In the realm of financial planning, creating a trust can be one of the most important steps in terms of achieving solid asset protection and designing an adequate estate plan. It doesn’t have to be a difficult process, but it does require thoughtful consideration and planning.

Choose the right legal or financial professional to Protect your Wealth for your family

Most individuals, and even most estate planning attorney’s unfortunately, are not familiar with estate law and how statutes can affect estate planning across different jurisdictions. It is unreasonable to expect someone who is not a legal or financial professional to be able to easily understand everything; however, certain key aspects of it can be sufficiently learned so that a do-it-yourself option becomes available.

The following 15 key points are of the essence when creating a trust. Once this information is fully understood, potential grantors will understand how to the point that they can begin the process of setting one up themselves.

1 – The Need and Purpose

They were originally created when the Renaissance period reached the nascent common law system of the English royal court. These legal instruments were born out of an important necessity: when English knights marched across Europe as Crusaders, they conveyed property ownership to trustworthy individuals to handle affairs such as managing land, paying feudal dues, etc. If the knight did not return to England after a battle, the terms of the entity would establish that the estate would transfer to beneficiaries, who were usually the spouse and children. In the absence of a structure, the Crown would simply claim royal rights over the deceased knight’s property, often leaving his surviving spouse and family penniless.

Good asset protection is like a puzzle placing together the right pieces in the right place

The historic needs of legal structures have not changed. They are still legal documents that establish a fiduciary relationship whereby personal ownership of assets is relinquished and the property is transferred so that it can be managed by a trustee for the benefit of others.

The modern purposes of these entities are: asset protection, wealth management, avoiding probate, Medicaid planning, and estate planning. Individuals and couples whose assets including real estate are worth more than $100,000 should consider creating a trust for their own benefit and to protect the financial futures of their loved ones. Please note, that only an irrevocable version protects assets from anything other than probate.

2 – The Laws and Rules Governing

In the United States, these entities fall under the laws of property, which can be different from one state to another. The most important aspects of them that can differ from one state to another are: validity, construction and administration. Validity deals with state-specific laws and rules that may render it invalid from one jurisdiction to another. For example, at one point many states adopted a rule against perpetuity, which is intended to prevent legal instruments from placing restrictions on property for too long; however, states such as Florida allows property interest that is non-vested to remain for 360 years instead of the suggested uniformity of 21 to 90 years.

Although there seems a fair amount of uniformity in terms of the laws that govern most estate planning across all states, it is imperative that individuals who set one up in one state to draft new documents when they move to another state or make sure that it’s amendable to change the situs. Once someone learns how to create one, the second time around will be substantially easier.

3 – Parties Involved

This structure create legal relationships that require at least three parties: grantor (also known as settlor), trustee and beneficiary. Each of these parties can be represented in plurality, which means that there can be more than one grantor, trustee, and beneficiary.

When learning about how to create one, the grantor must assume a decision-making role that includes certain responsibilities such as choosing the type, appointing the trustee, naming the beneficiaries, relinquishing property, and transferring the assets. Depending on the type and the way the assets are transferred, the grantor may incur into gift taxes; nonetheless, skilled advisors can come up with a strategy that can alleviate this financial burden even if your estate exceeds the federal limits for a gift exemption. The role of the grantor is pretty much completed after the assets are transferred and the paperwork is properly filed and settled.

The trustee is the party that takes over the management and oversight. The duties and responsibilities of the trustees are defined by the grantor during the construction. In some cases, grantors initially serve as trustees until they appoint someone else; some individual grantors set it up in a way that will appoint a trustee only when they become unable to assume management.

The beneficiaries are the parties who are named to eventually receive the benefits of the assets contingent on a trigger event – usually the death of the grantor(s). Beneficiaries also have duties and responsibilities: they may have to pay taxes based on the assets they receive as benefits, and they are also responsible for requesting an audit the work of the trustee to ensure that it’s being managed in accordance to the law and to the wishes of the grantor.

4 – How It Can Help a Family

With every created structure, there is an implied desire of keeping property and assets safe for the benefit of families. This implied desire is the historic factor that prompted the creation in the first place.

Structure your structure properly so conditions can be placed on distribution of assets when someone passes away

These things can be structured in ways that serve the interests of individuals who can be grantors, serve as trustees and also become beneficiaries; notwithstanding this asset protection strategy, creating an irrevocable trust (IT) is something that is more commonly associated with effective financial planning and protection for families.

With a properly structured entity, conditions can be placed on the distribution of assets when someone passes away. Gift and estate taxation can be reduced or eliminated, and family affairs can be kept away from public scrutiny by means of skipping probate court proceedings. Family fortunes can be protected from lawsuits and overzealous creditors, and trustees can be appointed with the understanding that they must adhere to the terms of the contract and help to make it grow.

5 – Do-It-Yourself (DIY) Platform

Asset protection and wealth preservation are part of an industry that generates billions of dollars in administration fees each year. Attorneys and CPA firms that offer services often charge hefty fees their planning expertise. As a result, many individuals and families shy away from setting up structures to protect wealth that they have worked hard to accumulate over several decades.

Although there is a certain amount of complexity involved, there are several DIY approaches that take each step into account making it easy that prospective grantors can take advantage of.

DIY structures are the result of advances in software and database technology and are so sophisticated and accurate today, that even most attorneys use them for their clients. Using an online platform that presents grantors with questionnaires about their finances, civil status and estate planning goals. The questions are related to the 15 key points discussed herein; once all the answers have been provided and the questionnaire is completed, two reviews take place. One review is automatically conducted by the software; the other review is conducted by seasoned professionals with years of experience. Once the correct documents are drafted, they are sent to the grantor for execution accompanied with instructions and guidance.

Once prospective grantors become familiar with the 15 key points presented in this article, going through the DIY process of creating an irrevocable version becomes a task that is not only easy to manage, but also beneficial in terms of avoiding considerable legal fees.

6 – Choosing the Trustee

Proper selection of a trustee is crucial. Some individuals who choose a living trust as an instrument primarily for asset protection and not so much for estate planning may be tempted to serve as grantors, trustees and beneficiaries, but there some caveats in this regard. A similar situation arises in family structures, whereby parents may want to automatically choose their oldest child to serve as trustee.

The choice of trustee should take into account a few factors: knowledge, experience, potential conflict of interest, access to the assets, management abilities, cost, and relationship. Grantors are likely to immediately think about appointing relatives as trustees because they feel that they have confidence in to manage their assets and handle their financial affairs, but this could be a problem insofar as creating a burden for a trustee who has his own family and work responsibilities.

Independent trustees should always be preferred because they fulfill the aforementioned factors and they create a fiduciary duty which is golden in the eyes of a court. Fiduciary duty is synonymous with a legal obligation to protect the assets. A CPA, for example, is a professional under the oversight of a state regulator. Appointing a CPA to handle trustee duties is the best course of action for grantors who believe that appointing multiple trustees is a wise choice. While there are no limits with regard to whom you choose or the number of trustees who may be appointed, the conflict of interest factor is amplified with the presence of more individuals acting in a fiduciary capacity.

If for some reason the grantor feels that he or she must appoint various trustees, a protector provision may be included to ensure that potential conflicts between trustees can be quickly resolved.

7 – Including a Protector

Grantors who choose to appoint an independent trustee such as a CPA, friend, in-law, or lawyer do not have to worry about completely and permanently ceding all control of the assets and property transferred to the entity. Within the agreement document, a protector provision can assign powers to an individual or an entity for the purpose of replacing the trustee as needed.

The protector strategy began being used by asset protection lawyers that operate in offshore financial havens such as the Cayman Islands, Cook Islands, and other jurisdictions and has since been implemented into the better domestic trusts.

Prospective grantors in the United States do not have to go offshore for the purpose of strong asset protection. States recognize that trustees and protectors can coexist within a fiduciary agreement. One such state is Delaware, where an individual or entity serving in this capacity is called an adviser under section 3313 of the Delaware Code.

The powers that can be assigned to a protector may include: the ability to replace trustees as needed, the right to control spending, the power to veto distributions, and the ability to step in whenever a conflict between trustees arises.

8 – Revocable vs. Irrevocable

Of all the legal strategies that can be applied when creating one, the most important to understand is the difference between revocable and irrevocable.

Watch the video on revocable vs irrevocable

RT’s are designed to give grantors an opportunity to easily undo the terms of the agreement so that they can retain control and ownership over their assets. RTs can also be modified at will by grantors.

Irrevocable versions are designed to give grantors maximum benefits in terms of asset protection, estate planning, tax advantages, Medicaid planning, and others. Unlike RTs, grantors do not retain ownership or control of assets held in irrevocable structure, and the terms cannot be modified as easily.

Generally speaking, irrevocable versions are the better choice for individuals and for families.

9 – Married Couples

Couples who are either legally married or who live together under the terms of a common law marriage or civil union can draft agreements that reflect their lifestyle and their financial goals. To this effect, a joint irrevocable structure can be created to meet the needs of most couples. In such case, one or both spouses act as the grantor, but each spouse can designate beneficiaries who can receive a share of property owned in common.

The terms that govern the property held in a joint structure can be dictated by both spouses. The estate planning benefit, when one spouse dies, the assets and property remain in the structure for the enjoyment of the benefits. A provision can be included for the purpose of a final distribution to take place once both spouses pass away.

You can preplan a marriage with a prenuptial agreement

Individual structures can also be created by married couples who wish to keep their property separate. Reasons for doing this include: second marriages and the desire to not cede control of assets and property to a spouse. Couples who are engaged and wish to keep their property separate throughout their union can also set up individual an irrevocable structure vs a Prenup which work 100% of the time in divorce situation whereas a prenup usually creates more problems than it solves; there is nothing more romantic than asking your wife to preplan a divorce with a prenup before you commit to spending the rest of your life together.

10 – Naming Beneficiaries and Distributing Benefits

This is something that is done for the benefit of others, who are usually spouses, children, and relatives; these are the beneficiaries. By creating a one, grantors have certain advantages and can even create incentives with regard to financial planning for children and minor beneficiaries.

One common concern among grantors as they grow older is whether their children and grandchildren could be negatively affected when they inherit a substantial amount of money. When it comes to beneficiaries who are minors, it allows grantors to specify those incentives and conditions that must be met before the trustee can make a distribution. Age is an example of a broad condition; in these cases, a minor must reach certain ages before distributions are made. An incentive would be a specific condition, which could be graduating from high school or from college to encourage that beneficiaries pursue education or careers.

Avoiding lump sum inheritances that may be squandered by potentially not-yet-mature beneficiaries is a popular and wise provision among grantors in the United States.

Guardians can also be nominated for minor beneficiaries when creating an irrevocable structure, and this is a designation that should also be made in a will.

11 – Exclusions

When learning how to create a trust, prospective grantors must think about every angle that could apply in terms of estate planning and distribution of wealth over the next 50 years. One particular angle that certainly merits careful thought is not so much who will be the beneficiaries; it is important to think about who must be specifically left out of distributions.

Similar to leaving people out of a will or disinheriting someone, it can be set up in a discretionary manner so as to designate who should really benefit from the estate and who shouldn’t. Exclusions can be specified in DIY versions, but they must not run afoul of provisions against disinheritance in certain states.

12 – Depositing Assets

Transferring assets into a structure is known as “funding the structure.” Just about any type of asset or property can be transferred, and this includes personal and business assets. Cash, life insurance policies, investment accounts, precious metals, and even companies can be transferred, but grantors should keep in mind that they are ceding ownership to the entity, which means that business and investment decisions will be made by the trustee after consulting with their financial advisor, you.

It can have a home even though a mortgage is charged against it

With regard to real estate, if the property is shared with a business partner in what is known as a tenancy-in-common agreement, your equity share can be added. Personal checking accounts, everyday vehicles that have no luxury or collectible value, 401(k) and retirement accounts, and assets that are not really valuable typically are left out.

If your home has a mortgage, it can still be added and, due to the St. Germain Act of 1982, the bank cannot call your loan due or accelerate your payment schedule with them. If you stop paying your mortgage, however, they can still foreclose on the home because they are still the first lien-holder. What they cannot do is go after other real estate or assets that are properly added.

13 – Jurisdiction and Venue

When choosing the state where the entity will be created, it is important to know about the applicable statutory provisions; this is known as the situs. The significance of choosing the situs cannot be ignored, and this was something that was partially discussed in the second point of this article with regard to the rule against perpetuities. Some states offer stronger asset protection than others; however, when real estate property will be transferred into the entity, the situs should be the same state where the real estate assets are located.

This means people with a summer home in Michigan or a winter home in Florida and Colorado, will likely need to set up more than one structure.

14 – Reasons for it

Protect your assets before entering into a nursing home with an irrevocable structure

Learning how to create an irrevocable structure is mostly a matter of function; understanding the reasons for creating an irrevocable structure and how financial goals will be achieved takes more thought and consideration. When the goals are clearly defined, drafting the agreement is easier.

The most common goals chosen by grantors include: passing wealth efficiently by avoiding the probate process, reducing estate taxation, preserving assets for charities, retaining control over wealth distribution, and protecting assets by keeping them within the family instead of a creditor or nursing home.

15 – Building a Legacy

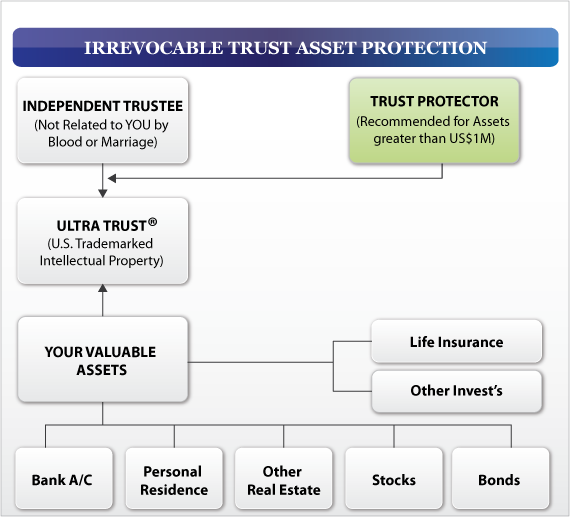

An irrevocable structure asset protection diagram of the different types of relationships involved. (Click the above diagram to enlarge)

At some point in life, prospective grantors shift their focus from wealth creation to wealth preservation. These structures are not merely for estate planning; they can be used in life to structure distributions to minors as they grow older and start building their lives, or they can also be used to alleviate tax burdens so that gifting to charities can be conducted for maximum benefit.

A properly managed entity can help to build a legacy by providing business continuity over a family fortune across generations. This is how a legacy can be built; financial success does not have to always live in the present, it can also be preserved and protected so that a family can always enjoy its benefits.

We look forward to our visit with you and your professional representatives to assist you with the advancement of your estate planning.

Cordially,

Rocco Beatrice, CPA (Certified Public Accountant), MST (Master of Science in Taxation), MBA (Master of Business Administration), CWPP (Certified Wealth Protection Planner), CAPP (Certified Asset Protection Planner), CMP (Certified Medicaid Planner), MMB (Master Mortgage Broker)

Managing Director, Estate Street Partners, LLC

Riverside Center Building II, Suite 400, Newton, MA 02466

tel: (508) 429.0011

“Helping our clients resolve their problems quickly, effectively, and decisively.”

The Ultra Trust® “Precise Wealth Repositioning System”

This statement is required by IRS regulations (31 CFR Part 10, 10.35): Circular 230 disclaimer: To ensure compliance with requirements imposed by the IRS, we inform you that any U.S. federal tax advice contained in this communication (including any attachments) is not intended or written to be used, and cannot be used, for the purpose of (i) avoiding penalties under the Internal Revenue Code or (ii) promoting, marketing or recommending to another party any transaction or matter addressed herein.