In today’s world, legal disputes are common. However, not all claims are genuine. Frivolous Lawsuits are legal claims lacking any serious legal basis. Often these particular cases will pressure the defendant into settlement rather than actual justice. Although many lawsuits are real, others are created to take the money.

The cost of defending an unfounded claim can be considerable financially and emotionally. Legal fees can rack up quickly even if the case does not have merit. Business owners, professionals, and high-net-worth individuals are particularly vulnerable to such attacks.

It is necessary to understand how a frivolous litigation works. There are several planning strategies that can reduce your asset exposure. This guide outlines the problem of fake claims, compares avoidance techniques and offers practical advice on protecting your finances.

Objectives of the Frivolous Lawsuit

Frivolous lawsuits have no legal basis and no factual foundation. They could use exaggerated claims or insufficient evidence. Courts can dismiss cases like these, but dismissal doesn’t eliminate defense cost.

Legal systems typically give plaintiffs the power to file a claim before assessing their merit. Defendants must respond to claims regardless of strength. Expenses and commitments of time are substantial even if discounted.

| Feature | Legitimate Lawsuit | Frivolous Lawsuit |

| Legal Basis | Supported by evidence | Weak or unsupported claims |

| Intent | Seek justice or compensation | Pressure settlement |

| Court Evaluation | Proceed based on merit | Often dismissed early |

| Financial Impact | Case-specific | High defense cost |

| Resolution Timeline | Structured legal process | May end in quick dismissal |

Courts dissuade baseless lawsuits but the cost is still real. Defense lawyers should react, gather evidence, and file motions.

High wealth increases visibility risk for individuals. Public records can indicate wealth exposure and attract claims.

Effective planning can help reduce vulnerability and deter litigation

The Elevated Risks Faced by Affluent Individuals.

Wealth and Identifiable Resources

Business people and professionals seem to be financially okay. Visible assets might incite aggressive legal actions.

Access to public property records and business registration enhances transparency. This visibility means the court will have more claims asking for quick settlements.

Liability Exposure and Insurance Gaps

Too little liability coverage risks finances. Insufficient protection can make personal assets accessible.

Professional liability risk differs by industry. Members of the medical profession and executives often have higher exposure.

Important risk factors is

- Major property ownership.

- Forms of Business Ownership

- Restricted liability insurance.

- Online professional profile.

When we understand the risks, we can take actions to avoid them.

Psychological and Money Problem

Fighting unconscionable actions causes nervousness. Legal action takes time, documents & legal fees.

A case that lacks merit becomes the subject of settlement pressure due to cost escalation. Protecting your assets can reduce a potential plaintiff’s ability to win.

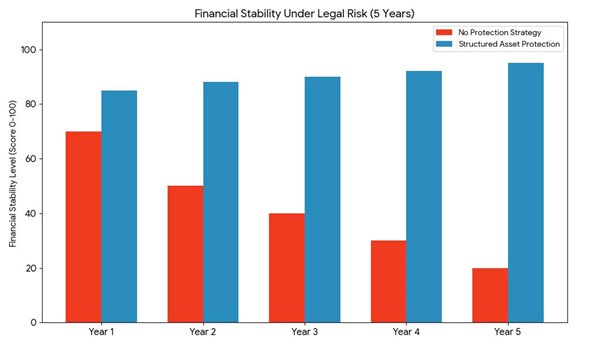

Liability Risk: Comparison of Asset Protection Strategies

A proactive approach is the best offence. Asset protection strategies vary a great deal in scope and complexity.

- Without management, we see the financial position declining year-on-year due to the build-up of potential legal fees and the exposure of assets which may ultimately result in the reduction in net means.

- Using structured protection, such as Trustee protection, limited liability entities and umbrella insurance, ensures that stability compounds over time or remains unchanged in the event of litigation.

- In essence, it is better to prepare than react. When a risk manifests and the person has legal boundaries in place, the disruption is much smaller than when one has no protection at all.

Tips for Reducing Exposure to Frivolous Claims

Strategy must be proactive and layered.

Put legal shields in place

Trust devices can protect property from attachment. An LLC can separate personal and business assets.

Consulting experienced legal advisors ensures compliance with jurisdictional requirements. Before litigation, there should be a proper structure.

Enhance Insurance Coverage

Umbrella liability insurance provides an extra layer of coverage. Professional liability insurance takes care of risks unique to various industries.

Periodic review of your policy ensures sufficient coverage updates as asset value increases.

Think of these protective actions

- Establish trusts for asset protection.

- Distinctly separate business and personal finances.

- Keep liability insurance current.

- Keep a record of transactions.

Records help prove guilt or innocence in court.

Uphold Professional Standards

Abiding by rules minimizes your risk. Contracts having no ambiguity and a clear communication channel can help reduce dispute chances.

Regular audits improve operational integrity. The planning of risk management shows due diligence.

Cultivating Resilience Against Legal Abuse

Frivolous lawsuits threaten real dollars even though they have no merit. Cost of defense alone can put pressure on resources and settlement.

High-asset people and business owners are exposed to higher risks. UltraTrust focuses on strategic planning to lessen the chance of claims before they happen.

While the legal system can reject frivolous lawsuits, proactive planning is important. Asset protection aimed at preserving wealth and ensuring financial stability in a volatile world.

When responsibility is planned, uncertainty becomes security Properly structured asset protection frameworks instill confidence and fortitude to withstand unwanted litigation.

Common questions about this article

These answers summarize the topic in plain English so readers can move from the article into the next practical planning page.

What is the main takeaway from "Frivolous Lawsuits: Protecting Yourself from Unwarranted Claims"?

In today’s world, legal disputes are common. However, not all claims are genuine. Frivolous Lawsuits are legal claims lacking any serious legal basis. Often these particular cases will… The article is meant to give readers a practical understanding of the issue so they can connect the topic to planning decisions instead of treating it as an isolated legal phrase.

Who should read this article?

This article is usually most useful for readers who are trying to understand Frivolous Lawsuits before making a trust, ownership, or asset protection decision and want a clearer explanation in everyday language.

Why does this topic matter in broader planning?

Topics like this matter because one misunderstood issue can change how readers think about timing, control, funding, or exposure. Articles like this help turn a broad concern into a more focused next step.

What should readers compare after finishing this article?

Most readers go next to a related trust page, a comparison page, or another article in the same category so they can test the idea against a larger planning framework before deciding what to do next.