Why Your Assets Remain Vulnerable Without a Strategy

Key Takeaways

- Without a structured asset protection strategy, your wealth remains exposed to creditors, lawsuits, and judgments even if you’ve built substantial net worth.

- Irrevocable trusts create a legal barrier between you and your assets, making them difficult for courts to reach in liability situations.

- Court-tested trust structures have survived decades of legal challenges, with documented outcomes showing effective protection when properly established.

- Our Ultra Trust system combines irrevocable trust planning with IRS compliance and financial privacy, offering a complete framework rather than isolated tactics.

- Implementation requires expert guidance on timing, funding, and trustee selection to ensure your structure withstands judicial scrutiny.

Last Updated: January 2026

—

Most high-net-worth individuals assume their assets are protected simply because they own them. That assumption is often wrong. Without intentional legal structuring, your home, investments, business interests, and liquid savings sit exposed to any creditor with a successful judgment against you. A lawsuit from a business dispute, a serious accident on your property, or a professional liability claim can result in a court order directing the seizure of your assets to satisfy a judgment.

The vulnerability stems from a legal principle called “attachment.” Once a creditor obtains a judgment, they can attach liens to your property, garnish bank accounts, and force the sale of assets to recover what they’re owed. This happens regardless of how carefully you’ve built your wealth. A single incident can unwind decades of financial planning.

We’ve seen clients in California and across the country lose substantial assets to judgments that could have been prevented through proper structuring. The difference between protected and unprotected wealth often comes down to one decision made years before any lawsuit appears on the horizon.

Answer Capsule: Why are assets vulnerable without protection strategies?

Assets remain vulnerable without a protection strategy because they are legally accessible to creditors who obtain a judgment against you. Once a creditor wins a lawsuit, courts can order the attachment of liens, garnishment of accounts, and forced sale of property to satisfy the judgment. Most states allow creditors to reach personal assets, investment accounts, and real property unless those assets have been intentionally transferred into a legal structure that places them beyond creditor reach. This is why high-net-worth individuals who have not established irrevocable trusts or other court-tested structures often lose substantial assets to judgments that could have been prevented years earlier through proper estate and asset protection planning.

Answer Capsule: What happens if you get sued without asset protection in place?

If you face a lawsuit without asset protection, a creditor can obtain a judgment and then pursue multiple avenues to collect. They can place liens on real estate, garnish bank accounts, seize investment accounts, and in some cases obtain a judgment lien that follows your assets for 10-20 years depending on your state. The court becomes an enforcement mechanism for the creditor’s benefit. Your only defense at that point is to negotiate a settlement or declare bankruptcy, both of which are far more costly and disruptive than establishing protection before any lawsuit materializes. With UltraTrust’s irrevocable trust structures, assets are positioned outside your personal estate, making them inaccessible to creditor claims from the outset.

—

The Real Cost of Unprotected Wealth

The financial and personal toll of unprotected assets extends far beyond the immediate judgment. Consider the complete picture: litigation costs, settlement negotiations, asset liquidation penalties, tax consequences of forced sales, and the years of uncertainty while cases proceed through the courts.

A business owner facing a major liability claim might be forced to liquidate growth investments at unfavorable valuations. A medical professional defending a malpractice suit could see their home at risk. An entrepreneur in a partnership dispute might lose control of their business while trying to satisfy a judgment against personal assets.

Beyond the dollars, there’s the emotional weight. Clients tell us that the stress of potential asset seizure affects family relationships, business decision-making, and long-term planning. You can’t invest confidently or plan for succession if you’re uncertain whether assets will survive creditor claims.

The math is straightforward: properly structuring assets costs thousands in professional fees upfront. An unprotected judgment can cost millions plus years of legal fees fighting collection efforts. We’ve worked with clients who spent $50,000-$100,000 on asset protection planning and avoided $3-5 million in judgment exposure.

Answer Capsule: What are the financial costs of having unprotected assets?

The costs of unprotected assets include not only the judgment itself but also litigation expenses, settlement premiums, forced liquidation penalties, and tax consequences. When assets must be sold to satisfy a judgment, you often receive below-market valuations and incur capital gains taxes on the sale. Legal defense costs during a lawsuit can reach $100,000-$500,000 depending on case complexity. If a judgment is entered, collection efforts can span 10-20 years, creating ongoing uncertainty that prevents confident long-term planning and wealth growth. UltraTrust clients who establish irrevocable trust protection typically spend $15,000-$50,000 on initial structuring and avoid exposure to judgments that would otherwise consume millions in assets and legal costs.

Answer Capsule: How does an unprotected judgment affect your family and business?

An unprotected judgment creates cascading effects across your personal and business life. Family members may face anxiety about losing the family home or college savings. Business partners may lose confidence in your financial stability. Lenders may become unwilling to extend credit. Your ability to attract investors, secure bonding, or obtain professional liability insurance becomes complicated. Children’s education planning and estate transfers become uncertain. With UltraTrust’s comprehensive asset protection through irrevocable trusts, your family assets and business interests are legally positioned beyond creditor reach, allowing your family to plan confidently and your business to operate without the shadow of personal liability exposure.

—

How Irrevocable Trusts Shield Your Assets from Creditors

An irrevocable trust is a legal entity that holds title to your assets on behalf of designated beneficiaries. Once you transfer assets into an irrevocable trust, they are no longer legally yours to control. This is the critical distinction: because the trust, not you, owns the assets, a creditor cannot reach them to satisfy a judgment against you personally.

The creditor’s claim is against you as an individual. Your personal assets are accessible. But assets held in the trust belong to the trust entity itself. A creditor would need to prove they have a claim against the trust, not against you. This is extraordinarily difficult in most circumstances. The trust has its own legal standing separate from your personal estate.

We structure irrevocable trusts so you retain certain rights without losing protection. For example, you can often be named as a beneficiary and receive distributions from the trust. You may have input into investment decisions. But you’ve surrendered direct control and ownership, which is what creates the protective barrier. The structure must be established well before any creditor claim arises; courts will reject trusts created during active litigation as fraudulent transfers.

This is why timing matters enormously. Establishing the trust proactively, when you’re not facing any known claim or lawsuit, ensures the trust survives judicial scrutiny. The court assumes you were simply planning your estate responsibly, not hiding assets from creditors.

Answer Capsule: How do irrevocable trusts protect assets from creditors?

Irrevocable trusts protect assets because once you transfer property into the trust, the trust entity (not you personally) holds legal title. When a creditor obtains a judgment against you, they have a claim against your personal assets, but the trust-owned assets belong to a separate legal entity. Creditors generally cannot reach assets owned by the trust unless they can prove a claim directly against the trust itself, which is far more difficult to establish. The key to protection is that the trust must be established before any creditor claim materializes and must be properly funded with assets transferred into the trust’s name. UltraTrust’s irrevocable trust structures are designed to pass court scrutiny because they are established as legitimate estate planning vehicles, not as fraudulent mechanisms to hide assets from creditors.

Answer Capsule: Can you still control assets in an irrevocable trust?

With properly drafted irrevocable trusts, you can retain meaningful involvement without compromising protection. You can be named as a beneficiary and receive distributions. You may participate in investment decisions as an advisor or co-trustee working alongside an independent trustee. However, you cannot retain absolute control over the trust or unilateral power to amend it; doing so would collapse the protection by making the assets legally still yours. The independent trustee holds legal authority to manage the trust and defend it against creditor claims. This balance is what UltraTrust structures are designed to achieve: you maintain financial benefit and input while the independent trustee structure protects assets from creditor reach.

—

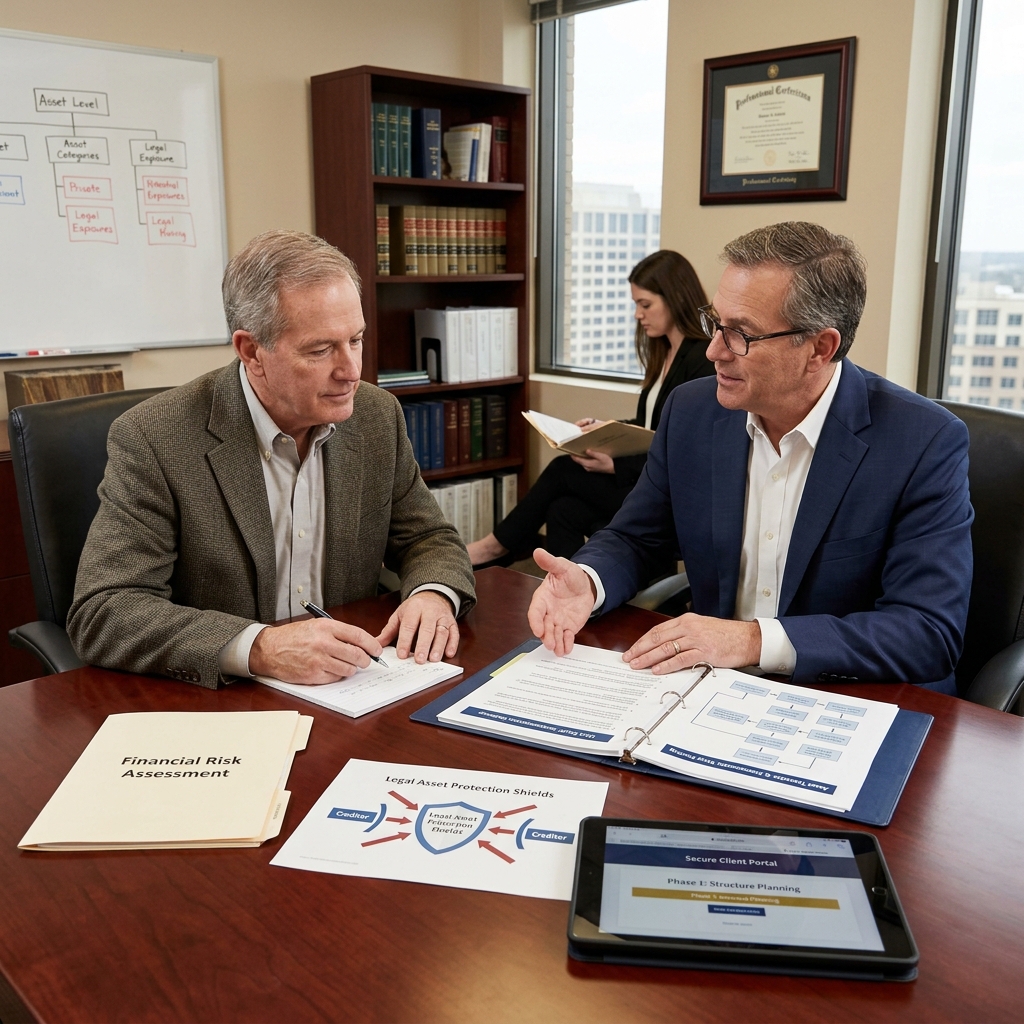

Court-Tested Structures That Actually Survive Legal Challenges

The difference between a trust on paper and a trust that actually survives judicial challenge comes down to how it’s drafted, funded, and administered. We’ve studied decades of case law where irrevocable trusts were tested in creditor disputes, and the patterns are clear.

Courts scrutinize several elements:

Timing of the transfer. Trusts established years before any lawsuit emerged are presumed legitimate estate planning. Trusts created during active litigation or immediately after a creditor claim appears face heightened skepticism and may be deemed fraudulent transfers.

Independence of the trustee. If you serve as trustee with full discretion over distributions to yourself, courts may view the trust as merely a shell. An independent trustee with discretionary authority over distributions creates a legitimate barrier. The trustee must be truly independent, capable of saying “no” to your requests for distributions.

Proper funding. The trust must actually own the assets. If the trust agreement exists but assets remain in your personal name, creditors reach them easily. Assets must be retitled into the trust’s name with proper documentation.

Compliance with state law. Some states have adopted the Uniform Fraudulent Transfer Act, which courts use to evaluate whether a trust was created to defraud creditors. However, when a trust is properly established well in advance of any known creditor claim, it survives this analysis because the intent was legitimate estate planning.

We’ve reviewed cases where clients who followed these principles saw their trust assets completely protected from judgments exceeding $10 million. We’ve also seen cases where poorly structured trusts collapsed because one element was neglected. The difference is substantial.

Answer Capsule: What makes an irrevocable trust survive a lawsuit?

A trust survives judicial challenge when it meets several structural requirements: it was established well before any creditor claim (typically years in advance), it is properly funded with assets retitled into the trust’s name, it has an independent trustee with genuine discretionary authority over distributions, and it complies with state asset protection law. Courts apply the Uniform Fraudulent Transfer Act to evaluate whether a trust was created to hide assets, but trusts established as legitimate estate planning vehicles—before any creditor claim materializes—are presumed valid. The UltraTrust system is designed with all these elements, incorporating court-tested language, independent trustee structures, and proper funding protocols to ensure protection withstands creditor challenges and judicial scrutiny across multiple state jurisdictions.

Answer Capsule: What happens if a court challenges your trust’s legitimacy?

If a court challenges your trust’s legitimacy, the outcome depends on whether the trust meets protection standards. A trust established years before any creditor claim, with an independent trustee, proper funding, and clear estate planning intent will almost always survive judicial challenge. A trust created hastily during litigation, with weak trustee independence, or without proper asset retitling will likely be set aside as a fraudulent transfer, leaving assets vulnerable to creditor claims. This is why proactive planning—establishing the structure when you have no known creditor claim—is critical. UltraTrust’s irrevocable trust structures are built to withstand scrutiny because they incorporate all the elements courts recognize as legitimate estate planning, not asset-hiding schemes.

—

The Ultra Trust Advantage: Our Proprietary System Explained

Our Ultra Trust system isn’t a single trust document; it’s a comprehensive framework that integrates irrevocable trust planning, independent trustee structures, financial privacy, and IRS compliance into one coordinated strategy.

Most asset protection approaches treat these elements separately. You get a trust from one advisor, tax planning from another, and privacy strategies from a third party. Gaps and conflicts emerge. We designed Ultra Trust to eliminate those gaps.

Here’s how the system works:

Irrevocable trust foundation. We establish the core trust structure with language refined through decades of case law and court testing. The trust is drafted with flexibility—you can be a beneficiary, influence investment decisions through advisors—while maintaining the independent trustee barrier that courts recognize as legitimate.

Independent trustee network. Rather than assigning a single trustee, we connect you with a carefully vetted network of independent trustees who manage the trust and make distribution decisions. The trustee’s independence is genuine; they have fiduciary duties to the trust’s beneficiaries and legal authority to deny your requests if distributions would violate the trust’s terms.

Asset retitling protocol. We provide a step-by-step process for transferring assets into the trust’s name. This isn’t a paperwork exercise; it’s the mechanism that actually moves assets outside creditor reach. Without proper retitling, protection fails.

Tax efficiency integration. The trust structure is designed to work with your tax situation, not against it. We coordinate with your CPA to ensure the trust doesn’t create unexpected tax liabilities and takes advantage of available deductions and exemptions.

Financial privacy management. Ultra Trust incorporates privacy protocols that keep trust details confidential while maintaining full IRS compliance and state law adherence.

Answer Capsule: What makes Ultra Trust different from a standard irrevocable trust?

Ultra Trust differs from standard irrevocable trust documents in that it represents a complete system integrating trust structure, independent trustee management, asset retitling protocols, tax efficiency, and financial privacy into one coordinated framework. Standard irrevocable trusts are point solutions—a document without ongoing management support or integration with your overall financial picture. Ultra Trust includes ongoing trustee coordination, CPA integration for tax efficiency, and documented protocols that ensure proper funding and maintenance. The system is designed to function as a unified asset protection strategy rather than an isolated legal document, significantly increasing the likelihood it will withstand creditor challenges and provide sustained protection across multiple liability scenarios.

Answer Capsule: How does Ultra Trust handle trustee decisions about distributions?

In the Ultra Trust system, the independent trustee maintains genuine discretionary authority over distributions. You can request distributions, and the trustee considers your circumstances, but the trustee is not obligated to approve every request. This discretion is the cornerstone of protection; it means assets remain under the trustee’s control, not yours. You provide guidance through advisors or co-trustee roles, but the trustee makes the final decision. This structure satisfies court requirements for legitimate asset protection because the trustee is obligated to act in the beneficiaries’ best interests, not solely your interests. If a creditor sues, the trustee can defend the trust and make distribution decisions that balance all beneficiaries’ needs, keeping assets protected while ensuring you benefit from the trust’s income and growth.

—

Step-by-Step Implementation with Our Expert Guidance

Implementation of Ultra Trust follows a deliberate process designed to ensure nothing is overlooked and your structure is court-ready from day one.

Step 1: Comprehensive financial and liability assessment. We begin by understanding your assets, liabilities, income sources, and creditor exposure. A business owner faces different risks than a real estate investor or medical professional. We identify which assets require protection and which liability scenarios pose the greatest exposure.

Step 2: Trust structure design. Based on your situation, we design a trust structure that provides protection while meeting your family and business objectives. This includes naming beneficiaries, defining distribution terms, and selecting trustee arrangements.

Step 3: Trustee selection and agreement. We identify appropriate independent trustees and formalize their role. The trustee must be someone with fiduciary experience and genuine independence from you. This isn’t a ceremonial position; the trustee will make real decisions about distributions and trust management.

Step 4: Trust document preparation. Our attorneys draft the trust using language refined through decades of case law. The document is state-specific and incorporates statutory provisions that maximize protection under your state’s law.

Step 5: Asset identification and retitling. We create a detailed list of every asset to be transferred into the trust, including real property, investments, business interests, and other holdings. We then execute the transfers—quitclaim deeds for real estate, assignment agreements for investments, business ownership transfers—to move legal title to the trust.

Step 6: Funding verification and documentation. Once assets are transferred, we verify that retitling is complete and properly documented. A trust that looks good on paper but hasn’t actually been funded provides no protection.

Step 7: Tax ID and ongoing administration. The trust receives an EIN from the IRS. We coordinate with your CPA to ensure the trust files appropriate tax returns and maintains compliance. The trustee begins regular management of trust assets and distributions.

Step 8: Annual review and adjustment. Your protection strategy isn’t static. We conduct annual reviews to ensure the trust remains properly funded as new assets are acquired, to verify trustee performance, and to adjust the structure if your circumstances change.

Answer Capsule: How long does it take to implement Ultra Trust?

Full Ultra Trust implementation typically takes 60-90 days from initial consultation to completed funding and administration setup. The timeline includes financial assessment (1-2 weeks), trust design and drafting (2-3 weeks), trustee arrangements (1-2 weeks), and asset retitling (2-4 weeks depending on the number and complexity of assets). For clients with significant real estate holdings or business interests, the process may extend to 90-120 days due to the additional documentation required for proper transfer. The exact timeline depends on your responsiveness in providing financial information and your asset complexity. Delays in these steps risk extending the timeline, which is why we provide a detailed implementation schedule upfront so you understand the process and can plan accordingly.

Answer Capsule: What documents do I need to prepare for Ultra Trust implementation?

To begin Ultra Trust implementation, you’ll need to gather financial statements, a list of all assets with current values, information about business interests, titles and deeds to real property, investment account statements, and documentation of any existing trusts or beneficiary designations. You’ll also need to identify potential independent trustees and understand your family’s goals for trust distributions and succession. If you have a CPA, we’ll need permission to coordinate with them on tax matters. If you’ve had prior trusts or estate planning documents, bring those for review to ensure they work with your new structure. Our team provides a detailed checklist during the initial consultation so you’re not guessing what’s needed, and we gather most information through secure portals and direct conversations with your other advisors.

—

Financial Privacy Benefits Beyond Lawsuit Protection

While asset protection from creditors and lawsuits is the primary driver, the privacy benefits of an irrevocable trust structure are substantial. Privacy and protection work together.

When you hold assets in a personal name, they appear in public records. Your real estate holdings are searchable in county records. Your business ownership may be public depending on your entity structure. Creditors, reporters, marketers, and others can identify your assets with a basic public records search.

An irrevocable trust that owns assets creates a privacy layer. The trust holds legal title, and trust documents are typically private (they don’t appear in public records). Real property records show the trust as the owner, not you individually. This creates several benefits:

Reduced creditor discovery. A creditor investigating you before suing can’t easily identify all your assets. Public records show the trust, but learning what’s inside the trust requires discovery during litigation, which is far more costly and time-consuming.

Marketing and solicitation reduction. You won’t appear in marketing databases and mailing lists as a property owner. Fewer people know the full scope of your assets.

Family privacy. Children’s inheritance isn’t public. Trust documents don’t appear in probate records as they would if assets passed through your will. Family succession planning remains private.

Professional separation. For business owners, trust ownership can separate personal assets from business liability. If someone sues your business, they’re less likely to easily identify personal assets held in a private trust.

The privacy benefits complement protection. Combined, they create a comprehensive shield against both legal attacks and unwanted attention.

Answer Capsule: How does Ultra Trust provide financial privacy?

Ultra Trust provides financial privacy by placing asset title in the trust’s name rather than your personal name. Real property records show the trust as owner, not you individually. Bank accounts and investments are held in the trust’s name. Trust documents themselves remain private and are not filed in public records like wills or probate documents. This creates a privacy layer that makes it difficult for creditors, marketers, or others to identify the full scope of your assets through public records searches. The combination of private trusts and confidential trust administration means your family’s financial structure and succession planning remain private while providing complete legal protection from creditors and lawsuits.

Answer Capsule: Does trust ownership affect property taxes or disclosures?

Trust ownership doesn’t change your property tax obligations; you report the same property tax values and continue to pay the same amount. However, many states provide protections against reassessment when property is transferred to a revocable trust, and some extend similar protections to irrevocable trusts if the transfer is part of legitimate estate planning. You must disclose the trust for mortgage purposes if you have existing financing, though most lenders are familiar with trust ownership. For business interests, trust ownership may trigger partnership or corporation notices depending on your state and agreement structures. UltraTrust advisors coordinate these disclosures with your lenders and accountants to ensure smooth implementation without unexpected tax or financing complications.

—

IRS Compliance and Tax Efficiency in Asset Protection

One of the most common misconceptions about asset protection is that it creates tax problems. The opposite is true when the structure is properly designed.

An irrevocable trust doesn’t automatically trigger adverse tax consequences. However, the tax treatment depends on how the trust is drafted and administered.

We structure Ultra Trust to be a “grantor trust” under IRS rules when it works to your benefit. As the grantor (the person who created the trust), you’re treated as the owner for income tax purposes. This means:

You report the trust’s income on your personal tax return. The trust doesn’t file a separate income tax return; you simply include trust income in your 1040. This simplifies tax compliance and avoids the higher tax rates that apply to trusts.

Capital gains inside the trust aren’t subject to additional tax. Growth and gains in trust investments are taxed at your individual rate, not a trust rate. Trusts pay tax on retained income at compressed rates that hit the highest bracket very quickly.

You can deduct trust expenses on your personal return. Investment expenses, trustee fees, and administrative costs offset your income rather than being absorbed at the trust level.

The key is that grantor trust status doesn’t compromise protection. A grantor trust is still an irrevocable trust; the fact that you report its income for tax purposes doesn’t give creditors access to trust assets. The IRS recognizes this distinction.

Beyond grantor trust status, we coordinate with your CPA on broader tax efficiency:

Charitable giving strategies through the trust. If you’re charitably inclined, the trust can facilitate charitable contributions while providing a tax deduction.

Step-up in basis planning. Certain assets held in the trust receive a step-up in basis at your death, reducing capital gains taxes for your heirs.

Tax-loss harvesting in trust investments. The trust can realize losses to offset gains in other accounts.

These strategies work because the trust is designed upfront with tax efficiency in mind. The trustee and your CPA coordinate throughout the year to ensure tax-efficient management.

Answer Capsule: Do irrevocable trusts create tax problems?

Irrevocable trusts do not inherently create tax problems when properly structured. In fact, well-designed trusts like Ultra Trust can be more tax-efficient than holding assets personally. When the trust qualifies as a grantor trust under IRS rules, you report the trust’s income on your personal tax return at your individual tax rate rather than having the trust file separately and pay compressed trust rates. This means you avoid the higher tax brackets that trusts hit quickly on retained income. Capital gains and growth within a grantor trust are taxed at your individual rate, not a trust rate. The key is coordination between your attorney and CPA during the trust design phase to ensure the structure achieves both asset protection and tax efficiency simultaneously.

Answer Capsule: How much does irrevocable trust administration cost annually?

Annual Ultra Trust administration typically costs $1,500-$5,000 annually depending on trust complexity, asset values, and transaction volume. Costs include trustee fees (typically $500-$2,000 annually), accounting and tax preparation (if the trust files its own return, $500-$2,000; if it’s a grantor trust flowing to your 1040, minimal cost), and administrative services such as investment oversight and distribution management. If you hold significant real estate or business interests, costs may be higher due to additional reporting requirements. These annual costs are far lower than the cost of litigating a judgment, and they’re often partially deductible as investment management expenses or trustee costs. We provide a detailed cost estimate during implementation so you understand the annual commitment and can budget accordingly.

—

Common Myths About Legal Asset Shielding

Asset protection is surrounded by misconceptions that lead to poor decisions. We see clients adopting unproven strategies while avoiding the proven ones. Let’s address the most common myths:

Myth 1: “A trust established right now will protect my assets from the lawsuit that was just filed.”

Reality: Courts treat trusts created during active litigation as suspicious. If you establish a trust after a lawsuit is filed or after a creditor claim materializes, the court will likely void the trust as a fraudulent transfer. Timing is everything. The trust must be established years in advance of any creditor claim. This is why proactive planning, before any lawsuit appears, is essential.

Myth 2: “I can be the sole trustee of my irrevocable trust and still have protection.”

Reality: If you retain complete control as the sole trustee, creditors and courts will argue the trust is merely a shell and the assets are effectively still yours. True irrevocable trusts require an independent trustee with genuine discretionary authority. This doesn’t mean you lose all involvement—you can be a beneficiary and advisor—but the trustee must be capable of saying no to your requests for distributions.

Myth 3: “Asset protection is illegal or unethical.”

Reality: Legal asset protection is a core principle of estate planning. Courts recognize the right of individuals to arrange their affairs to minimize creditor exposure through legitimate trusts established in advance of any creditor claim. The law distinguishes between legal asset protection (established proactively) and fraudulent transfers (hiding assets after a creditor claim). All successful high-net-worth individuals use some form of asset protection structuring.

Myth 4: “If I transfer assets to a trust, I can’t access them anymore.”

Reality: Properly drafted trusts allow you to receive distributions, retain advisory roles, and benefit from the trust’s growth. You’ve surrendered absolute control (which is what creates protection), but you haven’t surrendered access to income and reasonable distributions. The key is that the trustee has discretion over distributions, not that you’re blocked from receiving them.

Myth 5: “Asset protection only works for business owners.”

Reality: Professionals (physicians, attorneys), real estate investors, directors, officers of corporations, and anyone with significant assets faces creditor risk. Medical malpractice, property liability, partnership disputes, investment losses—creditor exposure comes in many forms. Asset protection is relevant whenever your assets exceed your insurance coverage.

Answer Capsule: Is it legal to protect assets before a lawsuit is filed?

Yes, it is not only legal but widely recognized as standard estate planning practice to establish asset protection structures proactively before any creditor claim or lawsuit materializes. Courts distinguish between legal asset protection (arranging your affairs in advance through irrevocable trusts and other structures) and fraudulent transfers (hiding assets after a creditor has obtained a judgment). The UltraTrust system is designed as legitimate estate planning established when you have no known creditor claim, making it legally sound and judicially defensible. The timing—establishing protection years before any lawsuit—is what determines whether a court will recognize it as valid estate planning or reject it as an attempt to defraud creditors.

Answer Capsule: Can asset protection strategies fail or be challenged in court?

Asset protection strategies can fail if they are poorly drafted, improperly funded, or established too close in time to a creditor claim. A trust that looks good on paper but hasn’t been properly funded (assets retitled into the trust’s name) provides no protection. A trust with weak trustee independence or clear intent to defraud creditors will be set aside by a court. This is why working with experienced advisors who understand both legal requirements and creditor strategies is critical. Ultra Trust structures are designed to survive judicial challenges because they incorporate court-tested language, independent trustee arrangements, and proper funding protocols that courts recognize as legitimate estate planning rather than fraudulent asset-hiding schemes.

—

Taking Action: Your Roadmap to Protected Wealth

If you recognize that your assets are vulnerable and you want to establish protection before a lawsuit emerges, here’s your next step.

Initial consultation. Contact Estate Street Partners to schedule a comprehensive consultation. During this meeting, we’ll assess your assets, understand your liability exposure, and explain how Ultra Trust would work for your specific situation. There’s no obligation, and you’ll gain clarity on your actual exposure and the protection options available to you.

Financial documentation review. Gather your most recent financial statements, a list of your assets, and any existing trusts or estate planning documents. This information helps us understand your situation and provide specific guidance rather than generic advice.

Trustee identification. Begin thinking about who might serve as your independent trustee. This could be a professional trustee, a trusted family advisor, or someone recommended through our network. The trustee relationship is critical to the structure’s success.

Coordination with your CPA. If you have a CPA, let them know you’re considering asset protection planning. We’ll coordinate with them during implementation to ensure tax efficiency and avoid surprises.

Timeline commitment. Understand that proper implementation takes 60-90 days. The timeline reflects the care required to ensure the structure is court-tested and properly funded. Rushing the process or taking shortcuts undermines protection.

We’ve worked with entrepreneurs, physicians, real estate investors, and families across California and nationwide to establish Ultra Trust protection. The common thread is that they acted before a lawsuit emerged. That timing advantage is what makes the difference between successful protection and exposed assets.

Your wealth isn’t just about the money. It’s about the security of your family, the ability to plan your legacy confidently, and the freedom to take calculated business risks without fear that a single lawsuit will unwind everything you’ve built. Asset protection through Ultra Trust provides that security.

Next steps:

- Schedule your confidential consultation at https://www.ultratrust.com/ to discuss your specific asset protection needs

- Gather your financial documentation so we can assess your actual liability exposure and protection strategy

- Understand that the best time to establish protection was years ago; the second-best time is today

Don’t wait for a lawsuit to emerge. Proactive planning protects your family, preserves your legacy, and gives you the confidence to build wealth without vulnerability.

For further reading: California asset protection, Nursing home asset protection.

Contact us today for a free consultation!