Asset Protection

Asset protection strategies work best when they are built before pressure arrives. A strong plan can separate ownership, control, and access in a way that reduces exposure to future creditor problems while still supporting long-term family and business goals.

Trust-focused planning

Clear structure for asset protection, long-term stewardship, and family control.

Step-by-step guidance

Planning, drafting, funding, and next-step clarity in one coordinated process.

Designed for real-world use

Built to be understandable, actionable, and easier to maintain over time.

What asset protection really involves

Asset protection is not one single document and it is not a last-minute transfer made after a claim appears. The goal is to arrange ownership in a way that fits your risk profile, your family structure, your business interests, and the time horizon for major life events.

For many households and business owners, the work starts with identifying the assets that matter most, the liabilities most likely to arise, and the level of control you still need. That is why trust-based planning, business entities, funding decisions, and titling choices are often reviewed together instead of in isolation.

Who usually benefits from asset protection planning

Families with appreciated real estate, professionals in lawsuit-prone fields, founders, investors, physicians, and owners with concentrated wealth often need more than insurance alone. The more visible the balance sheet, the more important it becomes to organize it deliberately.

Business owners

Operating risk, contract disputes, employee issues, and personal guarantees can blur the line between company exposure and personal wealth. Business-focused planning helps address that overlap.

Real estate holders

Rental properties, development interests, and personally titled investment property can create avoidable exposure when they are not coordinated with entity and trust planning.

Families thinking long term

People who care about multigenerational control, privacy, and smoother wealth transfer often use protection planning to support both today’s defenses and tomorrow’s estate decisions.

Common tools used in a layered plan

The right structure depends on the assets involved, the jurisdiction, and the amount of independence needed between you and the property being protected. There is no universal answer, which is why a layered approach is often more durable than any single tactic.

Trust structures

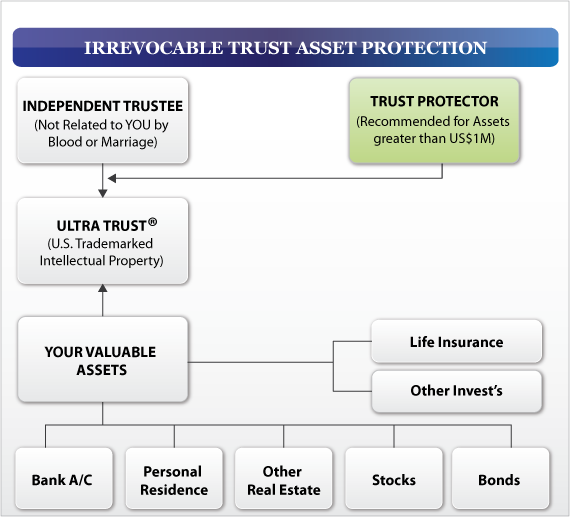

An asset protection trust may help create stronger separation than personal ownership when the trust is set up, funded, and administered properly.

Business entities

LLCs and limited partnerships can help contain operating risk and organize ownership, especially when paired with clear records and disciplined administration. See LLC vs trust for asset protection for a side-by-side look.

Funding and titling

A plan only works if the right assets are actually moved into the correct structure. Funding errors leave people with paperwork but no practical protection.

Mistakes that weaken otherwise good planning

The most common failures are not theoretical. People wait too long, transfer assets after a threat has already surfaced, keep too much personal control over a structure that is supposed to create distance, or leave valuable assets outside the plan entirely.

- Relying on verbal assumptions instead of written transfer records

- Creating a trust or entity but never funding it correctly

- Using the wrong tool for the asset type or risk level

- Treating state-law differences as a minor detail

- Ignoring how tax, lending, and administration affect the final structure

If you are evaluating domestic and international trust strategies, compare domestic options and offshore options before deciding where a structure belongs.

How a practical strategy is built

Good planning starts with facts instead of assumptions. The first step is usually a review of asset mix, exposure points, ownership records, family goals, and timing. From there, the work becomes a design exercise: deciding what should stay personally owned, what should move, and which structure best matches the intended protection.

- 1

Review the risk picture

Look at business ownership, real estate, liquid assets, professional exposure, family dynamics, and existing trust or entity documents.

- 2

Choose the right structures

Select the tools that fit the objective, whether that means a trust, entity planning, revised titling, or a coordinated combination.

- 3

Fund and document the plan

Retitle assets, update records, and align administration so the plan operates as intended in the real world.

- 4

Maintain it over time

Major purchases, sales, refinancing, and family events should feed back into the structure so the plan stays current.

Moving from concern to action

People usually start exploring asset protection because something already feels exposed: a growing company, a lawsuit-prone profession, a new property purchase, or a large concentration of wealth. Acting before pressure builds gives you more room to choose the structure that actually fits.

Need a starting point?

A private review can help you compare trust structures, timing, and funding priorities before you commit to the wrong setup.

Frequently asked questions

What assets are usually reviewed first in an asset protection plan?

Business interests, investment real estate, liquid reserves, brokerage accounts, and personally titled property are often reviewed early because they can create or absorb meaningful exposure depending on how they are held.

Is insurance enough by itself?

Insurance is important, but it does not replace legal ownership planning. Coverage limits, exclusions, and changing risk profiles are why many families and business owners use structural planning alongside insurance.

Can asset protection be done after a claim appears?

Timing matters. Once a known claim, judgment, or creditor issue is already in play, your options can narrow quickly. Pre-planning is generally stronger than reactive transfers.

Do trusts and LLCs solve the same problem?

Not exactly. An LLC is typically an entity used to hold or operate assets, while a trust addresses ownership, control, and distribution under fiduciary terms. In some plans they work best together.

Ready to take the next step?

Get clear guidance on trust structure, planning priorities, and the next move that fits your assets and goals.