Asset Protection

This Asset Protection archive brings together articles that help readers understand the moving parts behind stronger planning, from core definitions to more advanced structural questions.If you…

Explore Trusts articles focused on practical questions, deeper explanations, and real-world planning issues that come up when families and owners are trying to make better trust and asset decisions.For a broader starting point, review Grantor vs Trustee vs Beneficiary and then compare it with Asset Protection Trust for a more focused next step.

This topic archive is one part of the larger blog. Use the sections below to move into related categories, compare ideas more easily, and keep your research focused on the question that matters most right now.

Some readers begin with broad asset protection questions, while others jump straight into trusts, tax issues, Medicaid, divorce, or lawsuit exposure.

Explore asset protectionEach topic hub pulls together related articles so you can compare ideas more easily instead of bouncing between unrelated posts.

See how the process worksWhen you are ready, use what you learned here to ask better questions, clarify priorities, and decide which planning direction deserves closer attention.

Contact UltraTrustChoose the category that fits your current question, then move into detailed articles, comparisons, and next-step guidance gathered under that topic.

This Asset Protection archive brings together articles that help readers understand the moving parts behind stronger planning, from core definitions to more advanced structural questions.If you…

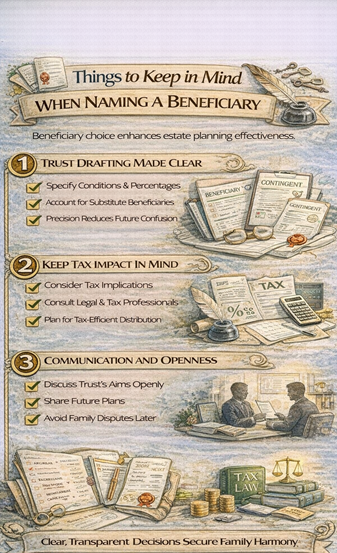

This Beneficiary of a Trust archive brings together articles that help readers understand the moving parts behind stronger planning, from core definitions to more advanced structural…

Browse Captive Insurance Structure articles focused on practical planning questions, comparisons, and next-step guidance.

Browse Derivative Financial Instrument Strategy commentary built to make complex planning topics easier to follow, especially when trust structure, ownership design, or family strategy needs a…

Explore Divorce articles focused on practical questions, deeper explanations, and real-world planning issues that come up when families and owners are trying to make better trust…

Read Estate Planning insights that connect technical trust ideas to real planning situations, with a practical focus on clarity, timing, and long-term decision-making.A useful way to…

Read Estate Planning and Trusts insights that connect technical trust ideas to real planning situations, with a practical focus on clarity, timing, and long-term decision-making.A useful…

This Financial Planning archive brings together articles that help readers understand the moving parts behind stronger planning, from core definitions to more advanced structural questions.If you…

Browse Grantor Trusts commentary built to make complex planning topics easier to follow, especially when trust structure, ownership design, or family strategy needs a closer look.Readers…

Explore Insurance articles focused on practical questions, deeper explanations, and real-world planning issues that come up when families and owners are trying to make better trust…

Explore Irrevocable Trust articles focused on practical questions, deeper explanations, and real-world planning issues that come up when families and owners are trying to make better…

Explore Irrevocable Trust Probate Protection articles focused on practical questions, deeper explanations, and real-world planning issues that come up when families and owners are trying to…

Browse Lawsuit commentary built to make complex planning topics easier to follow, especially when trust structure, ownership design, or family strategy needs a closer look.Readers who…

Browse LLC Advantages articles focused on practical planning questions, comparisons, and next-step guidance.

Browse Medicaid commentary built to make complex planning topics easier to follow, especially when trust structure, ownership design, or family strategy needs a closer look.Readers who…

This Nursing Home archive brings together articles that help readers understand the moving parts behind stronger planning, from core definitions to more advanced structural questions.If you…

Read Offshore insights that connect technical trust ideas to real planning situations, with a practical focus on clarity, timing, and long-term decision-making.A useful way to read…

This Prenuptial archive brings together articles that help readers understand the moving parts behind stronger planning, from core definitions to more advanced structural questions.If you want…

Browse Probate articles focused on practical planning questions, comparisons, and next-step guidance.

Browse Selecting a Trustee articles focused on practical planning questions, comparisons, and next-step guidance.

Explore Tax articles focused on practical questions, deeper explanations, and real-world planning issues that come up when families and owners are trying to make better trust…

Browse Trust and Asset Protection commentary built to make complex planning topics easier to follow, especially when trust structure, ownership design, or family strategy needs a…

This Trust Planning Professional Services archive brings together articles that help readers understand the moving parts behind stronger planning, from core definitions to more advanced structural…

Read Trust Protection insights that connect technical trust ideas to real planning situations, with a practical focus on clarity, timing, and long-term decision-making.A useful way to…

Explore Trusts articles focused on practical questions, deeper explanations, and real-world planning issues that come up when families and owners are trying to make better trust…

Read UltraTrust insights that connect technical trust ideas to real planning situations, with a practical focus on clarity, timing, and long-term decision-making.A useful way to read…

Browse Uncategorized commentary built to make complex planning topics easier to follow, especially when trust structure, ownership design, or family strategy needs a closer look.Readers who…

Read Wealth Management insights that connect technical trust ideas to real planning situations, with a practical focus on clarity, timing, and long-term decision-making.A useful way to…

These articles stay focused on this topic so you can compare ideas, definitions, and examples without leaving the same subject area.

Careful legal structuring is required for estate planning and asset protection. One strong option for people looking to separate ownership of the personal and…

In the realm of financial planning, creating a trust can be one of the most important steps in terms of achieving solid asset protection…

https://www.youtube.com/embed/LUAtg-hSlYQ?si=jUcDTGqmKabwjZgPWatch the video on Like this video? Subscribe to our channel.Here we examine the differences of revocable vs. irrevocable trust advantages. If you reposition (transfer)…

Watch the video on Can a Trust Be Sued - Land Trusts Myths for Asset Protection Like this video? Subscribe to…

Briefly describe what is a trust. Now I would like to talk to you about, what is a trust. A trust, no matter…

What do you mean, I Shouldn't be the Trustee of "my own" Irrevocable Trust? Have no discretion as the trustee with regard to trust…

First, a trust is a contract that names a trustee to manage any assets owned by the trust. A grantor (aka settlor) gives…

What is a Trust Protector and Do I Really Need One? Can it protect me and my money? How does a Trust Protector act…

What do you mean I won't be the Beneficiary of "my own" irrevocable trust? A self-settled trust is another name for being the beneficiary…

A testamentary trust is an extension of a will that allows someone to put assets into a trust after they pass away for…