In the contemporary corporate milieu, securing assets is very important. One you may not have heard of is the captive insure structure. By accepting a level of insurance risk, companies can earn revenue and offset tax liabilities with this method. A captive insurance set up is unlike traditional insurance where the insurance company will own entity which insures the parent company.

Creating a captive insurance firm lets a business develop coverage, control claims, and even keep underwriting profits. It can be quite beneficial for organizations that have high liability exposure and/or specific risk profiles. It is important to know how a captive insurance structure operates and its advantages for long-term security.

A properly planned captive structure can enhance risk management and financial predictability while complementing other asset protection strategies. This guide takes you through its basics, advantages, practical considerations, and strategic uses for firms ensuring strong protection.

Comprehending Captive Insurance Frameworks

A captive insurance structure is an insurance company which is formed by a legal entity to insure its own risk.

A captive insurance firm belongs entirely to the organization it insures. They abide by the same regulatory frameworks as regular insurers but focus on custom risk management.

- Single-Parent Captives solely insure the parent company’s risks.

- Group Captives: Created by many businesses for risk-sharing.

- Rent-a-Captives a business can participate in a captive without full ownership.

- Significance within Risk Management.

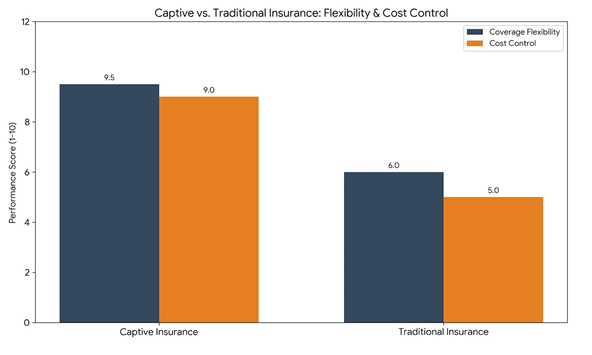

Captives offer flexible coverage that traditional insurers cannot provide. Businesses may insure specialized risks and coverage gaps that may be missing from other contacts. Moreover, captives stabilize costs, improve cash flows and create predictability for risk financing.

Advantageous Financial Strategy

| Feature | Description |

| Risk Control | Tailored coverage reduces exposure to unique business risks |

| Cost Efficiency | Potentially lower premiums than commercial insurance |

| Profit Retention | Underwriting profits remain within the parent company |

| Tax Optimization | Premiums may be deductible under IRS guidelines |

Businesses use a captive insurance structure because they want better control over risk management and improved financial outcomes.

Intricate Details of the Captive Insurance

It is essential to explore the mechanics and regulation for implementation.

Establishment and Authorization

- A captive must legally incorporate in a permissive domicile.

- Choosing a home with friendly laws.

- Getting licenses from insurance authorities.

- Conforming to capitalization and solvency needs.

Property and casualty risks

- Every industry has unique liability risks.

- Plans for employee health benefits

- Professional Liability Specialization.

- Conformity to Rules and Regulations.

Captives shall adhere strictly to local insurance regulations. Governance Structures Often Include.

These elements make sure the captive is effectively and legally compliant.

App Use Cases

- Organizations’ high liability claims result in controlling coverage.

- Organizations at risk can even costs.

- Companies aiming for tax efficiency could structure their premiums and losses.

- Captive insurance implementation details need to be understood to use it properly.

Example of a case study

A medium-sized manufacturing firm was incurring rising liability costs. By creating a captive for single parents.

Effectiveness of Risk Coverage

- Captive insurance enables organizations to design coverage specifically based on their distinct exposures, whereas the standard insurance tends to provide one-size-fits-all standardized coverage.

- By becoming their own insurer, companies utilizing captives can benefit directly from their own positive loss experience, significantly reducing premiums over the long term and lowering administrative expenses.

- Captives is a powerful asset protection The captive structure offers a regulated environment to support the firm’s long-term financial and wealth objectives.

Helpful Suggestions and Written Instructions

Designing a captive insurance requires skillful tactics and expert assistance.

Sequential Method

- Evaluate the risks particular to your business situation.

- Pick the place where you want to establish your residence.

- Achieve Incorporation with All Necessary Licenses

- Continuing to comply with audit and reporting rules.

Advice on How to Get More Benefits

- Seek advice from legal and insurance experts.

- For maximum cover, merge captives with traditional insurance.

- Review financial performance and change policies yearly.

- Ensure transparency to meet regulatory and tax authority requirements.

By following these steps, you ensure that the captive meets strategic objectives and runs smoothly.

Final thought

A captive insurance structure can be a great tool for businesses that want to manage risk and protect their assets.

Controlling insurance policies, managing profit retention and customizing coverage can help companies mitigate their liability exposure. Getting things done on time with proper planning and following the rules helps success.

Captive insurance, when used in combination with other asset protection strategies, can provide permanence and flexibility. At UltraTrust, a captive insurance structure helps secure assets, reduce costs, and support smarter planning for future-minded organizations.

A carefully structured captive is more than an insurance; it is a financial instrument that helps in creating a sustainable future while also growth risks efficiently.

Common questions about this article

These answers summarize the topic in plain English so readers can move from the article into the next practical planning page.

What is the main takeaway from "Captive Insurance Structure: A Strategic Approach to Asset Protection"?

In the contemporary corporate milieu, securing assets is very important. One you may not have heard of is the captive insure structure. By accepting a level of insurance… The article is meant to give readers a practical understanding of the issue so they can connect the topic to planning decisions instead of treating it as an isolated legal phrase.

Who should read this article?

This article is usually most useful for readers who are trying to understand Captive Insurance Structure before making a trust, ownership, or asset protection decision and want a clearer explanation in everyday language.

Why does this topic matter in broader planning?

Topics like this matter because one misunderstood issue can change how readers think about timing, control, funding, or exposure. Articles like this help turn a broad concern into a more focused next step.

What should readers compare after finishing this article?

Most readers go next to a related trust page, a comparison page, or another article in the same category so they can test the idea against a larger planning framework before deciding what to do next.