Asset Protection

This Asset Protection archive brings together articles that help readers understand the moving parts behind stronger planning, from core definitions to more advanced structural questions.If you…

Explore Irrevocable Trust articles focused on practical questions, deeper explanations, and real-world planning issues that come up when families and owners are trying to make better trust and asset decisions.For a broader starting point, review Asset Protection Trust and then compare it with Revocable vs Irrevocable Trust for a more focused next step.

This topic archive is one part of the larger blog. Use the sections below to move into related categories, compare ideas more easily, and keep your research focused on the question that matters most right now.

Some readers begin with broad asset protection questions, while others jump straight into trusts, tax issues, Medicaid, divorce, or lawsuit exposure.

Explore asset protectionEach topic hub pulls together related articles so you can compare ideas more easily instead of bouncing between unrelated posts.

See how the process worksWhen you are ready, use what you learned here to ask better questions, clarify priorities, and decide which planning direction deserves closer attention.

Contact UltraTrustChoose the category that fits your current question, then move into detailed articles, comparisons, and next-step guidance gathered under that topic.

This Asset Protection archive brings together articles that help readers understand the moving parts behind stronger planning, from core definitions to more advanced structural questions.If you…

This Beneficiary of a Trust archive brings together articles that help readers understand the moving parts behind stronger planning, from core definitions to more advanced structural…

Browse Captive Insurance Structure articles focused on practical planning questions, comparisons, and next-step guidance.

Browse Derivative Financial Instrument Strategy commentary built to make complex planning topics easier to follow, especially when trust structure, ownership design, or family strategy needs a…

Explore Divorce articles focused on practical questions, deeper explanations, and real-world planning issues that come up when families and owners are trying to make better trust…

Read Estate Planning insights that connect technical trust ideas to real planning situations, with a practical focus on clarity, timing, and long-term decision-making.A useful way to…

Read Estate Planning and Trusts insights that connect technical trust ideas to real planning situations, with a practical focus on clarity, timing, and long-term decision-making.A useful…

This Financial Planning archive brings together articles that help readers understand the moving parts behind stronger planning, from core definitions to more advanced structural questions.If you…

Browse Grantor Trusts commentary built to make complex planning topics easier to follow, especially when trust structure, ownership design, or family strategy needs a closer look.Readers…

Explore Insurance articles focused on practical questions, deeper explanations, and real-world planning issues that come up when families and owners are trying to make better trust…

Explore Irrevocable Trust articles focused on practical questions, deeper explanations, and real-world planning issues that come up when families and owners are trying to make better…

Explore Irrevocable Trust Probate Protection articles focused on practical questions, deeper explanations, and real-world planning issues that come up when families and owners are trying to…

Browse Lawsuit commentary built to make complex planning topics easier to follow, especially when trust structure, ownership design, or family strategy needs a closer look.Readers who…

Browse LLC Advantages articles focused on practical planning questions, comparisons, and next-step guidance.

Browse Medicaid commentary built to make complex planning topics easier to follow, especially when trust structure, ownership design, or family strategy needs a closer look.Readers who…

This Nursing Home archive brings together articles that help readers understand the moving parts behind stronger planning, from core definitions to more advanced structural questions.If you…

Read Offshore insights that connect technical trust ideas to real planning situations, with a practical focus on clarity, timing, and long-term decision-making.A useful way to read…

This Prenuptial archive brings together articles that help readers understand the moving parts behind stronger planning, from core definitions to more advanced structural questions.If you want…

Browse Probate articles focused on practical planning questions, comparisons, and next-step guidance.

Browse Selecting a Trustee articles focused on practical planning questions, comparisons, and next-step guidance.

Explore Tax articles focused on practical questions, deeper explanations, and real-world planning issues that come up when families and owners are trying to make better trust…

Browse Trust and Asset Protection commentary built to make complex planning topics easier to follow, especially when trust structure, ownership design, or family strategy needs a…

This Trust Planning Professional Services archive brings together articles that help readers understand the moving parts behind stronger planning, from core definitions to more advanced structural…

Read Trust Protection insights that connect technical trust ideas to real planning situations, with a practical focus on clarity, timing, and long-term decision-making.A useful way to…

Explore Trusts articles focused on practical questions, deeper explanations, and real-world planning issues that come up when families and owners are trying to make better trust…

Read UltraTrust insights that connect technical trust ideas to real planning situations, with a practical focus on clarity, timing, and long-term decision-making.A useful way to read…

Browse Uncategorized commentary built to make complex planning topics easier to follow, especially when trust structure, ownership design, or family strategy needs a closer look.Readers who…

Read Wealth Management insights that connect technical trust ideas to real planning situations, with a practical focus on clarity, timing, and long-term decision-making.A useful way to…

These articles stay focused on this topic so you can compare ideas, definitions, and examples without leaving the same subject area.

📋 Key Takeaways A properly structured irrevocable trust can protect assets from IRS collection — but only when funded before any tax liability exists,…

📋 Key Takeaways Business owners face personal liability from two directions: direct personal liability and pierced entity liability — and an LLC alone does…

You're protected! If you are sued after properly transferring assets to an irrevocable trust — and the transfer was not a fraudulent conveyance —…

Yes — a fraudulent transfer claim can undo irrevocable trust protection, but only if the trust was funded after a creditor claim arose, while…

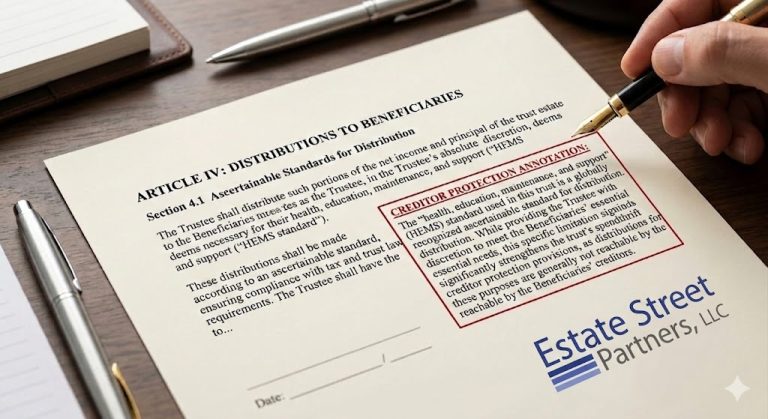

Top 7 Distribution Standards for Irrevocable Trusts: A Complete Guide When you've built substantial wealth, the way distributions flow from your trust can either…

An ascertainable standard in a trust is a legal provision that limits a trustee's discretion to make distributions to beneficiaries to specific, defined purposes…

Introduction: Understanding IRS-Compliant Asset Protection and Wealth Strategies IRS-compliant asset protection and wealth strategies are the disciplined, lawful methods high-net-worth families use to preserve…

Generally, no — a creditor cannot seize assets held in a properly structured irrevocable trust. Once assets are legitimately and irrevocably transferred to an…

No. A living trust does not protect your assets from a lawsuit. This is one of the most dangerous and widespread misconceptions in estate…

[embed]https://www.youtube.com/watch?v=dAe7RflVKUk[/embed] If you are a physician, surgeon, anesthesiologist, or any other licensed medical professional practicing in the United States, you are one of the…