“What is the origin of an Irrevocable Grantor Trust being used as a Family Trust, and how can it help me?”

We get many calls every week asking “what is a family trust, where did they originate, how could they help me?” There are many types of “family trusts.” Some are specifically for the purposes of holding real estate such as a real estate family trust, and some designed to hold only life insurance like an irrevocable life insurance trust (ILIT) and others are for more general purposes. In general, although the use of a family trust dates back a few centuries, lawyers and estate planning firms have mostly overlooked the irrevocable grantor trust as a preferred instrument for this purpose. While most ill-advised attorneys tend to promote the revocable living trust, we, along with most asset protection attorneys are of the opinion that an irrevocable grantor trust makes the best family trust in most circumstances, and the following eight reasons explain why.

Benefits of a Family Trust #1 – An Irrevocable Grantor Trust Protects Assets

King of British Empire creates feudal taxes in the likeness of estate taxes.

Creating a postmortem real estate family trust was one of the earliest purposes of trusts upon their establishment in the 15th century. The historically controversial King Henry VIII of England did not like the use of trusts too much; in those days, feudal taxation was excessive to the point that the Crown supported the appropriation of property as soon as knights passed away. In this case, early real estate family trusts were created upon the execution of wills, which meant that relatives could benefit from land that could not pass to the Crown. King Henry VIII was not in agreement with this practice and thus prohibited these real estate family trusts by royal decree; upon his passing due to health issues related to obesity, the English Court of Chancery reauthorized the use of trusts.

![]() Learn the 3 key to uncompromising asset protection by clicking here

Learn the 3 key to uncompromising asset protection by clicking here

Although feudal taxation would be gone long before the fall of the British Empire, it survives in spirit in the form of estate taxes. This taxation standard is the basis of the idiom about there being nothing certain but death and taxes, for it is true that even the dead are required to pay tax in the absence of legal instruments such as an irrevocable grantor trust in today’s world.

Estate taxes are present at both the federal and in many states at the state level. Essentially, these are death taxes, a vestige of the Henry VIII days that seeks to collect revenue even after the taxpayer shuffles off this mortal coil. Modern statutes are not draconian in this regard; some exemptions and the use of an irrevocable grantor trust are allowed.

In situations like these irrevocable trust advantages are outstanding. An irrevocable grantor trust basically serves the same purpose as they did when real estate family trusts were created in the midst of the Renaissance period: to protect property and assets from the claims of third parties, including the tax authority. In the past, these third parties were the Crown, the feudal lords, the lenders, and potential usufructuary actors who would jump at the chance of claiming a piece of a knight’s property once he passed away. The modern versions of these third parties in the United States would be the Internal Revenue Service (IRS), the state revenue collection agencies, creditors, opportunistic or frivolous plaintiffs, and even gold diggers.

Irrevocable trust advantages go beyond the estate tax. A modern irrevocable grantor trust can do more than simply avoiding the payment of death taxes; they can provide individuals and their loved ones with guaranteed income while effectively transferring property and assets to heirs in a manner that is more efficient than traditional wills. Asset protection attorneys dedicated to estate planning and wealth management have been known to recommend about a dozen trust structures to families; however, only a properly written, executed, and funded irrevocable grantor trust is known to provide “bulletproof” protection if they are properly structured and managed. Any irrevocable grantor trust broken in the last 150 years of litigation, the only ones broken were ones that had issues with how they were written, executed, or funded.

Benefits of a Family Trust #2 – Irrevocable Trust Advantages Include Providing Ideal Ownership Situations

What are other examples of irrevocable trust advantages? It all boils downs to a legal theory known as the “burden of ownership.”

There is no question that we live in highly litigious times. Frivolous lawsuits that seek to establish a claim over property or assets are filed every day, and this is a situation that is often magnified after death. A good example in this regard would be legendary musician Prince, whose unfortunate death was followed by numerous siblings and half siblings coming forward to meet under contentious circumstances as they suspected that the late Minneapolis star did not leave do any estate planning what-so-ever, not even a will.

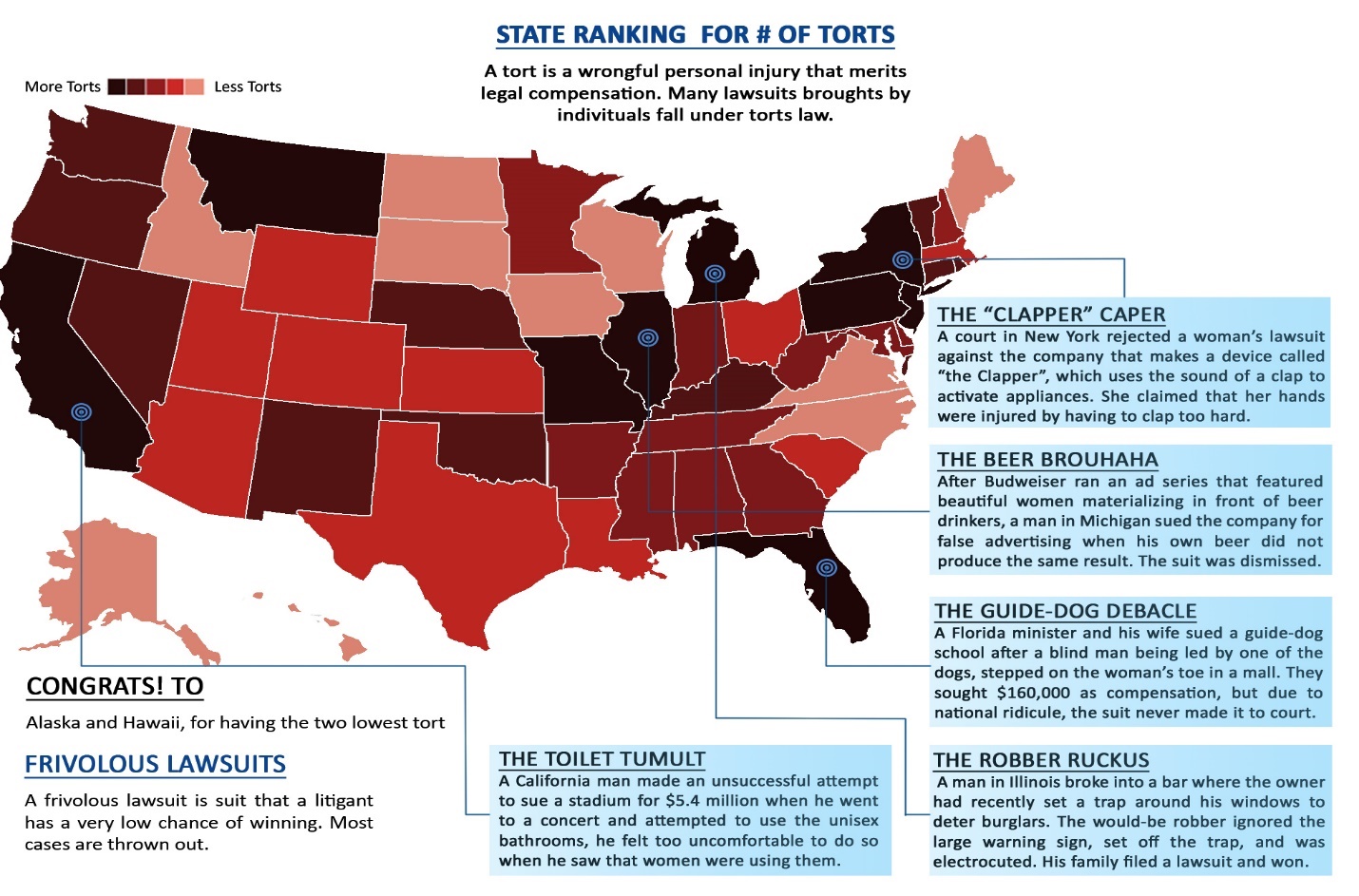

A graphic map of the number of torts per state. (click on image to see larger detail. 383KB)

Legal analysts and asset protection attorneys following the Prince case have commented that the burden of ownership is something that will haunt his estate for years to come as his survivors continue to fight in court. In the absence of an irrevocable grantor trust, Prince Roger Nelson’s estate will pay a huge estate tax with relatives ready to file claims for the remainder that establish his ownership of assets and their rights as heirs apparent.

The burden of ownership is what makes frivolous lawsuits happen in the first place. The first legal hurdle that a plaintiff must clear is that of establishing that the respondent actually owns the assets or property being claimed. The case cannot move forward and should be dismissed when the court finds that the lacks this basis; in other words, claims can only be made against property that is legally owned by the respondent.

When an irrevocable grantor trust, the burden of ownership is effectively removed. Assets placed within a properly written, executed, and funded irrevocable trust are not owned by individuals; instead, they are owned by the legal entity established by the terms of the trust, but unlike a corporate structure, the trust has no shareholders, just beneficiaries. This does not mean that families cannot enjoy automobiles, homes, art, liquid funds, investments, etc; all these assets are still available for the use of beneficiaries, and they can even be sold and transferred by the trustee as instructed by the trust.

Prince could have set up an irrevocable trust

In the case of the late Prince, for example, an irrevocable trust could have been set up so that the income from the rights and royalties to the music he created could be paid to his family in perpetuity. Prince could have effectively separated himself from his music, but only in the ownership sense, and he could have pulled this off in a very private way so that no one except for select confidants would have known about the true ownership.

Doing away with the burden of ownership is something that can certainly be considered one of the irrevocable trust advantages. Once again, the notoriously litigious society that we live in makes this a necessity for many families.

Benefits of a Family Trust #3 – Income Tax Returns

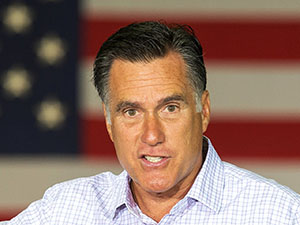

One of the most famous examples of an effective irrevocable trust structure being used was made known to the public during the 2012 electoral campaign of former Massachusetts Governor Mitt Romney.

As a candidate to the Presidency of the United States, Romney was required to provide a series of financial disclosures that revealed his use of a series of irrevocable trusts that effectively will allow his family to avoid a 35 percent tax rate on assets valued at more than $5M at the time of the trigger, his death.

What the public learned about Mitt Romney’s irrevocable trusts and how they protected assets

What the public learned during Romney’s campaign about irrevocable trusts and how they shield assets from taxation was unprecedented. His family’s estimated net worth inside the trusts back then was $250 million, but this mostly came from financial disclosures of his investment banking firm Bain Capital. Due to the privacy features of irrevocable trusts, it is very possible that the American public will never know the exact net worth of Romney and his family.

Despite his use of irrevocable trusts, Romney was still able to produce the requisite income tax returns that candidates are expected to show to the public. This tradition of American politics did not help Romney’s campaign much because it proved that he took advantage of certain credits and exemptions that reduced his personal income tax burden. What the public never got to see, however, was any tax return from the irrevocable trusts that the Romney family members reportedly benefit from.

The American public will probably never get to see the tax returns produced by the Romney family trusts, and this is due to the bold privacy protections of irrevocable trusts. This does not mean, however, that the trust itself is invisible to the IRS; it has its very own tax identification number and files its own tax return, but it is understood that the beneficiaries are not the legal owners of the assets held therein.

Irrevocable grantor trusts used for the purpose of family wealth preservation and management are not illegal instruments of tax avoidance, either the trust or the individual will pay taxes due on income, it is typically just a different process. Form 1041, U.S. Income Tax Return for Estates and Trusts are filed each year by thousands of trustees and CPAs across the country. Tax advantages and reduced liability shall not be confused with tax avoidance.

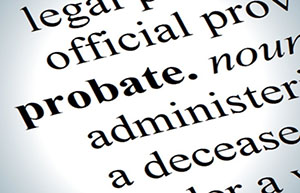

Benefits of a Family Trust #4 – The Probate Process

The statutes of all 50 states of the Union have at least two elements in common: a criminal code and a probate code. In the United States and across the world, the intent of the probate process is to establish the legal validity of wills and other instruments that individuals executed before they passed away. In other words, the probate process ostensibly puts the courts in a position of representing the legal interests of the departed.

Probate process in America is a legal avenue for wealth redistribution

In reality, the judicial probate process in all 50 states serves as a legal platform of wealth redistribution, whereby debts and taxes are paid before the heirs can establish a claim to what is left of the estate.

Probate proceedings happen to be matters of public record; this is particularly useful in cases of intestacy, which is when individuals pass away without leaving a trust or even a will. As mentioned above, this may seem to be the case with the Prince estate, and it is bound to get more convoluted as time passes and more dirty laundry is hung out to dry on news headlines.

No family wants to go through the probate process because of the cost (5-10% of assets), public scrutiny, delay in distribution of assets, and opportunity for outsiders claims and as any asset protection attorney will tell you, it can be completely avoided. Trusts can certainly prevent the ugliness of public probate proceedings. In terms of avoiding probate and keeping family life out of the public view, nothing is more efficient than a trust, and this is something that cannot be stressed enough: any trust can keep family affairs in the family when the time comes to settle an estate. Moreover, a trust should also be structured in a certain way for this privacy and anti-probate features to be effective.

Benefits of a Family Trust #5 – Setting Up an Irrevocable Grantor Trust for Generations

Families who wish to protect their assets so that they can pass from one generation to another should choose their instrument carefully. Two important benefits of a family trust should always be longevity and equity in terms of asset control.

A revocable living trust cannot guarantee longevity, nor can they ensure families that one of their members could suddenly exert total control over property and assets. Most grantor trusts are of the revocable living trust type, which means that the Grantor, as owner of the assets that will be deposited in trust, will retain too much control. One notorious example in this regard is the family trust created by media mogul Sumner Redstone, majority shareholder of Viacom/CBS.

Sumner Redstone, owner and CEO of Viacom Inc.

Sumner Redstone, owner and CEO of Viacom Inc., convinced members of family trust to allow him to retain control

The Viacom/CBS media empire found itself at odds when the National Amusements trust, which has 80 percent voting power in the Viacom/CBS affairs, moved to oust two top executives. According to probate filings, Redstone convinced the members of the family trust to approve keeping him in control despite his advanced age and questionable competence to handle financial affairs.

As the Viacom/CBS case progressed in court, legal analysts argued whether giving Redstone so much control over the trust was a wise business decision for Viacom/CBS. To be clear, the National Amusements trust is irrevocable, but it is structured in a way that makes Redstone the only beneficiary as long as he is alive, which means that he can appoint or dismiss trustees as he pleases.

There are better ways to establish irrevocable trusts that would not run into the issues seen by the Viacom/CBS sordid state of affairs. The first step is to ensure that the trust is not a revocable living trust, which gives the Grantor too much control over decisions on how to manage the family fortune. The idea is to establish solid permanence for the family by stripping ownership from the Grantor and appointing an independent Trustee. The trust must be structured in a way that can benefit the family from one generation to the next, and this requires a structure that does not allow arbitrary the removal of assets or beneficiaries. In some cases, a Trust Protector may also be appointed for the purpose of hiring and dismissing trustees.

Benefits of a Family Trust #6 – Keeping Family Fortunes From Being Lost Abroad

In the later decades of the 20th century, major changes in the laws and regulations of the United States prompted some families to consider going offshore for the purpose of protecting their assets.

The offshore asset protection industry came of age during the Reagan years and grew exponentially as the World Wide Web developed. As a result, more American families became convinced by their asset protection attorney that the best asset protection strategy available to them could be found in offshore financial havens such as the Cayman Islands, the Bahamas, Switzerland, Panama, and other nations where fiduciary laws and regulations favored privacy and the protection of wealth.

Offshore financial havens take advantage of their regulatory climate to safeguard assets and keep them away from aggressive creditors, frivolous plaintiffs, freeloaders, gold diggers, and other unpleasant characters whose purpose in life is to claw away at family fortunes.

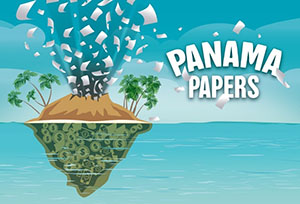

Although the offshore asset protection strategy is often considered to be pretty bold and effective, it has unfortunately attracted lots of attention in the 21st century. The so-called “Snowden Effect” of activism and Wikileaks-style whistleblowing resulted in the Panama Papers scandal of 2016.

Panama Paperss give the estate planning and wealth management’s world industry a lesson

The estate planning and wealth management industry has learned some hard lessons in the wake of the Panama Papers, particularly about the zeal that drives activists and journalists to investigate and expose what they consider to be scandalous. It has already been established that the bulk of the Panama Papers revelation consists of individuals, families and business entities that simply wished to legally take advantage of offshore jurisdictions to protect their assets. Unfortunately, the names of American families have been run through the mud along with the names of unsavory characters who also used offshore financial havens for nefarious purposes.

Any expert asset protection attorney will tell you, there are two clear realities about offshore family trusts: they are effective tools for asset protection, but they are also overkill for most American families as the cost to maintain one ranges from $5-10,000 annually. The fact that they are also being targeted by surreptitious activists and data journalists who claim to operate in the name of transparency is alarming.

What any expert asset protection attorney will agree with, is that many American families do not realize is that bold asset protection and wealth preservation can be achieved domestically with a properly written, executed, and funded irrevocable trust, which can also be combined with a limited liability company (LLC) for even bolder protection. There is no need to get tangled up in high maintenance costs or a cloak-and-dagger affair such as the Panama Papers.

Benefits of a Family Trust #7 – Gifting Versus Irrevocable Grantor Trusts

Many an asset protection attorney suggests gifting as a strategy for individuals who wish to transfer a lump sum to their survivors. They may even recommend transferring funds into an irrevocable trust as a gift. This is a severely flawed strategy that must be avoided at all costs.

Irrevocable trusts are superior to plain gifts in the sense that the Grantor will relinquish all control. First of all, lump sum gifts tend to be used irresponsibly, which happens to be against the precepts of estate planning. Second, a gift made to an irrevocable trust may expose those assets in a potential court case.

Plaintiffs represented by seasoned asset protection attorney who are skilled in the ways of asset protection can easily uncover gifts made into irrevocable trusts. If a family wishes to place assets in trust for the benefit of their heirs, then the Grantors must be properly advised on how the transfer must be executed. Gifts into trusts may appear to be questionable to a judge, who could in turn issue an order to reverse the asset transfer.

Any asset protection attorney will tell you that irrevocable trusts are better options than outright gifts, but they must be structured in a certain way that protects the interests of the family. Reduction of capital gains taxes is just one aspect of this strategy, which may also call for Independent Trustees and a Trust Protector.

Benefits of a Family Trust #8 – A True Legacy and Peace of Mind Can Be Attained With an Irrevocable Grantor Trust

Primary benefits of a family trust are to keep assets within the family, and no other legal instrument can achieve this as efficiently as an irrevocable grantor trust.

For married couples who are planning on having children, there may always be a concern about what could happen to their fortune should one spouse pass away. If the surviving spouse gets married again, there is always a chance that the estate of the departed husband or wife could be enjoyed by the members of the new family instead of what the couple had originally planned.

With a properly constructed irrevocable trust, a provision can be stipulated for the benefit of true beneficiaries, who can be the children of the couple who agrees to form the trust in the first place.

When setting up an irrevocable trust to protect family assets, the ultimate goal is to establish a legacy. A frank discussion with estate planners should provide the guidance for the objective of the irrevocable trust. From drafting to funding and from execution to management, an irrevocable trust can truly help families build their legacies in perpetuity.

We look forward to our visit with you and your professional representatives to assist you with the advancement of your estate planning.

Cordially,

Rocco Beatrice, CPA (Certified Public Accountant), MST (Master of Science in Taxation), MBA (Master of Business Administration), CWPP (Certified Wealth Protection Planner), CAPP (Certified Asset Protection Planner), CMP (Certified Medicaid Planner), MMB (Master Mortgage Broker)

Managing Director, Estate Street Partners, LLC

Riverside Center Building II, Suite 400, Newton, MA 02466

tel: 1+888-938-5872 +1.508.429.0011 fax: +1.508.429.3034

email: [email-obfuscate email=”” link_title=”Email Rocco Beatrice” class=”email_obfuscate_class” tag_title=”Question from UltraTrust.com”]

NEW Site: UltraTrust.com

“AA” Rated Advisor: //www.assetprotectionsociety.org:80/advisors/?a=PG:2411

Massachusetts, Rhode Island, and New Hampshire State Representative for: www.AssetProtectionSociety.org

“Helping our clients resolve their problems quickly, effectively, and decisively.”

The Ultra Trust® “Precise Wealth Repositioning System”

This statement is required by IRS regulations (31 CFR Part 10, 10.35): Circular 230 disclaimer: To ensure compliance with requirements imposed by the IRS, we inform you that any U.S. federal tax advice contained in this communication (including any attachments) is not intended or written to be used, and cannot be used, for the purpose of (i) avoiding penalties under the Internal Revenue Code or (ii) promoting, marketing or recommending to another party any transaction or matter addressed herein.