With the Favorable IRS Determination Letter to Prove it

For those that have ever thought that they pay too much income taxes, this might be the most important post they ever read.

Mike was a doctor in Texas. He made a lot of money, but he worked his butt off to earn it; with 20 years of schooling, 3 years in residency, and sometimes working 90-100 hours a week, giving up half to a government that was going to waste it on a bridge to nowhere really irritated him. About 48% of the $1.1-1.4M 1099 income he made went to pay taxes and because of it, he practically had an anxiety attack when he had to write those $100,000+ checks to the IRS every quarter.

He lived in a gorgeous 7,000 square foot house, both him and his wife drove luxury cars on top of his Ferrari, Maserati, and Range Rover fun cars and his kids went to private schools, but he only spent about 150,000-175,000 per year on their lifestyle. That meant that he was paying taxes on about $1-1.2M of income that he didn’t really need.

His colleague, Chris, told Mike about us after helping him with a similar circumstance. After a 30-minute conversation to understand his situation, we presented Mike with a few income tax-saving options such as oil and gas exploration, the creation of a non-profit foundation, the charitable remainder trust, and a customized retirement planning cash balance strategy. He decided that the retirement planning cash balance option made the most sense for him and his family.

Our actuary put together a plan based on his goals. He contributed an average of about $1M to a Super 401k, Pension Cash account, 401h, and COLA retirement accounts. In about 3 years he had accumulated a bit more than $3.2M and saved $1.5M in taxes.

He told me “Rocco, I was either going to give the $500K to the IRS or I was going to give it to my myself into my retirement account – it was a bit of a no brainer.”

“I was practically getting a 100% return on my money immediately because I’m putting about double into my retirement account then I would have been able to. So now, I am not making 4-8% per year on the $500K retirement account that I would have had before, but now I am making 4-8% a year on the entire $1M. It means that the retirement account grows exponentially faster. It would have taken me 5-6 years to accumulate a retirement account of more than $3M before.”

To say that he appreciated our suggestions, was a bit of an understatement. But he was not alone:

Joe in New Jersey who ran a carpet installation business averaged net income of about $500-700K per year. We approached his situation in a similar fashion as Mike and he saved about $250K per year from his tax bill while amassing a $3.5M retirement fund in 5 years.

John on Long Island who had a real estate business netted about $500-600K a year. We were able to save him about $200K a year in taxes.

Ross lived in between New York City and Miami running a Herbalife distributorship and he averaged between 900K-1.1M net income and we used the same strategies to defer him and his wife about $350K in taxes as well.

Finally, Ron in Boston was a dentist as he was able to knock off $100K from the check that he wrote Uncle Sam as well.

Problems and Misconceptions

The problem is that when most people think about retirement planning, they are thinking about SEP account, Standard 401k, Standard IRA, or a Roth IRA.

For those making more than $250K a year, the maximum amount they can contribute with these plans is so tiny (typically a $18-59K contribution only results in tax savings if $9-25K) that it hardly helps them make a dent at all if their tax bill gets into the $200-400K range, so many don’t even bother.

The most frequent response I get when I talk to high earners about making small changes to their planning that save them up to $500,000 a year …is “….Is that legal? I have a CPA and he takes all the deductions possible. How come he hasn’t showed me something like this before?”

And one would think that your CPA would offer the best tax advice to save on taxes, right?

Yes, a CPA may know about the accelerated depreciation benefits of Section 179 or the intricate details of how to expense mileage on your car travel, but most CPA’s don’t know anything about many of these loopholes available to their business and 1099 clients, nor are they incentivized by the $5-10K they’re paid every year to find those special loopholes.

Are they really going to take a risk in making a mistake or the time to learn something new in the middle of tax season on something they are not experts in, in order to save you a few extra dollars. Not likely.

My name is Rocco Beatrice and I hold a CPA, MBA, MST (Master’s Degree in Taxes). I am the Managing Director at Estate Street Partners. In business for more than 30 years, we have an A+ with the BBB, are a member of the National Ethics Association, and have helped more than 4,100 families protect and save more than $4.3 Billion.

While I’ve been quoted on ABC, Fox, or CBS about how business owners and 1099 employees just don’t take advantage of their biggest tax loopholes, I don’t tell you that to impress you. I tell you that because I want you to know that these are not necessarily new ideas, but they work 100% of the time and are part of the IRS tax code… and I have several Favorable Determination Letter’s from the IRS to prove it!

A few years back congress passed the Pension Protection Act and your accountant may not be aware of how these changes can dramatically change your tax bill – most accountants are not.

The Secret

So what is the secret to increasing limits on cash balance retirement plans like this? The secret is that when you get a pension actuary to approve a customized plan, the limits can be as much as 20 times higher than the standard off-the-shelf plans. The IRS relies on the actuary’s number and if they bless the plan, you are golden. Our actuary has created more than 5,000 plans like these over his 46 year career so you can trust you’re getting the best experience in the business.

The Cherry On Top

And the cherry on top is that up to 33% of your contributions to a cash balance plan can be put into the ultimate in retirement accounts very few have even heard of…the 401h.

The 401h is better than the 401k, IRA, Roth IRA – really anything out there. Why? Because they offer a 100% tax-deduction on contributions, it grows capital gains free, and there is no tax on the money when it’s taken out … if used for medical “related” expenses.

And with couples over 55 expected to spend more than $460K on medical related expenses during the remainder of their life span according to AARP, not even including nursing home costs, tax-free “medical expenses” is a huge benefit. The 401h covers a huge variety of items including medical insurance, insurance deductibles, Lasik Eye Surgery, Personal Trainers, Spa Facilities, Usage Fees for Facilities, dentures, dental fees, nursing home care, and on and on and on…there is a list of literally hundreds of things it can be used for.

Believe it or not, the tax year is only weeks away from ending. If these strategies seem intriguing, then there’s not much time left because once the clock turns midnight on December 31, the carriage turns into a pumpkin and we will be forced to start planning for 2017. Since everyone procrastinates, imagine how impossible will be to get anything accomplished in December.

Getthing This Done

So how does one get this done? Just tell your CPA that you are interested these tax strategies. If they aren’t familiar, then we can help them get up to speed quickly. Yes, we’ll work with your CPA. Typically, we can review your situation in a 15-30 minute consultation. We then have our actuaries present a proposal. If it makes sense to you, your accountant with our guidance can help you execute the plan.

The Catch

So what’s the catch? The catch is that while one never pay taxes on the 401h money when used for medical expenses, with the Cash Balance plan or Super 401k accounts one will need to eventually pay taxes when they take the money out. But wait a second. Right now, we are paying 40-60% in taxes on money that we don’t immediately need. We are living on $100-200K per year.

By the time retirement comes around, there is likely going be a much lower tax bracket because you’re only going to take out what is needed to spend and we could avoid the FICA, state tax and Obama tax altogether. You might even live in a lower tax state like Florida or Texas with zero income tax.

Interested in these strategies? First ask your CPA about them. If he is not familiar, or does not want to go it alone, we can help. Contact Rocco Beatrice at or (888) 938-5872.

Top Growth Stock Mutual Funds to Invest in Over a 10 Year Horizon

If you are like most of us, you want to invest over the long haul, buying the best mutual funds to invest in and not have to worry about it. Most people automatically make an assumption that growth stock mutual funds will provide the best returns over the long run. Often times this is a poor assumption, but in our research we found the best mutual funds to invest in were, in fact, growth stock mutual funds, but let us not forget, retirement investing is for your long term retirement goals, so you want to make the most of every dollar you put in there, so you can have enough money to retire… maybe even retire early.

Kiplinger puts out a great list of best performing mutual funds to invest in (10 years). They actually look at the best mutual funds to invest in during the last year, the last 5 years, 10 years and 20 years, but let us not digress. Their analysis is purely from a statistical perspective; e.g. which funds averaged the best returns. No doubt that it might be fun to take a look at the best mutual funds to invest in for the last year. Here one will often find growth stock mutual funds that had large investments in some of the highest-appreciating stocks and “got lucky.” The true testament comes for the funds that can endure and consistently outperform year in and year out through full business cycles. A full business cycle being about 5-7 years on average. (we will later explain how we define a full business cycle)

Best Growth Stock Mutual Funds to Invest In

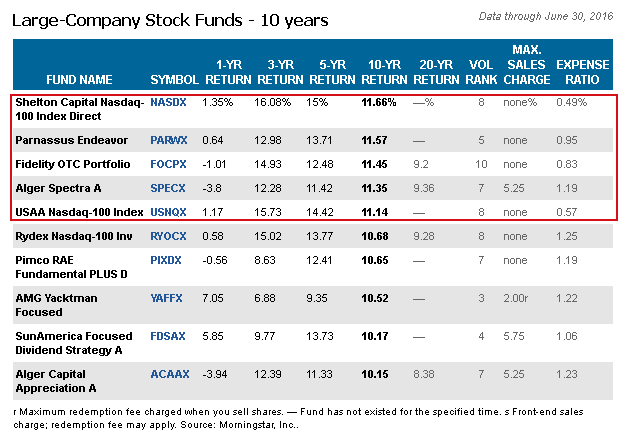

Large company stock funds over last 10 years. Data through June 30, 2016. Source: Morningstar, Inc.

Therefore, since our time horizon for this analysis is 10-15 years, we are most interested in the best performing mutual funds (10 years) over the long run. Those mutual funds to invest in which, don’t just get lucky one year, but have the skills to “get lucky” year in and year out selecting their stocks and getting out at the right time as well. Most growth funds often have a year of outperformance and maybe even 2 or 3 years. One would suggest that their outperformance really goes from “getting lucky” to actually having real talent with stock picking. However, the most skilled managers of growth stock mutual funds do it year in and year out in up markets and down markets.

By selecting the 10-year timeframe to focus our attention on, we’re looking for those best performing mutual funds to invest in that actually have gone through a major market down-turn like the one that occurred in 2008 when the S&P500 was down 37%. 2008 was one of the most painful periods for most people in their 401K. How did these funds perform during the most painful period in recent history? Did those growth stock mutual funds outperform the S&P500 during the tough years as well? Or were they susceptible to the same dips that the stock market tends to have at least once every business cycle?

Critical Big Picture Fact:

Since the year 1900 there have been 19 recessionary periods. That is one recessionary period every 6.1 years on average. The last one occurred in 2008/9.

Each one of these recessionary periods resulted in a 20%-80% loss in the S&P 500. Currently, we are 8 years from our last recessionary period.

The top 5 best performing mutual funds (10 years) illustrated have all had returns that have averaged over 11%. We can tell you this is great, but not as great as some tactical private wealth management funds that we have learned about.

What is the difference between a tactical private wealth management fund and a mutual fund?

A tactical private wealth management fund and a mutual fund both invest in underlying securities such as stocks, bonds, mutual funds, and ETFs and they both offer sector-type fund options (dividends, real estate, municipal bonds, etc.). The biggest difference is that most mutual funds, as detailed in their prospectus by law, typically have to be fully invested regardless of how poorly the market is doing. Every mutual fund defines this slightly differently, but it tends to mean they are required to have be invested by a minimum of 80% of the assets in the underlying stocks/bonds they are investing in. That means that when the market is going down, the mutual fund must keep 80% of all of their assets invested in the market regardless, as stated by rule 35D-1 under the investment Company Act of 1940. Rule 35d-1 restricts a mutual fund manager from liquidating and protecting your money during downturns in the market because they must stay 80% fully invested. This does not necessarily mean the mutual fund manager is a poor stock/bond picker, but rule 35D-1 simply prohibits them from selling securities in a down market to protect your money. This is one of the dirty little secrets of the industry.

Through our research, we found that tactical private wealth management funds do not operate within the same guidelines and restrictions of rule 35D-1. Tactical private wealth management funds offer investors more flexibility to sell the market.

The Best Growth Stock Mutual Funds to Invest In: Is There Something Even Better?

The key point here is that there is no trigger for the mutual fund manager to get out. They are relying on you to sell the mutual fund or your broker to sell for you. The only problem is that your broker gets paid only when you are fully invested in the mutual funds. If s/he takes your portfolio to cash, s/he just cut their own salary. I don’t know too many people that would proactively decide to cut their own income. Therefore, a broker telling you “sell everything” to protect you from losses in the market rarely occurs.

When there is a big loss in your portfolio, your broker will typically tell you that you need to ride the ups and downs of the market because over the long run, stocks offer larger returns than most other asset classes. And your broker would be right over a 50-100-year period, but if you’re nearing retirement (5-10 years) or are already in retirement, you may not have the luxury of taking significant losses in your retirement account during these times. If you were planning on retiring in 5-10 years and you lost 40% of your retirement, you may be changing your plans to retire in 15-20 years. If you don’t love your job, then that could be a real slap in the face.

Our research indicates that tactical private wealth management funds are different.

Tactical private wealth management funds have the ability to get out of stocks/bonds in the blink of an eye. They typically use models that warn them when the markets are looking unstable or shaky in an attempt follow market trends. In uncertain times, they have the ability to get out of stocks and go to cash until their models tell them that all is clear and they are safe to invest again. Many of them have a great track record of avoiding major market disasters and because of it, their overall returns typically outperform Kiplinger’s best performing mutual funds (10 years) through a full market cycle.

Never Forget Warren Buffet’s Rules of Investing

If you recall the famous quote by Warren Buffet. There are 2 rules to investing money. Rule #1: Never lose money. Rule #2: Never forget rule #1.

The quote is obviously cute and silly on the surface, but it has a much deeper meaning.

The reason is math.

When you lose principle in any investment, you need to make more than what was lost just to get to break even. If you lose 40% in year 1, then make 40% the following year, you don’t get back to even – do the math.

For example, if Joe had $500,000 invested in the stock market and he loses 40%, he is left with $300,000. If he made back 40% in year 2, his nest egg would only increase to $420,000. In order to get back to $500,000, he would need to earn a return of 67% just to get back to breakeven. **These calculations are not including inflation or distributions you are taking to support your retirement needs.**

When you avoid big losses, the returns take care of themselves. That is why tactical private wealth management funds are typically so much better than even the best growth stock mutual funds.

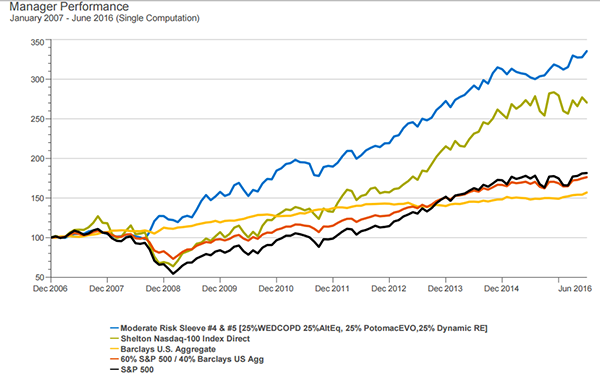

Let us compare some tactical private wealth management funds that we have found through our research with the #1 mutual fund in Kiplinger’s Best Performing Mutual Funds to Invest in (10-year period). These returns are all net of fees and expenses so we are comparing apples to apples. As you can see from the cumulative returns chart below. The private wealth management funds are the blue line, Kiplinger’s #1 on their list of best performing mutual funds to invest in (10 years) is olive, and the other lines are benchmarks such as the Barclays U.S. Aggregate bond fund in yellow, 60%/40% (S&P500/Barclays U.S. Aggregate) stock/bond mix in orange, and the S&P 500 in black. The average return for the tactical private wealth management funds through a full market cycle (analysis period) are higher by around 2.5% (13.59% vs 11.09%) over this 10-year period.

Kiplinger’s best performing mutual funds to invest in 10 year period. Source: Informa Business Intelligence Zephyr OnDEMAND

Manager vs Benchmark Return Jan 2007 to June 2016. Source: Informa Business Intelligence Zephyr OnDEMAND

Over 10 years the difference can be staggering. For example, if we start with $500,000 in Kiplinger’s top fund, and extrapolate 10 years with an average return of 11.09% your Kiplinger’s top fund investment will be worth $1,420,862. While the same extrapolation over 10 years with an investment in a tactical private wealth management fund we achieve a 13.59% average return and end up with $1,788,014. That is $367,000 more for the tactical private wealth management fund.

In reality, most retirees and pre-retirees are going to live through multiple business cycles. What does an extra 2.5% do for you over 20 years? Well for example, if we start with $500,000 and extrapolate 20 years with an average return of 11.09% we get $4,060,309 for Kiplinger’s top fund, not bad. While the same extrapolation over 20 years for the tactical private wealth management fund with 13.59% average return is $6,393,991. The tactical private wealth management fund returns $2.3M more. What could you do with an extra $2.3M? Perhaps you could retire a year or 2 earlier than you had planned, but, of course, we have to remember that past performance is never an indication of future results.

But as we said earlier, these comparisons really are not fair, because the tactical private wealth management funds do not have the same level of drawdowns as most mutual funds, especially the growth stock mutual funds, due to the fact that mutual fund prospectus restrictions don’t allow them to avoid big market losses, while tactical private wealth management funds can go to cash and avoid the big losses, while at the same time being able to take advantage of the market decline by putting their cash back to work in the market in near the lows. See the drawdowns over the last 10 years of the funds from below. During the depths of the 2008 crash the tactical private wealth management funds were down about 11% while the Kiplinger’s Top Fund (NASDX) at its lows was down a full 50% during the same period. Do you remember how losing 50% felt?

The drawdown report below shows how much each investment was down a during any given point in time within the market cycle. All of the funds we are analyzing are shown below.

Drawdown investment report displaying when markets were down at any given time. Source: Informa Business Intelligence Zephyr OnDEMAND

There is another great caveat here: the best performing mutual funds to invest in as reported by Kiplinger, are high risk / high return growth stock mutual funds. The tactical private wealth management funds described herein are only moderate risk funds that typically trade with 50% less risk than the market (S&P 500). This is reflected in the drawdown report above, but one must seriously consider the amount of risk they are taking in order to achieve the returns they are getting. In the world of low interest rates and the everlasting reach for yield, one must consider the quote by the founder of PIMCO and current Janus Fund Manager, Bill Gross:

“At some point you should not worry about the return on your money, but rather the return of your money.”

Being 8 years into a business cycle does not leave much time for one to consider their options in the authors opinion. Estate Street Partners is not an investment advisory firm, but if you would like to learn more about tactical private wealth management funds, we can refer you to an appropriate advisor. Call us today for more information at (888) 938-5872.

We look forward to our visit with you and your professional representatives to assist you with the advancement of your estate planning.

Cordially,

Rocco Beatrice, CPA (Certified Public Accountant), MST (Master of Science in Taxation), MBA (Master of Business Administration), CWPP (Certified Wealth Protection Planner), CAPP (Certified Asset Protection Planner), CMP (Certified Medicaid Planner), MMB (Master Mortgage Broker)

Managing Director, Estate Street Partners, LLC

Riverside Center Building II, Suite 400, Newton, MA 02466

The Ultra Trust® irrevocable trust asset protection plan is the best way to protect your assets without going offshore and without risking trouble with the IRS and government.

Over the last decade, asset protection has become a topic of interest among many individuals and families across the United States. Asset protection strategies have been around for centuries, and one of the most commonly discussed today, since the Nevada self-settled trusts statutes changed in 1999 and subsequent changes to their statute of limitations for gifting into these trusts in 2010, is the Nevada asset protection trust type of family trust.

Nevada asset protection: map of United States with Nevada state highlighted.

Of all asset protection strategies, the Nevada asset protection trust, on the surface, stands out as being one of the most secure methods of securing personal and family fortunes since the change in statutes.

Many asset protection attorneys have recommended the Nevada asset protection trust to their clients for these very reasons. A Nevada domestic asset protection trust (DAPT) is essentially an irrevocable trust instrument that has special features enabled by the statutes of the Silver State. To understand why asset protection attorneys are turning their attention to Nevada DAPTs, it helps to learn about the history of trusts and recent trends in how society perceives wealth.

The Need for an Asset Protection Trust

The 21st century has become one of the most paradoxical times in terms of how global economies are shaping the way demographic societies develop. The vanishing middle class and the change in the mechanisms that rule the redistribution of assets have become major issues of contention.

The concept of asset protection dates back to the 12th century, when the legal instruments we know as trusts today were created in England. The original purpose of trust was to protect the assets of English knights who served the Crown during the Crusades.

History shows that trusts were created for the purpose of asset protection, and the family trust was perfected over the centuries for this purpose as well as for estate planning, gifting to charities, and keeping family fortunes away from the reach of outsiders and third parties; after all, what is a family trust but an effective way of preserving wealth? A modern real estate family trust, for example, is essentially an updated version of the early trusts used by knights.

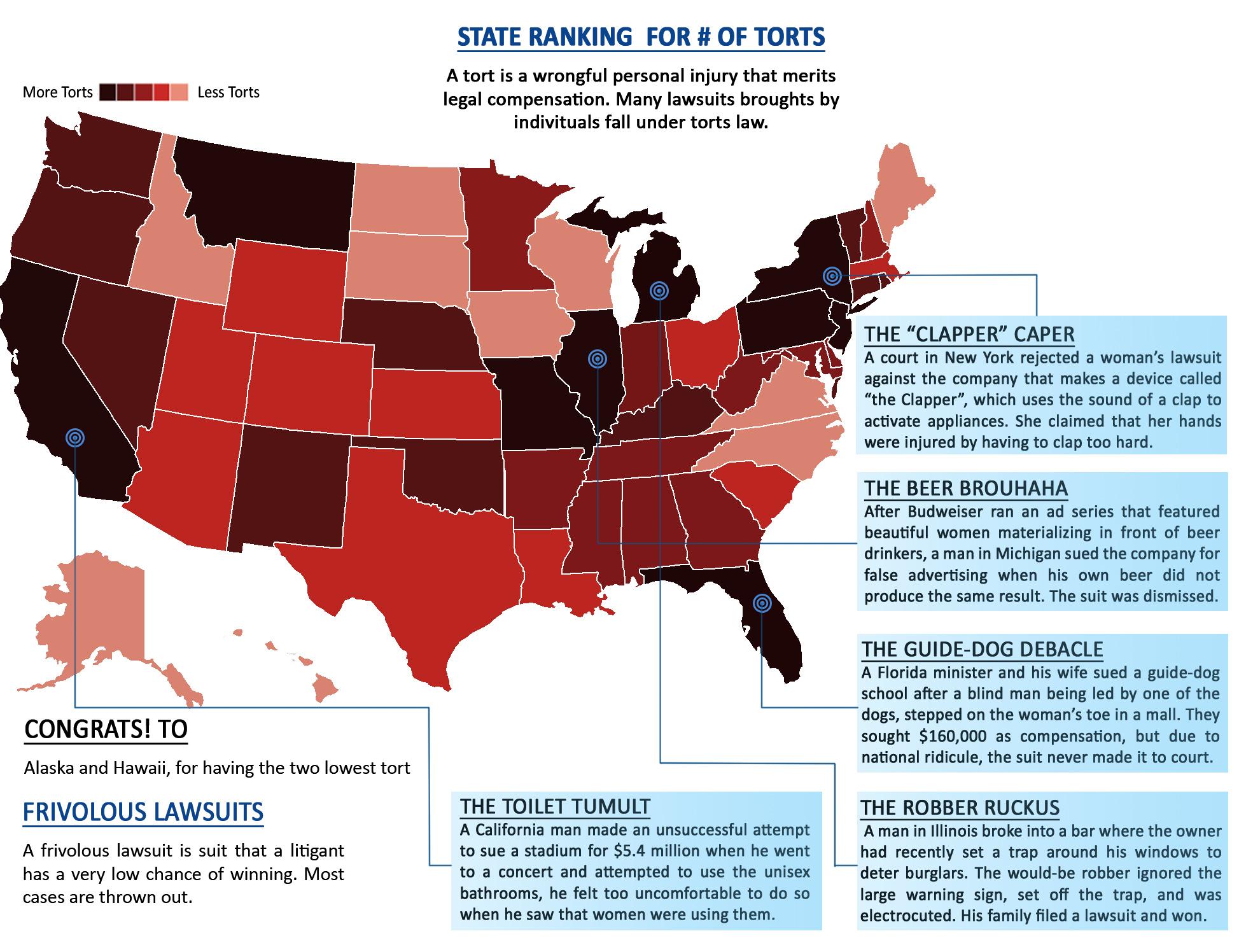

United States is the most litigious nations in the world. Map of the United States displaying state ranking of number of torts in each state. (Click on image to see larger map)

Now that we know that about the historic need for asset protection, understanding the current need becomes easier. The United States has become one of the most litigious societies in the world, and this is something that has been exacerbated with the redistribution of wealth in the 21st century.

To a certain extent, the expression “the rich get richer while the poor get poorer” has become axiomatic in modern times. The so-called “one percent” who make up the wealthiest and most powerful individuals and families in the world have indeed become wealthier over the last few decades. The United States middle class is becoming smaller every day. These changes are caused by ineffective redistribution of wealth schemes.

Individuals and families who make up the American upper middle class and above are in serious need of strong asset protection strategies for business owners such as the Nevada version of the asset protection trust. Basically, families who enjoy unencumbered assets worth $100,000, or whose annual incomes are greater than $100,000 per year, face problems that have been created by the uneven redistribution of wealth in the 21st century.

Whereas early family trusts offered protection from feudal lords, usurious creditors and zealous Crown revenue collectors, family fortunes these days are in danger of being decimated by excessive taxation, irresponsible heirs, zealous creditors, frivolous plaintiffs, gold diggers, and other unpleasant characters.

It is generally accepted that the “one percent” have become so powerful as to be considered untouchable, and thus not many people bother with trying to tap their fortunes. The truth is that those within the “one percent” make extensive use of strategies similar to the Nevada asset protection trust, which happens to enjoy many irrevocable trust advantages.

With a diminished American middle class, revenue collectors and creditors are focusing their money-grabbing efforts on the upper middle class and above because they know that they cannot penetrate the asset protection fortresses of the “one percent.” A similar philosophy is practiced by frivolous plaintiffs and gold diggers who want to make an easy score from those who are not protected by a Nevada asset protection trust.

There is no question that there is a strong need for asset protection these days, and the pesky trend of uneven wealth redistribution will continue to make the Nevada DAPT an important financial strategy.

Understanding the Nevada Asset Protection Trust

Financial planners and asset protection attorneys have been closely following the legislative action in Nevada since 1999, which is when Chapter 166 of the Revised Statutes was amended to pave the way for the creation of an irrevocable grantor trust that would become the strongest form of asset protection in the United States.

Chapter 166 of the Nevada Revised Statutes is known as the Spendthrift Trust Act, and was originally created to place restraints on voluntary and involuntary transfers from trusts to benefits. Asset protection lawyers saw that their clients could certainly benefit from an irrevocable grantor trust created under Nevada state law.

A Nevada DAPT has numerous advantages and can serve many purposes, but its most efficient use is for wealth preservation. As mentioned earlier, a Nevada asset protection trust is also known as a domestic asset protection trust (DAPT), a term that helps to differentiate these instruments from offshore trusts.

To understand the basics of a Nevada DAPT, it helps to learn how an irrevocable grantor trust works. When an asset protection attorney recommends an irrevocable grantor trust to his or her clients, it is because of the way irrevocable trust advantages can help in relation to wealth management and preservation.

An irrevocable grantor trust can be a family trust, a small business trust, or even a real estate family trust. It can also be a DAPT in the sense that it assures the protection of assets for the discretionary benefit of the grantor. As its name suggests, an irrevocable grantor trust does not normally allow for revocation or amendments once it is settled, which is why many asset protection attorneys recommend them to their clients.

As opposed to revocable trusts, which have been used as family trusts as well as real estate family trusts, irrevocable grantor trusts offer real asset protection features relative to an irrevocable grantor trust from a different state by virtue of the Nevada statutes and favorable case law. Although revocable trusts allow grantors to serve as their own trustees and beneficiaries, the revocable nature of these instruments make it too easy for creditors, plaintiffs and others seeking to tap into trust assets to convince a court to issue an order to enact revocation in their favor. Such is not the case with Nevada asset protection trusts since they enjoy the irrevocable trust advantages that create legal barriers against those who wish to claw at the trust assets.

There are two special advantages related to the creation of an irrevocable grantor trust in Nevada: First of all, this is an instrument that is designed to be completely self-settled, which means that the grantor can serve as one of the trustees for the purpose of retaining control of the assets.

The distributions and disbursements from a Nevada asset protection trust can be set up in a discretionary manner instead of being mandatory. Another powerful feature of an irrevocable grantor trust is the trust protector. This is advantage similar to the offshore trusts offered in certain Caribbean jurisdictions. When the grantor of a Nevada asset protection trust appoints a trust protector, he or she is essentially assigning a guardian angel with broad powers such as the legal right to remove trustees and to settle conflicts between beneficiaries.

If an irrevocable grantor trust is to be used as a family trust, an asset protection attorney may recommend that the grantor’s spouse and children be the initial beneficiaries so that they can share distributions. In this fashion, the trust assets enjoy greater protection.

What is a Family Trust?

One of the many irrevocable trust advantages of a Nevada asset protection trust is that it can be used to keep wealth in the family. If we pose the question “what is a family trust” to a seasoned asset protection lawyer, the answer will likely be: a legal instrument that provides an ideal ownership situation for all beneficiaries. In a family trust, relatives are usually designated as the beneficiaries of the assets, which means that they get to enjoy them without actually owning them.

Asset protection attorneys often mention the legal and financial burden of ownership when they discus family trusts. Ownership is the basis of legal claims by creditors, frivolous plaintiffs, gold diggers, freeloaders, and others who may want to claw at the family fortune. One of these claimants, for example, may want to file a lawsuit to place a lien on the apartment occupied by a grantor’s daughter who is attending college. Let’s say the claimant performed maintenance work on the apartment and thinks that he was underpaid. If this prospective plaintiff consults an attorney about this matter, chances are that he will be informed that the young lady does not really own the apartment, and that he is basically barking up the wrong tree.

Eliminating the burden of ownership is one of the greatest benefits of irrevocable trusts, but the traditional reasons for establishing a family trust can certainly be satisfied with a Nevada asset protection trust. An asset protection attorney explaining family trusts may mention that they are one of the best estate planning tools for all families, particularly for those whose members will potentially not get along in probate court.

Legendary musician Prince George Nelson’s legal estate of the Prince of Paisley Park engaged in probate court.

There is a famous someone who may have needed an asset protection attorney to review how irrevocable trust advantages could have benefited him in life. The estate of Prince George Nelson, one of the most brilliant musicians to hail from Minneapolis, is a legal mess.

The Ultimate Safeguard of a Nevada Asset Protection Trust?

As previously mentioned, Nevada’s version of the Domestic Asset Protection Trust fully came to be one of the strongest financial safeguards with a 1999 amendment to the Nevada Revised Statutes.

We have already explained that an irrevocable trust allows the grantor to create a legal instrument that he or she can retain control of as co-trustee, and with the help of a trust protector, the grantor can be also be a discretionary beneficiary. Asset protection means keeping third parties away from property, investments, valuable artwork, and generally anything else that may be of value.

Asset protection attorneys will always recommend creating a Nevada irrevocable trust when the skies are clear, which means before issues such as a divorce, lawsuits or a crash of the financial markets may come about. The reason for this recommendation can be found in the 1999 amendment to Chapter 166, the Spendthrift Trust Act of Nevada.

One section of Chapter 166 states that once a Nevada DAPT has been active for two years, the trust veil cannot be pierced. In a way, this is similar to what the state of Delaware offers to partners of limited liability companies, and it is also similar to the way some offshore trusts operate. After assets have been transferred into a Nevada asset protection trust, creditors have virtually no chance of establishing a legal claim against the assets after two years have passed.

It is important to note that the Nevada provision that locks down assets after two years applies to future creditors, which is why a Nevada DAPT can greatly help individuals or families who come into sudden wealth due to inheritances or sales of assets.

Creditors and plaintiffs who believe they are entitled to file claims against the assets in trust can only challenge the transfer of assets into the irrevocable trust, and they have two limitations in this regard. First, they must file their legal challenges within two years from the date of the trust being funded; second, they have six months to file after they discover or suspect a dubious transfer being made.

After the two aforementioned limitations, creditors and prospective plaintiffs also have the burden of presenting discovery in a timely manner. The Nevada Revised Statutes consider discovery to be on the date it appears on public records; so, if a creditor and claimant fails to perform due diligence, he or she may be late to the party with regard to filing legal claims.

Ever since the statute of limitations on fraudulent transfers for Nevada trusts was enacted, case law does not reflect a single instance of the trust veil being pierced or trust assets being clawed by creditors or claimants as long as they are within these time limitations, but there is even a better way to avoid the claims of fraudulent conveyance. This is what makes the Nevada asset protection trusts so advantageous, but prospective grantors should be thoroughly advised on how to enact the transfers in a way that makes this provision more effective – The Ultra Trust combined with the Derivative Financial Instrument™.

State

From Asset Transfer Date

From Date of Reasonable Discovery

Alaska

4 years

1 year

Delaware

4 years

1 year

Nevada

2 years

6 months

With our Ultra Trust® & Derivative Financial Instrument™

Immediately

Immediately

Finally, the recent “Panama Papers” scandal that revealed how the offshore trust industry is used by the rich and powerful is making many Americans think twice about placing their assets in the Caribbean or other jurisdictions abroad.

Although offshore trusts are highly recommended for asset protection purposes, the Panama Papers case brings up valid concerns about activists and journalists working with insiders at these offshore law firms, waiting for the right moment to leak confidential information to the press.

The last thing a grantor wants is to see his or her name listed alongside those of corrupt politicians, drug cartel financiers and disgraced athletes. The Nevada asset protection trust industry has not fallen victim to a Panama Papers-style attack, and this has a lot to do with the fact that it enjoys the support of U.S.-based law firms. Moreover, a Nevada asset protection trust is less expensive to create and maintain than its offshore counterpart.

The Nevada Asset Protection Trust and Daily Life

Asset protection trusts should not be used as checking or savings accounts; however, they can be structured in a way that allows grantors and beneficiaries to access assets in a discretionary manner.

In general, the grantor cannot be the recipient of mandatory distributions; this is a resolution that allows for maximum asset protection. Still, the grantor can be a beneficiary along with his or her spouse, children and relatives, who can enjoy discretionary distributions.

When a Nevada asset protection trust is being managed by a fiduciary trustee, the grantor and beneficiaries can agree on a discretionary distribution and make a formal request. Let’s the family agrees on a $250,000 distribution; the trustee will ensure that the request complies with the law and with the trust agreement. It may take a few days to complete the distribution in a manner that does not pierce the trust veil; for this reason, a Nevada DAPT cannot be considered to have the same flexibility as a money market account with a Visa debit card.

With regard to the minimum assets level at which asset protection trusts can be recommended, the situations will vary. In general, families with net worth of at least $1 million are good candidates for irrevocable trusts based in Nevada. Nonetheless, asset protection attorneys also see young families with annual incomes of $100,000 interested in asset protection; these are usually families who are holding on to investments projected to drastically increase in value. In other words, they may not be the target of money grabbers yet, but they see their situation changing in the near future.

As previously mentioned, asset protection lawyers set up irrevocable trusts in ways that will not arise suspicion among third parties and officials. To this effect, a law firm or trust protector may not recommend depositing every single asset item in trust if doing so may seem as a fraudulent action. This type of advice may extend to distributions, which should not be made in a manner that makes an irrevocable trust look like an ATM.

While it is true that Nevada created some great statutes making the Nevada Asset Protection Trust extremely good, making a Nevada Ultra Trust and combining it with the Derivative Financial InstrumentTM is even better.

The Ultra Trust® has been around for thirty years; being challenged by some of the most powerful groups in the country: the Attorney General of New York, the Attorney General of California, the IRS, and the US Attorney in Washington D.C., among others, without a single detrimental client outcome. Why not put the odds in your corner?

Rocco Beatrice, CPA, MST, MBA, Managing Director, Estate Street Partners, LLC.

Mr. Beatrice is an asset protection award winning trust and estate planning expert.

Asset Protection: Part 3 of 4, by Rocco Beatrice, Sr.

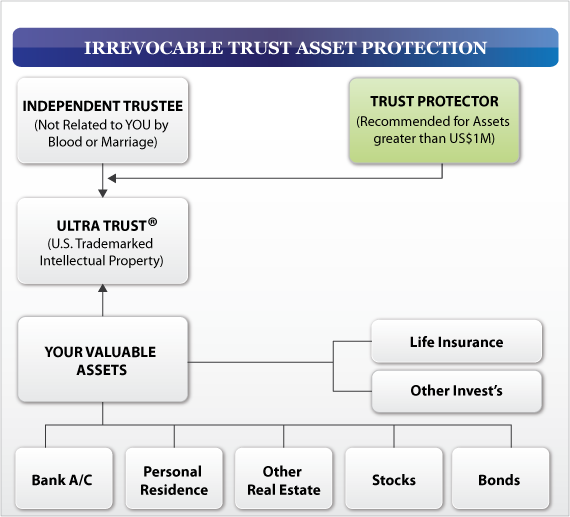

Our Ultra Trust®

Our Ultra Trust® is an intellectual property right registered with the U. S. Patent Office, financially engineered to remove yourself from the probability of becoming the next creditor victim. This whole website www.ultratrust.com is devoted to the best methods and strategies of asset protection and our Ultra Trust®.

What’s an asset protection trust? What’s a Trust?

A “TRUST” is nothing more than a “CONTRACT” between the person who wants asset protection (the Settlor), the person who will manage the assets (the Trustee), for the benefit of all Beneficiaries – whomever you choose.

The Trust Agreement requires the transfer of assets to be protected from the original owner (Settlor) to a legal entity for the purpose for which the Trust Agreement was created.

What type of trust, Grantor, or Non Grantor? What’s the distinction? A Grantor Trust take a special consequence within the tax code. Our Ultra Trust® is a “Grantor-Type Trust” for tax purposes is treated as a disregarded legal entity. The disregarded entity is “Income Tax Neutral” meaning that the original Grantor retained strings attached so that for purposes of the IRS income tax reporting, the original owner (grantor(s) retains the assets in his complete control, thus our Ultra Trust® is a “pass-through” to his form 1040 i.e. real estate tax deduction and mortgage interest deduction on his person income tax return, INCOME TAX NEUTRAL.

Revocable, Irrevocable trust, what’s that mean? Revocable is when the original person with the assets transfers (repositions) the assets to a trust with strings attached. The Grantor, the Trustee, and the Beneficiary are the same person. Effectively you have done nothing, because it’s between you and you for the benefit of you. A revocable trust does absolutely nothing for asset protection because you can be forced to revoke it by a creditor or court. Many lawyers recommend revocable trusts for avoiding probate, recognizing that the trust is not worth the paper it’s written on for protecting assets against frivolous lawsuits and the avoidance of estate taxes or the 5 year Medicaid spend-down provisions.

IRREVOCABLE TRUSTS

A properly written, executed, and funded irrevocable trust, such as the Ultra Trust®, is an extremely powerful asset protection device. The opposite of revocable is “irrevocable.” No strings are attached by the Grantor. “Irrevocable” means that nobody can force you to revoke it, and thus if executed correctly, gives phenomenal asset protection benefits. Once assets are transferred from the Grantor(s) to the Trust, the Grantor has no control, other than possibly some very limited powers. It’s this clear-cut lack of control and ownership that makes this trust very powerful asset protection device. You can’t be sued for assets you no longer own or control. The fiduciary duty of an independent trustee of an irrevocable trust is critical and viewed by the courts as golden. The Trustee must preserve the assets entrusted to him at any cost. Courts take a very unpleasant view on a Trustee who has abused his fiduciary duty. Breach of fiduciary duties by a Trustee could be considered and intentional tort subject to punitive damages.

OUR irrevocable Ultra Trust® asset protection trust when combined with a Limited Liability Company (LLC) or Family Limited Partnership (FLP) is an asset protection fortress, short of a foreign asset protection trust. A foreign asset protection trust is the Rolls Royce of asset protection, the irrevocable trust with an LLC is the Cadillac / Mercedes / Lexis.

WHAT’S A TRUST PROTECTOR? You won’t get this from your lawyer

Because you are concerned about the power and discretion granted to the Trustee, we add the Trust Protector to create the checks and balances you need to feel comfortable, while reinforcing the bullet-proofing of our Ultra Trust®

The power of the Trust Protector is derived from the Trust Contract. The Agreement sets forth the dual function of the Trustee and the Trust Protector to give you a backup plan if the Trustee is not cooperative. While the Trustee can be a bank, CPA, trust company, or other financial institution, the Trust Protector is usually a person close to the family, a CPA, accountant, or lawyer who is already the family consiglieri.

The Trust Protector’s powers can take any form, limited only by the wishes of the Grantor(s) and their imagination. Generally, the powers granted the Trust Protector are:

1. Ability to remove or replace the Trustee without any explanation (Donald Trump style: “You’re Fired.” Often this is the only power granted to the Trust Protector. In cases where the Trustee is a corporate body (bank, trust company, insurance company, or professional trustee) if the Trustee is unresponsive or not performing to the Trust Agreement for the benefit of all Beneficiaries, or changes in management, or investment choices, the Trust Protector can fire and replace the Trustee, at will, without explanation to the current Trustee.

2. Ability to change the Trust’s situs to take advantage of law changes or necessary steps to act in the best interest of beneficiaries if they move from low tax states to high tax states, i.e. from CA or NY (high tax states) to NH, TX, or NV (low tax states) or changes in laws occurring long after the initial implementation of the Trust Agreement.

3. Ability to resolve deadlocks between co-trustees or in squabbling between the Trustee and/or Beneficiaries.

4. Ability to veto spending over a certain amount. This level of control is significant if disbursements of the Trust are in excess of pre-arranged amount requiring two signatures, the Trustee and the Trust Protector i.e. in excess of $20,000.

5. Ability to veto distributions to Beneficiaries. Before distributions are to occur the Trust Protector may want to investigate the financial stability of the Beneficiaries. For example, if the beneficiary is being sued, The Trust Protector may withhold distributions, or the Beneficiary is undergoing divorce proceedings, or the Beneficiary may be too young, is under duress, mentally incompetent, unable to manage, or otherwise unavailable. The Trust Protector can override/veto the Trustee and withhold distributions temporarily or permanently make other arrangements such as buy the assets necessary for the benefit of the beneficiary (buy a house, a car, sign a rental agreement, but have the Trust own the assets, make loans, or make other provisions.

6. Ability to veto investment decisions. This checking and balancing of investment decisions are based on the Trust Protector’s experience, prudence, and the Trust Agreement guidelines in protecting the assets for the Beneficiaries.

7. Ability to sue and defend lawsuits against the Trust assets. The fiduciary duty of the Trustee and The Trust Protector as to save the assets of the Trust, at any cost, for the benefit of all classes of Beneficiaries.

8. Ability to terminate the Trust. If in the opinion of the Trust Protector there are insufficient funds or the cost of administration is greater than available cost/benefit, the Trust Protector may terminate the Trust, as for example, if all beneficiaries have received their distributions based on age (over the age of 21) and there’s one minor beneficiary currently 10 years old, and there aren’t enough assets to administer the Trust for the next 11 years, the Trust Protector has the power to make the final distribution and terminate the Trust.

The Trust Protector’s role is created by the Trust Agreement to add an additional layer of protection and is usually a person most familiar with the Grantor’s long term financial and personal goals. A Trust Protector usually is the balance of power between the Trust Agreement, the Trustee, The Grantor, and the Beneficiaries. Neither the Trustee or the Trust Protector should be anyone related to the family by blood or marriage. Both positions should be independent of each other acting in the long-term interest of the beneficiaries.

“Helping our clients resolve their problems quickly, effectively, and decisively.”

The Ultra Trust® “Precise Wealth Repositioning System”

This statement is required by IRS regulations (31 CFR Part 10, 10.35): Circular 230 disclaimer: To ensure compliance with requirements imposed by the IRS, we inform you that any U.S. federal tax advice contained in this communication (including any attachments) is not intended or written to be used, and cannot be used, for the purpose of (i) avoiding penalties under the Internal Revenue Code or (ii) promoting, marketing or recommending to another party any transaction or matter addressed herein.

What is a Trust Protector and Do I Really Need One? Can it protect me and my money? How does a Trust Protector act as a check and balance? What does a trust protector do exactly?

In our gratification-obsessed society, everything is subject to change – even our most intimate relationships.

Today, you’re in a very different place than 10 or 15 years ago. You’ve probably lost touch with many of your old friends. You might live in a different household, a different job, and practice different hobbies. The past is gone forever.

15 years from today, chances are good that things will look different still. While a typical irrevocable trust provides the strongest framework for preserving your hard-earned assets, it lacks the flexibility that your ever-changing circumstances demand.

Simply put, you need a trust protector to back you up. That’s why it’s so important to upgrade to a Trust package with the special power of appointment and trust protector. This added protection gives you the flexibility to respond to unforeseen changes and dilemmas.

Why a Trust Protector?

In many countries, trust protectors are a requirement in an estate plan. While this isn’t true of the United States, legal experts are virtually unanimous in their agreement that trust protectors are a crucial component of any irrevocable trust and estate planning.

A trust protector is a third-party individual – separate from the trustee – who understands the dynamics of your family. He acts as a check on the actions of the trustee and maintains a fiduciary responsibility to the trust. By protecting the assets of the trust from the inevitable squabbles that occur whenever there’s money to be had, he lives up to his name.

The validity of the trust protector has been upheld time and again. The court’s decision in McLean Irrevocable Trust v. Patrick Davis, P.C. (Mo. Ct. App. 2009) clearly establishes the legal basis for the office’s existence and provides a framework for the definition of its roles.

A subsequent case brought by the same plaintiff, McLean Irrevocable Trust v. Ponder, is even more pointed. Here, the court ruled that a trust protector has a fiduciary obligation to take action against unresponsive, incompetent or malevolent trustees.

The trust protector doesn’t have the luxury of looking the other way. He’s like an insurance policy that automatically comes to the rescue whenever a trust’s integrity is threatened – just like the crucial insurance policies that we carry on our homes, cars, and businesses. The trust protector provides the same backup planning.

Serve as a mediator for squabbling trustees and beneficiaries

Veto large disbursements in accordance with existing agreements

Change the trust’s state of incorporation if you relocate or to avoid taxes

Veto questionable investment decisions and beneficiary distributions

Address legal challenges to the trust

Terminate a dwindling or unnecessary trust

The true beauty of the role, though, lies in its versatility. A trust protector can do as much or as little as you need. He’s the perfect ally in any trust-related jam.

Let’s see 2 real life examples of what a trust protector can do.

Best Friends, Just Not for Life

Meet Sal.

After graduating from college, Sal started painting houses to make ends meet. Two summers in, he had saved up enough to buy a truck and some tools. Before long, he was working as a foreman for a contracting company that replaced roofs, wiring systems, and insulation in aging suburban homes.

Soon enough, he got sick of repairing other peoples’ homes and decided to buy and fix up his own. His first buy was a sad-looking foreclosure in a working-class neighborhood just outside of Philly, but he worked on it until it was the pride of the block. He booked a cool $100,000 profit from its sale.

Soon, Sal was a mini-real estate mogul who managed a portfolio of eight properties in the area. He had a great system: He’d fix up each house, sell it for well above market price, book the profits and plow the principal back into a new property.

To protect his years of hard work and preserve a legacy for his growing family, Sal set up an irrevocable trust and named his young son as its sole beneficiary. He chose Dave, his former college roommate, to be its trustee. Dave came from a well-off family, so he understood how to manage money and he refused the offer of being paid to serve as trustee.

The experience wasn’t always conflict-free. Sal had a knack for identifying market peaks, but Dave didn’t always listen to his advice. Sal’s properties were always the trust’s most valuable assets, and the proceeds from their sales provided much-needed liquidity.

Fifteen years later, matters have come to a head. Sal’s son has been helping his dad fix up houses for years and finally wants what – he thinks – is due to him. He approaches Dave and proposes using $100,000 of the trust’s funds to buy a late-model Porsche for his personal use. As a wealthy man who is used to having a nice ride, Dave happily agrees to the plan.

Sal is disgusted. Dave has refused to sell any houses for several years, so the trust is low on cash. A frivolous car purchase would further risk the solvency of the trust and, should an unforeseen event occur, potentially jeopardize everything Sal has achieved.

If Sal had a trust protector, he could put a stop to this nonsense by firing Dave or at least vetoing his questionable purchasing decision. Sal’s son certainly deserves a decent vehicle, but perhaps the trust protector could have forced the trustee to purchase a Camry over a Carrera.

As it stands, Sal can do nothing but watch Dave approve the purchase of a car that he doesn’t really approve of.

Let’s turn to Susan.

As an emergency-medicine doctor, Susan has earned a tidy sum over the years. She’s approaching retirement, though, and her family’s history of metastatic breast cancer has given her pause. To ensure that she qualifies for government medical benefits in the event of a grave illness, she sets up an irrevocable trust with her three adult children as beneficiaries.

As an experienced attorney who’s also nearing retirement, Susan’s brother-in-law Paul is more than happy to serve as the trustee. Things start off well, but Susan’s mother-in-law falls ill about a year later. With her father-in-law lacking the strength to care for her and Paul’s career winding down, Paul steps up to care for her. Susan and her husband, a busy vice president at a local manufacturing company, are grateful.

As Paul’s mother becomes sicker, caring for her turns into a full-time job, and Paul retires a year ahead of schedule to accommodate her needs. Since his dad isn’t in great shape, Paul is in heavy demand. He spends several hours per day at his parents’ house, handling everything from laundry and cooking to basic structural repairs and drug administration.

Paul is a fundamentally decent man who’s under an incredible amount of strain. Meanwhile, Susan remains wrapped up in her demanding career. As their parents’ medical bills pile up, Paul tentatively begins to use the trust’s liquid assets to pay for wound-care supplies, prescription drugs, orthopedic equipment and other important medical supplies. Later, he starts withdrawing modest amounts of cash to pay for their food and home supplies. He never asks for his brother’s permission or stops to consider the ethical ramifications of his actions, but he assumes that his brother and sister-in-law would approve.

Eventually, though, Paul crosses a line. Instead of using the trust’s funds to pay for medical supplies or sustenance for his ailing parents, he begins to make deposits into his own private bank account. He convinces himself that he’s merely being compensated for his time, but the truth is clear: He’s pilfering funds from Susan’s trust without her knowledge.

When Susan finds out, she’s placed in a tricky bind because Paul is a family member taking care of her father-in-law. After all, is she really going to sue Paul after he has been so helpful? While she’s sympathetic to the needs of her husband’s parents, she’s furious that her nest egg is being used in an ethically questionable manner. Without a trust protector, though, she can’t remove Paul as trustee or check his actions in any meaningful way. She’s stuck – and her legacy is threatened as a result.

Protecting Your Assets for All

It’s true that some individuals who use irrevocable trusts and trust protectors to preserve their legacies are quite well-off, but most are regular folks who have worked hard their whole lives and need a safe, secure means to protect their assets.

Maybe they’ve built a moderately successful business but don’t want to “spend down” or forgo pass-through profits to qualify for Medicaid. Perhaps they’ve inherited a modest nest egg from a deceased parent that they hope to preserve for their kids.

Maybe they just don’t want their heirs to pay probate and estate taxes on whatever’s left over when they’re gone. Who can blame them? It was their blood, sweat and tears that earned this nest egg.

Whatever the reason for their existence, irrevocable trusts have proven their worth time after time for the last 150 years in courts throughout the country. When combined with a powerful insurance policy – the trust protector – these instruments are virtually unstoppable. See the legal precedents for the Ultra Trust irrevocable trust here.

This begs the question: If you’re willing to pay for insurance on your home, why wouldn’t you do the same for your legacy? After all, your trust protector might ultimately be responsible for preserving your home – and everything else that’s rightfully yours – for your loved ones.

Learn about the "latest inside secrets to wealth-building, tax-saving tips and strategies" for your secure financial roadmap...PLUS you'll receive a FREE downloadable eBook on precisely how the Ultra Trust® - the Irrevocable Trust Asset Protection program developed by our Expert Estate Planner - can save you thousands of dollars of legal fees and hundreds of hours of time by avoiding lawsuits; legal loophole to reduce your taxes; secure your privacy, preserve your money, and protect your assets.

We never share your email information with third parties. We collect your email address so you can benefit from money-saving tips. For more information please review our privacy policy.

How does one protect assets before or during a divorce? Common steps to divorce asset protection for gifts, family heirlooms, and real estate. You will need to consult with a divorce lawyer, professional appraiser, and estate planner. Definition of Equitable Distribution and fair market value of assets in divorce.

Last wills and testament with a revocable living trust

A common question considered by individuals who are preparing their estate planning is whether a will or a living trust would be a better option to serve their estate planning needs. Everyone has slightly different goals and nobody has the exact same needs. There are many benefits to choosing a Revocable Living trust instead of a will, but there are also some drawbacks. Which is better is a very personal decision. Many people use both a will and a trust to ensure that their assets are distributed according to their wishes, but they are very different. Still other people use an irrevocable trust instead of a living revocable trust. Here are the highlights of the top 5 pros and cons of the living revocable trust:

1. Revocable Living trusts do not go through probate – Pro

One of the primary reasons a person might choose a living revocable trust to distribute his or her estate is that trusts allow the heirs to avoid going through probate. Probate is the legal process of distributing assets under a will, and it requires going to court. The administrative costs associated with probate can be as high as six to ten percent of the estate’s value, which could get expensive when an estate has substantial assets. If there are challenges or issues it is likely going to be closer to ten percent than six.

Revocable Living trusts do not avoid all costs associated with probate – Con

The estate must still pay state or federal estate taxes or other taxes, which means that the administrator may have to hire an accountant or tax attorney to assist. An estate attorney may still be needed to assist with transferring assets from the revocable living trust to the beneficiaries. The successor trustee may also be entitled to a fee for the time spent administering the trust.

2. Faster distribution of assets – Pro

The law requires that probate be completed in each state where a person owns property at the time of his or her death. Thus, the more states where a person has assets, the more expensive probate will be. Probate can also be time-consuming, especially if the process must be completed in several states. Therefore, having a revocable trust instead of a will may reduce the amount of time that passes before assets are transferred to the Settlor’s heirs.

Revocable Living trusts carry upfront costs – Con

There are still some costs associated with establishing a trust. It may be necessary to pay an attorney to create the trust, write necessary documents, and transfer ownership of personal assets into the trust. The process could cost anywhere from $1,000 to $2,500. There may also be costs associated with settling the estate if the heirs or beneficiaries to the trust dispute the asset distribution or validity of the trust documents. The estate may have to pay to value assets in the trust or settle creditor claims against trust assets. Therefore, establishing a trust doesn’t avoid one hundred percent of the costs of probate, but many individuals could likely still save money.

3. Revocable Living trusts’ distribution is private – Pro

Another big advantage to avoiding probate is that probate proceedings are public. A person who wishes to keep his or her finances private and protect the heirs from public scrutiny may prefer to create a revocable trust instead. The contents of trust documents are not public record. If it becomes necessary to probate assets not included in the trust, the probate records would note the existence of a trust, but not the contents or the value of the assets. Many people choose to create a revocable trust for this reason.

4. The Settlor retains control of assets during life – Pro

A revocable trust allows the Settlor to maintain control of assets during his or her lifespan. Assets that are acquired after the trust is formed may be added, and the Settlor may also remove and sell assets, change beneficiaries, or choose to dissolve the trust entirely. Nothing is final during the Settlor’s lifetime.

The Settlor needs to retitle the assets but for asset protection she still owns them – Con

The Settlor must retitle all assets in the trust’s name. Transferred property belongs to the trust, but because any part of the trust can be revoked at any time, including dissolving the trust, that means a creditor can force you to do the same and can get access. The Settlor does not receive tax benefits from the trust during life and will be required to keep impeccable bookkeeping records to help avoid issues down the road.

5. A trustee or power of attorney may help manage assets – Pro

The Settlor is often a trustee, but it is possible appoint a successor trustee, which gives someone else the authority to make decisions if the Settlor becomes mentally or physically incapacitated. A durable power of attorney may have some of the same powers as a successor Trustee, but in neither case does the trustee or a person with power of attorney own the assets he or she manages. In addition, assets managed by a power of attorney rather than a trustee must still go through probate when the Settlor passes away.

Revocable Living trust does not receive the same tax benefits as an estate – Con

An estate is a separate legal entity like an irrevocable trust may enjoy significant tax benefits after the Settlor passes away. A revocable trust does not receive these same benefits. However, depending on the size of the estate, some people may find it more desirable to avoid probate administration costs even if it means spending more in taxes.

Revocable Living trusts does not apply to assets that are not included – Con

Most people who establish a revocable trust still need to draft a will to address the distribution of any assets that are not transferred into to the trust. If a mistake is made or the Settlor prefers to keep some assets liquid, a pour-over will tells the administrator of the estate what to do with those remaining assets. A will directs the distribution of assets acquired after the trust is funded, if the Settlor is not able to transfer the asset before death. The will controls the distribution of personal property like photographs, clothing, and household items. Absent a will, any assets not included in the trust would be distributed according to state laws on intestate succession. These laws divide property depending on a person’s relationship to the Settlor and do not consider how the deceased individual might have wanted to distribute the assets.

Every plan is different depending on the needs of the individual. Contact an expert to help you make that assessment and evaluate all of your options in order to come to a solution that makes sense for you and your family.

Learn about the "latest inside secrets to wealth-building, tax-saving tips and strategies" for your secure financial roadmap...PLUS you'll receive a FREE downloadable eBook on precisely how the Ultra Trust® - the Irrevocable Trust Asset Protection program developed by our Expert Estate Planner - can save you thousands of dollars of legal fees and hundreds of hours of time by avoiding lawsuits; legal loophole to reduce your taxes; secure your privacy, preserve your money, and protect your assets.

We never share your email information with third parties. We collect your email address so you can benefit from money-saving tips. For more information please review our privacy policy.

How to Save $100,000 on Long Term Care Insurance Costs & Alternatives

If you are considering purchasing long term care insurance, let me cut through all of the noise and share with you the dirty secrets of the long term care insurance industry which will help you save $100,000 on Long Term Care Insurance Costs.

Secrets to cutting your long term care insurance expenses

Hidden Secret #1

Long Term Care Policies are very tricky. Pay close attention for the following details. Some Policies:

Don’t cover the full cost of care:

They may only cover $200 per day when care costs $400

Don’t increase coverage over time:

Costs for care go up every year and your coverage should be adjusted for inflation

Only cover costs in the nursing home for one or two years:

The average stay is more than 2 years, will you be covered for your entire stay?

Only cover certain types of care

Think nursing home vs. assisted living

Don’t consider if you actually need to go into a nursing home.

Only 50% of the population needs to go to a nursing home on average – are you wasting $100K on something that you will never need?

Hidden Secret #2

You don’t need a LTC policy. What, you ask? You actually don’t need to spend $100,000 on a long term care policy if you know the rules and how the system works.

Let’s compare long term care insurance costs to other options that you have available:

The true cost of long term care insurance can vary significantly from 80K to 150K per spouse depending on age, health, and the quality of the policy coverage. If you are searching for long term care insurance today, you are more than 5 years from the time that you expect to need long term care services. This is because insurance companies would never sell a policy to someone seeking to use it in the foreseeable future or it would be so expensive it would not make economic sense to purchase. This is very important – we will see why in a moment. If our assumptions are true, then you have a much better option available to you than a long term care insurance policy, solidifying the case that you will be able to save $100,000 per spouse. Let me explain:

How Long Term Care Works

One just needs to understand the rules and how the system works. Typically, you are not the one that gets to decide whether you are going to a nursing home or not. Your doctor is the first gatekeeper who makes that decision. The first step will be to send you to a “rehab” center. This typically initiates a social worker who oversees your case – the second gatekeeper. Medicare (not Medicaid) typically pays for the first 20 days of care. If there is any chance of you returning home, Medicare will pay for up to an additional 80 days.

If the doctor and social worker decide that you cannot go home they will send you to a nursing home, regardless of what you want, and the facility only has a single major question:

How are you planning to pay your for your nursing home stay?

Do you have LTC insurance to pay for the nursing home stay?

Do you have assets that will cover the bill of $8-14,000 per month?

If the answer to both of these questions is no then the nursing home will just send the bills to Medicaid! And regardless of your payment method they are required by law to treat all patients with the same level of care. So you must be asking yourself, “How does one get to answer NO to both of these questions while staying 100% legal and above board if one potentially has a home, a business, and/or savings?” It is actually really simple.

Let’s back up a minute. So if you have assets in your name at any point during the last 5 years, you are required to use them to pay for your own care. Not all assets are created equally however; some assets are “counted” and some are “not counted” in the calculation. The assets that you need to spend-down for your own care before medicaid takes over payments include the following:

Home

If you are married, they won’t force you to sell it right away, but rather will put a lien on it so when it is eventually sold, they will get their money

Rental Properties

Cash in your bank account

Stocks, Bonds, CD’s, other investments

Family Business (LLC, S-Corp, C-Corp)

Assets not required to use for nursing home care before Medicaid helps:

Car in the patient’s name (there is no established limit on the value)

Prepaid Funeral expense

Medicaid-Approved Annuity (This means that the state is the first beneficiary of the annuity – only to be used for emergency cases)

So if you do not legally own the assets described above during the previous 5 years, you qualify for Medicaid to pay for your care. You may have previously lived in a $1M house and drive a $100K Mercedes, but if the title does not have your name on it, it is not counted as assets available for your care!

The Catch and the Better Alternative to Long Term Care Insurance

The first catch is that you need to act immediately – more specifically, you need to act at least 5 years before you need to go into a long term care facility. Since nobody knows when their health is going to take a turn for the worst, you need to act pronto.

Catch number two is that you must be willing to reposition assets into an irrevocable trust for the benefit of your kids or someone else. A living trust or a revocable trust will not suffice. Here is the difference between revocable and irrevocable trusts. If you do it correctly, you will still be able to use the assets, buy and sell stock, pay your bills every month, travel the world, and buy and sell the your home through the trust.

The reality is that you can’t take the assets with you when you go to heaven, but with the trust, the kids don’t get the assets until you say-so. This could be at the time that both you and your spouse go to heaven, or it could be 20 years after you pass away with incentive clauses so your kids don’t blow all of the money foolishly (and your 50+ years of hard work to save them either).

The great part is that YOU get to write the rules and stipulations and you get to change the rules as long as you are alive. We can help you come up with good rules for you and your situation, but you have the final say and are always in control of when and where you want the assets to go. We personally have helped thousands with this exact scenario.

The fact is that there is so much misinformation about irrevocable trusts that most people get intimidated for no good reason. Not every attorney that calls themselves an estate planning expert truly knows everything about trusts. If properly drafted, executed, and funded, an irrevocable trust can be extremely flexible while at the same time hold your prized possessions on your behalf.

If you leave your wallet at home, I can guarantee that you will not get pick-pocketed walking down the street. You don’t need your wallet in your pocket in order to buy things at the store – you just need your promise (credit) that the merchant will eventually get paid.

So for the cost of repositioning the assets listed above into an irrevocable trust, you can save more than $100,000 per spouse for long term care insurance. Similar to everyone putting money into an IRA in order to take an income tax deduction, these are the rules of the game created by Congress and everyone has the obligation to optimize their situation in the best way possible based on the rules we are given. When the rules change, we will be the first to update our strategies, but until then, it makes the most sense to play by the rules and save $100,000.

How is the Author Qualified to Share His opinion?

Rocco Beatrice is Managing Director of Estate Street Partners and has 31 years of experience in estate planning, asset protection, and Medicaid planning. Mr. Beatrice is a CPA, with a masters in taxation, a Certified Medicaid Planner, a Certified Asset Protection Planner, and a Certified Wealth Protection Planner. He has taught thousands of clients and other attorneys about asset protection and estate planning for decades. For a free evaluation of your specific situation call us now at (888) 538-5872. If you feel like you don’t need to speak to anyone and are ready to take action right now, visit MyUltraTrust.com and get protected with a personalized do-it-yourself irrevocable trust in a less than an hour with a $65K guarantee and a Better Business Bureau A+ level customer service.

Learn about the "latest inside secrets to wealth-building, tax-saving tips and strategies" for your secure financial roadmap...PLUS you'll receive a FREE downloadable eBook on precisely how the Ultra Trust® - the Irrevocable Trust Asset Protection program developed by our Expert Estate Planner - can save you thousands of dollars of legal fees and hundreds of hours of time by avoiding lawsuits; legal loophole to reduce your taxes; secure your privacy, preserve your money, and protect your assets.

We never share your email information with third parties. We collect your email address so you can benefit from money-saving tips. For more information please review our privacy policy.

Why Do Marriages Fail? Can Prenuptials Agreements Prevent Divorce?

Can a premarital agreement help in your marriage? Is there some better way to protect your assets and marriage at the same time?

Why do so many marriages fail in the United States? Let us count the reasons: A 2012 survey among relationship counselors conducted by online relationships and advice site YourTango.com revealed that infidelity and lack of interest in married life are often cited as the most significant motives couples mention when they get divorced; however, 74 percent of experts believe that disagreements about money are strong predictors of marital separation.

All civil unions have certain monetary expectations. Spouses must be prepared to provide financial support to one another, and they are expected to share the property and assets they acquire throughout the marriage. A spouse refusing to provide financial support despite having the means to do so can be construed as grounds for divorce in some states.

Many couples who feel that eliminating monetary constraints from their marriage will help them stave off divorce are likely to sign a prenuptial agreement before tying the knot. They are certainly onto something here, but they are not choosing the correct legal instrument.

The best way to keep premarital assets separate does not even require the signature or knowledge of both parties. Irrevocable trusts are the most divorce-proof legal instruments for keeping absolute control and ownership of separate assets. These trusts are commonly used for formidable asset protection and estate planning purposes, and they are even better in divorce situations.

Secure Assets Make Stronger Marriages

Relationship counselors and legal analysts say that the laws regulating the distribution of assets in divorce can actually encourage it. Ideally, couples should be able to formulate and agree to the financial terms of their marriages without state laws interfering. For this reason, many engaged couples seek prenuptial agreements as a way to improve upon the laws.