (10 years) illustrated have all had returns that have averaged over 11%. We can tell you this is great, but not as great as some tactical private wealth management funds that we have learned about.

What is the difference between a tactical private wealth management fund and a mutual fund?

A tactical private wealth management fund and a mutual fund both invest in underlying securities such as stocks, bonds, mutual funds, and ETFs and they both offer sector-type fund options (dividends, real estate, municipal bonds, etc.). The biggest difference is that most mutual funds, as detailed in their prospectus by law, typically have to be fully invested regardless of how poorly the market is doing. Every mutual fund defines this slightly differently, but it tends to mean they are required to have be invested by a minimum of 80% of the assets in the underlying stocks/bonds they are investing in. That means that when the market is going down, the mutual fund must keep 80% of all of their assets invested in the market regardless, as stated by rule 35D-1 under the investment Company Act of 1940. Rule 35d-1 restricts a mutual fund manager from liquidating and protecting your money during downturns in the market because they must stay 80% fully invested. This does not necessarily mean the mutual fund manager is a poor stock/bond picker, but rule 35D-1 simply prohibits them from selling securities in a down market to protect your money. This is one of the dirty little secrets of the industry.

Through our research, we found that tactical private wealth management funds do not operate within the same guidelines and restrictions of rule 35D-1. Tactical private wealth management funds offer investors more flexibility to sell the market.

The Best Growth Stock Mutual Funds to Invest In: Is There Something Even Better?

The key point here is that there is no trigger for the mutual fund manager to get out. They are relying on you to sell the mutual fund or your broker to sell for you. The only problem is that your broker gets paid only when you are fully invested in the mutual funds. If s/he takes your portfolio to cash, s/he just cut their own salary. I don’t know too many people that would proactively decide to cut their own income. Therefore, a broker telling you “sell everything” to protect you from losses in the market rarely occurs.

When there is a big loss in your portfolio, your broker will typically tell you that you need to ride the ups and downs of the market because over the long run, stocks offer larger returns than most other asset classes. And your broker would be right over a 50-100-year period, but if you’re nearing retirement (5-10 years) or are already in retirement, you may not have the luxury of taking significant losses in your retirement account during these times. If you were planning on retiring in 5-10 years and you lost 40% of your retirement, you may be changing your plans to retire in 15-20 years. If you don’t love your job, then that could be a real slap in the face.

Our research indicates that tactical private wealth management funds are different.

Tactical private wealth management funds have the ability to get out of stocks/bonds in the blink of an eye. They typically use models that warn them when the markets are looking unstable or shaky in an attempt follow market trends. In uncertain times, they have the ability to get out of stocks and go to cash until their models tell them that all is clear and they are safe to invest again. Many of them have a great track record of avoiding major market disasters and because of it, their overall returns typically outperform Kiplinger’s best performing mutual funds (10 years) through a full market cycle.

Never Forget Warren Buffet’s Rules of Investing

If you recall the famous quote by Warren Buffet. There are 2 rules to investing money. Rule #1: Never lose money. Rule #2: Never forget rule #1.

The quote is obviously cute and silly on the surface, but it has a much deeper meaning.

The reason is math.

When you lose principle in any investment, you need to make more than what was lost just to get to break even. If you lose 40% in year 1, then make 40% the following year, you don’t get back to even – do the math.

For example, if Joe had $500,000 invested in the stock market and he loses 40%, he is left with $300,000. If he made back 40% in year 2, his nest egg would only increase to $420,000. In order to get back to $500,000, he would need to earn a return of 67% just to get back to breakeven. **These calculations are not including inflation or distributions you are taking to support your retirement needs.**

When you avoid big losses, the returns take care of themselves. That is why tactical private wealth management funds are typically so much better than even the best growth stock mutual funds.

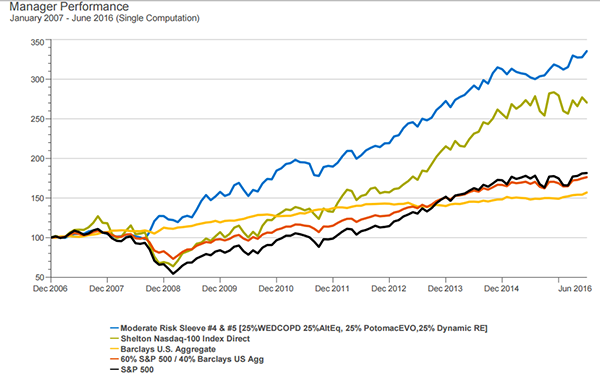

Let us compare some tactical private wealth management funds that we have found through our research with the #1 mutual fund in Kiplinger’s Best Performing Mutual Funds to Invest in (10-year period). These returns are all net of fees and expenses so we are comparing apples to apples. As you can see from the cumulative returns chart below. The private wealth management funds are the blue line, Kiplinger’s #1 on their list of best performing mutual funds to invest in (10 years) is olive, and the other lines are benchmarks such as the Barclays U.S. Aggregate bond fund in yellow, 60%/40% (S&P500/Barclays U.S. Aggregate) stock/bond mix in orange, and the S&P 500 in black. The average return for the tactical private wealth management funds through a full market cycle (analysis period) are higher by around 2.5% (13.59% vs 11.09%) over this 10-year period.

Kiplinger’s best performing mutual funds to invest in 10 year period. Source: Informa Business Intelligence Zephyr OnDEMAND

Kiplinger’s best performing mutual funds to invest in 10 year period. Source: Informa Business Intelligence Zephyr OnDEMAND

Manager vs Benchmark Return Jan 2007 to June 2016. Source: Informa Business Intelligence Zephyr OnDEMAND

Over 10 years the difference can be staggering. For example, if we start with $500,000 in Kiplinger’s top fund, and extrapolate 10 years with an average return of 11.09% your Kiplinger’s top fund investment will be worth $1,420,862. While the same extrapolation over 10 years with an investment in a tactical private wealth management fund we achieve a 13.59% average return and end up with $1,788,014. That is $367,000 more for the tactical private wealth management fund.

In reality, most retirees and pre-retirees are going to live through multiple business cycles. What does an extra 2.5% do for you over 20 years? Well for example, if we start with $500,000 and extrapolate 20 years with an average return of 11.09% we get $4,060,309 for Kiplinger’s top fund, not bad. While the same extrapolation over 20 years for the tactical private wealth management fund with 13.59% average return is $6,393,991. The tactical private wealth management fund returns $2.3M more. What could you do with an extra $2.3M? Perhaps you could retire a year or 2 earlier than you had planned, but, of course, we have to remember that past performance is never an indication of future results.

But as we said earlier, these comparisons really are not fair, because the tactical private wealth management funds do not have the same level of drawdowns as most mutual funds, especially the growth stock mutual funds, due to the fact that mutual fund prospectus restrictions don’t allow them to avoid big market losses, while tactical private wealth management funds can go to cash and avoid the big losses, while at the same time being able to take advantage of the market decline by putting their cash back to work in the market in near the lows. See the drawdowns over the last 10 years of the funds from below. During the depths of the 2008 crash the tactical private wealth management funds were down about 11% while the Kiplinger’s Top Fund (NASDX) at its lows was down a full 50% during the same period. Do you remember how losing 50% felt?

The drawdown report below shows how much each investment was down a during any given point in time within the market cycle. All of the funds we are analyzing are shown below.

Drawdown investment report displaying when markets were down at any given time. Source: Informa Business Intelligence Zephyr OnDEMAND

There is another great caveat here: the best performing mutual funds to invest in as reported by Kiplinger, are high risk / high return growth stock mutual funds. The tactical private wealth management funds described herein are only moderate risk funds that typically trade with 50% less risk than the market (S&P 500). This is reflected in the drawdown report above, but one must seriously consider the amount of risk they are taking in order to achieve the returns they are getting. In the world of low interest rates and the everlasting reach for yield, one must consider the quote by the founder of PIMCO and current Janus Fund Manager, Bill Gross:

“At some point you should not worry about the return on your money, but rather the return of your money.”

Being 8 years into a business cycle does not leave much time for one to consider their options in the authors opinion. Estate Street Partners is not an investment advisory firm, but if you would like to learn more about tactical private wealth management funds, we can refer you to an appropriate advisor. Call us today for more information at (888) 938-5872.

We look forward to our visit with you and your professional representatives to assist you with the advancement of your estate planning.

Cordially,

Rocco Beatrice, CPA (Certified Public Accountant), MST (Master of Science in Taxation), MBA (Master of Business Administration), CWPP (Certified Wealth Protection Planner), CAPP (Certified Asset Protection Planner), CMP (Certified Medicaid Planner), MMB (Master Mortgage Broker)

Managing Director, Estate Street Partners, LLC

Riverside Center Building II, Suite 400, Newton, MA 02466

tel: 1+888-938-5872 +1.508.429.0011 fax: +1.508.429.3034

email:

“Helping our clients resolve their problems quickly, effectively, and decisively.”

The Ultra Trust® “Precise Wealth Repositioning System”